podcast

Building Your Financial Foundation

Starting a family or navigating your twenties and thirties is an exciting time—but it’s also when the most costly financial mistakes happen. After 40 years of helping people fix their finances, I’ve seen the same pattern over and over: the decisions you make early in life can cost you between $50,000 and $500,000 over your lifetime.

The good news? These mistakes are completely preventable. Today, I’m going to show you exactly how to build a rock-solid financial foundation from day one—so you never become that statistic.

The $640,000 Mistake: Understanding Opportunity Cost

Take $10,000. Let’s say you blow it on something that doesn’t matter. What did that really cost you?

If you earn 10% on your money, it doubles every seven years (the Rule of 72). If you’re young with 40 years until retirement, you have six doubling periods:

- Year 7: $20,000

- Year 14: $40,000

- Year 21: $80,000

- Year 28: $160,000

- Year 35: $320,000

- Year 42: $640,000

That $10,000 mistake just cost you $640,000. This is why getting started right matters so much.

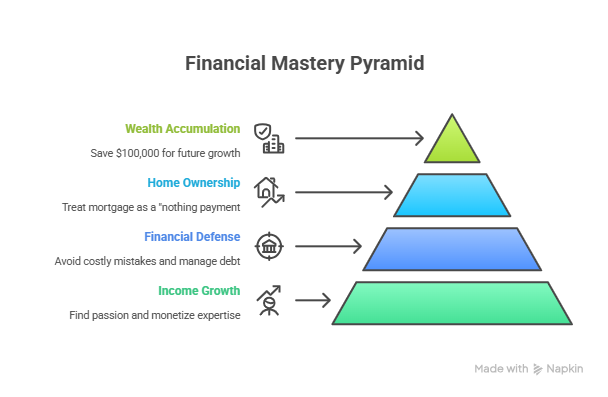

The Four Focus Points for Young People

After 40 years in this business (yes, I started at 25 and I’m now 64), I’ve identified four critical areas every young person needs to master:

1. Grow Your Income

By age 30, you should have found something you genuinely like doing. Not a job—something that feels like a hobby you get paid for.

People ask me all the time: “Are you ever going to retire?” My answer is always the same: “No. Why would I?” I have fun doing what I’m doing. I plan my own time, play lots of golf, and enjoy life because I found work I love.

The path forward:

- Find something you like (you’ll naturally become good at it)

- Become the best at it

- Monetize your expertise

- Consider self-employment or strategic job changes

I went 18 years straight making more income every year. Not cost-of-living increases—value increases based on what I brought to clients and my organization.

2. Play Defense (Goal: Don’t Lose)

Defense means avoiding the costly mistakes that derail financial plans:

- Budget properly

- Understand good debt vs. bad debt

- Protect your income and assets with insurance

- Master money management skills

The number one thing that helps people more than anything? A usable budget—a spending plan that controls money in advance, not an accounting system that shows you where it all went after it’s gone.

3. Achieve Home Ownership

Buy your home right. We’ll cover this in detail, but the key is treating your mortgage payment as a “nothing payment”—if you have to think hard about affording it, it’s too big.

4. Save Your First $100,000

If you’re in your early twenties, getting to $100,000 is your first major milestone. Why? Because at age 30, with five doubling periods ahead of you, that $100,000 becomes serious wealth.

Financial Mastery Pyramid

Understanding the Rule of 72

This is essential knowledge: Any interest rate divided into 72 tells you how many years it takes your money to double.

- 10% (S&P 500 historical average): Doubles every 7 years

- 2% (typical bank account): Doubles every 36 years

Over 40 years at 10%, you get six doubling periods. At 2%, you get one doubling period. That’s the difference between building wealth and staying broke.

The GPS System: Goal, Plan, Schedule

The Goal

Ask yourself: If your income went away, how long could you live?

The calculation: Total savings ÷ Monthly living expenses = Months of financial security

Example: $100,000 saved ÷ $5,000/month = 20 months of runway

Your ultimate goal? Live forever on your investments while leaving an inheritance. Rule of thumb: 20 times your desired annual income equals financial independence.

Want to retire on $100,000/year? You need $2 million.

The Plan

Determine how much to save monthly at what rate of return to hit your goal.

Real numbers to reach $100,000:

- In 5 years at 9%: $1,392/month

- In 10 years at 9%: $547/month

Visit sec.gov and use their compound interest calculators to run your own numbers.

The Schedule

When do you want to achieve financial independence? 10 years? 20 years? 30 years? Your timeline determines your monthly savings requirement.

Example: To save $18,000/year (about $1,400/month), you’d need to earn roughly $72,000. Save 25%, live lean, and you’re off to the races.

Building Your Team of Trusted Advisors

You need people who know more than you do in specific areas:

- Someone great with your health (doctor)

- Someone great with your money (financial advisor)

- Someone to help you avoid bad legal decisions (attorney)

Wealthy people don’t try to do everything themselves. They build teams.

