The High Cost of Procrastination

Do you have an invisible sign on your forehead that says, “I’m not saving any money right now, and every day I’m not saving money, I feel bad”?

If you’re a money procrastinator, this is your wake-up call. Today, we’re going to automate, accumulate, and protect your money—and finally get it moving.

What Is Procrastination Really Costing You?

Procrastination is the act of delaying or postponing important tasks, often replacing them with easier or less urgent activities. In money terms, it’s the failure to act on financial decisions when the cost of waiting is much higher than the cost of doing something.

We call this the “high cost of waiting” in investing—missing critical compounding periods that can never be recovered.

Here’s the brutal truth: Not making a decision IS a decision. And it’s usually the most expensive one.

- Money sitting in a bank account earning 0.5%? That’s a decision.

- Holding a stock you wouldn’t buy today? You’re buying it every day by not selling.

- Not contributing to your 401k? That’s choosing to leave free money on the table.

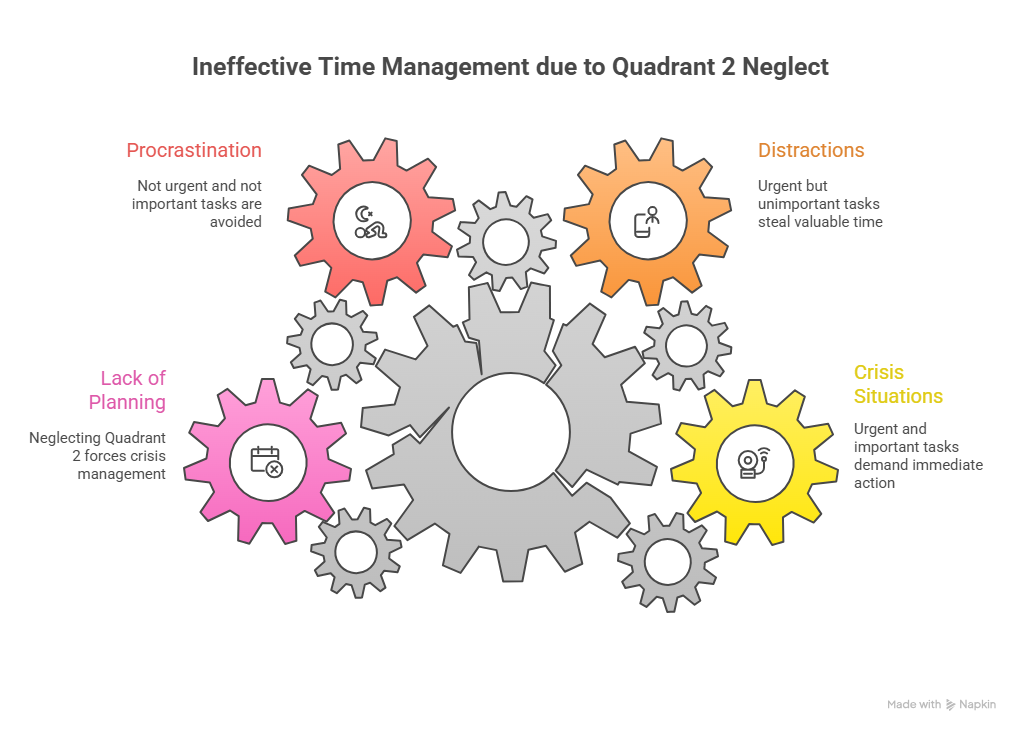

Ineffective Time Management due to Quadrant 2 Neglect

The Four Quadrants of Time Management

Stephen Covey’s “Seven Habits of Highly Effective People” introduced four quadrants that explain why we procrastinate:

Quadrant 1: Urgent and Important

- Crisis situations, pressing problems

- You have no choice—you must act

Quadrant 2: Not Urgent but Important ← THE KEY TO GETTING AHEAD

- Goal setting, planning, thinking

- Most people avoid this because “thinking is hard work” (as my dad used to say)

Quadrant 3: Urgent but Not Important

- Time wasters, distractions

- Feels busy but accomplishes nothing

Quadrant 4: Not Urgent and Not Important

- Pure procrastination territory

The problem: By lack of planning in Quadrant 2, we force ourselves into Quadrant 1 crises. You’re now behind on your money, didn’t start early, and have to buckle down urgently to catch up.

The Quality of Life Gap

Your financial stress comes down to this simple formula:

Income – Outgo = Quality of Life Gap

- Gap is positive (income > expenses): Good quality of life, low stress

- Gap is negative (expenses > income): Poor quality of life, high stress

Most stress comes from poor planning and procrastination, not