The Emergency Fund: Your First Savings Goal

Target: 3-6 months of expenses

- Dual income household: 3 months minimum

- Single earner household: 6 months minimum

Example: If monthly expenses are $5,000:

- Dual income: $15,000 emergency fund

- Single income: $30,000 emergency fund

Why Emergency Funds Matter

The “return” on your emergency fund isn’t the 3% interest—it’s everything you avoid:

You can now:

- Raise deductibles on car insurance (save money monthly)

- Raise deductibles on health insurance (if self-employed)

- Self-insure older vehicles (drop collision coverage)

- Pay cash in advance for services (get discounts)

- Avoid raiding retirement accounts during emergencies

The Pay-Yourself-First Principle

When I started in this business, I set up:

- $100/month → Money market account (emergency fund)

- $50/month → Investment account (wealth building)

How I did it: Automatic draft, hitting my account around the first of the month when other bills were due. This way, I paid myself first before the money could disappear.

Critical truth: If you wait to have “money left over,” you’ll never save. There’s always something else to spend it on.

The Budget System That Actually Works

Download the budget forms at roymatlockjr.com, then follow this system:

Step 1: Understand Your Current Reality

If you have consumer debt (credit cards, car payments) and little savings, you’re spending more than you make. Period.

Step 2: Fire All Your Expenses

Pretend you have $100,000 income and zero bills. Now ask: Which expenses would I NOT rehire?

- That subscription? Don’t need it.

- That expensive car? Too much.

- Eating out so much? Not necessary.

- Rent too high? Maybe downsize.

Goal: Create a 25% gap between income and expenses.

Step 3: Set Up Your Account Structure

Account #1: The Draft Account (All Income Flows Here)

- All household income deposits here

- All automated bills draft from here

- House payment, utilities, insurance, savings—all automated

Before money even reaches this account, maximize 401k matching and tax benefits.

Account #2: The Future Purchase Account This is a tracking system on paper. Money accumulates in the draft account, but you allocate it mentally for:

- Vacation fund

- Christmas fund

- Car replacement fund

- Home maintenance fund

When it’s time for vacation, transfer the accumulated amount to your spending account.

Account #3: The Weekly Spending Account Every Sunday, transfer your weekly allowance here:

- Gas

- Groceries

- Eating out

- Misc expenses

Pro tip: Get daily email alerts showing your balance. When you see “$100 left with two days to go,” you know exactly where you stand.

The Insurance Defense

Term Life Insurance

Purpose: Income replacement if something happens

Rule of thumb: 10-12 times your annual income

A 30-year-old can get $1 million in coverage for less than $100/month. There’s no excuse not to have this.

New benefit: Living benefits riders let you access up to 90% of your death benefit if you become critically or terminally ill. Money when you need it most.

Permanent Life Insurance

Purpose:

- Final expenses

- Estate planning

- Legacy for family

- Replaces lost Social Security income for surviving spouse

Why buy young? It’s cheaper and easier to qualify for.

Disability Insurance

I believe becoming disabled is worse than dying. If you die, your family gets life insurance. If you’re disabled without coverage, you can’t work, can’t earn, and can’t fix the situation.

Many employers offer disability insurance. If not, purchase it privately.

Health Insurance

Inexcusable to skip this. Health insurance is cheap when you’re young—often $100/month or less through health share plans.

As your emergency fund grows, raise your deductibles to save on premiums. Consider high-deductible plans with Health Savings Accounts (HSAs)—they’re like “super IRAs.”

Auto, Home, and Liability Coverage

Target liability: $300,000 minimum on auto insurance

Why? If you cause an accident and hit an expensive car or cause serious damage, you’re covered.

Raise deductibles as your emergency fund grows—$1,500 or higher.

Get an umbrella policy: $1-2 million in extra liability coverage for $500-$1,000/year. I call this a “cheap lawyer.”

Real story: I got sued after a fender bender (my Mercedes apparently made me a target for someone claiming back injuries). My umbrella policy covered everything. Cost to me? About 45 minutes with the insurance company, my cell phone records, and my annual premium. Two years later, settled. Done.

Good Debt vs. Bad Debt: The Critical Distinction

Bad Debt

- You can’t afford the payment

- It’s tied to something that depreciates (loses value)

Examples: Credit cards, car loans on vehicles you can’t afford, financing consumer goods

Good Debt

- You can easily afford the payment

- It’s tied to something that appreciates (gains value)

Examples: Mortgage on a home you can afford, rental properties, productive business equipment

Important: Don’t pay off those 3% mortgages early. There are better places for that money.

Getting Out of Bad Debt

Step 1: Get Your Budget in Place

You cannot eliminate debt without controlling spending first.

Step 2: Stop the Refinancing Cycle

Credit cards refinance every month by reducing your minimum payment as your balance drops. This keeps you in debt for 30 years.

Solution: Levelize your payments. If you’re paying $200 this month, set up automatic $200 payments every month. This drops your payoff timeline from 30 years to about 3 years.

Step 3: The Debt Snowball (Optional Motivation)

Dave Ramsey and I created this method years ago when we were on air together:

- Pay minimum payments on all debts

- Put ALL extra money toward your smallest debt

- When it’s paid off, take that entire payment and add it to the next smallest debt

- Repeat until debt-free

The psychological wins keep you motivated.

Buying Your First Home

The golden rule: Treat your mortgage as a “nothing payment.” If you have to think hard about affording it, it’s too big.

Buy something less expensive, pay it down a bit, and as your income grows, trade up. That’s the path to homeownership without being house-poor.

Estate Planning for Young Families

If you have kids, you need these documents:

- Will or Living Trust

- Healthcare Power of Attorney

- Financial Power of Attorney

- Guardianship designations for children

What happens if you don’t? If something happens to both parents, the courts decide who raises your kids and manages any inheritance. Don’t let that happen.

Easy solution: Visit roymatlockjr.com—we have term life insurance (up to $2 million) that can be issued in 10 minutes with AI underwriting (no blood work or physicals) and includes a do-it-yourself will and trust. Knock it all out in one afternoon.

The Path to Your First $100,000

Once you’ve handled the basics—budget, emergency fund, insurance, debt elimination—your focus shifts to accumulation.

Automate Everything

- 401k contributions (get that employer match—it’s free money!)

- IRA contributions

- Mutual fund investments

Start College Savings Early

When my daughter was born 33 years ago, I immediately set up her college fund. She attended a private four-year college, and it was paid for. No student loans. I did this for all my kids because I understood compound interest.

The Magic of Starting Young

I remember being so excited to set up that first college fund. The earlier you start, the less painful it is. A little bit for many years beats a lot for a few years.

Living Below Your Means: My Personal Stories

I’ve lived these principles my entire life:

Suits: When I was making real money, I bought suits at Ladies of Charity sales for $50 instead of paying $500 at department stores.

Dress shirts: I bought brand new pinpoint Oxford dress shirts at Goodwill for $1 each. People who donate to Goodwill are often wealthy—they buy quality and donate it when they outgrow it.

Cars: I decided never to buy anything new. Let someone else take the depreciation hit.

Hotels: I still negotiate better deals.

Rental cars: Same thing.

Cabs: Just the other night, a driver wanted $35 from downtown Nashville. I said, “I’ll give you $20. I live here—you’re not getting $35.” He took the $20.

The principle: Work hard for your money. Don’t throw it away. Watch the little dollars, and they become big dollars.

Exception: I tip generously for great service. If someone does a great job, I pay well. But I don’t overpay for poor service or inflated prices.

Growing Your Skills Through Education

Want to know how I grew my skill set? I listened to productive content while driving.

The math:

- 1 hour daily = 365 hours/year

- 5 years = 1,825 hours of education

You’re driving anyway. Why not make it worthwhile? Now you can listen to podcasts on any topic imaginable.

Shameless plug: We have about 200 podcast episodes on roymatlockjr.com covering everything you need to know about money. A recent client told me he listened to every single episode before our first meeting. (You don’t have to do that, but it certainly helps!)

The 11-Point Getting Started Action Plan

- Grow your income by developing valuable skills

- Set up your budget using the three-account system

- Automate retirement plans (401k with match, IRAs)

- Get term life insurance (income replacement)

- Get permanent life insurance (if appropriate, while you’re young and healthy)

- Get disability insurance (through work or purchased privately)

- Get health insurance (high-deductible plans with HSAs)

- Protect assets with proper insurance (auto, home/renters, umbrella liability)

- Eliminate bad debt (levelized payments or debt snowball)

- Start college savings for kids (529 plans, ESAs, UTMAs)

- Create estate documents (will, trust, powers of attorney)

Taking the First Step Today

If you’re a young person just getting started, or if you have kids or grandkids who need this guidance, here’s what to do:

Start with a few hundred dollars a month. We’ll help you. I love working with young people. We have young advisors who will meet with you and get the basics in place.

Get the essentials immediately:

- Term life insurance

- Will and trust (in case something happens)

- Investment accounts (start with $250)

Visit roymatlockjr.com to:

- Schedule a free 30-minute consultation

- Download budget forms

- Access 200+ podcast episodes

- Learn about our instant-issue life insurance (with free will and trust)

- Get started with as little as $250

The Bottom Line

Everything is about management. If you manage your money, it gets better. If you manage your health, it gets better. If you manage your career, it gets better.

Why would you work your entire life and struggle? Set aside some money, create a plan, and get on track.

The wealthy don’t work harder—they work smarter. They pay themselves first. They automate good behaviors. They avoid costly mistakes. They build teams. They think long-term.

You can do this. The question isn’t whether it’s possible—it’s whether you’ll take action today.

After 40 years in this business, I can tell you: The people who start young and follow these principles don’t worry about money. They’ve taken that stress off the table. And you can too.

Listen to the Full Podcast

Want to hear more details, real client stories, and additional strategies for young families? Listen to the complete episode where I walk through each principle with specific examples.

Listen to the full podcast episode: “Building Your Financial Foundation”

In this episode, I share personal stories about buying used cars, negotiating deals, and building wealth from scratch. I also explain the exact account structure for budgeting, the insurance products every young family needs, and how to avoid the mistakes that cost tens of thousands of dollars. This is essential listening for anyone starting their financial journey.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.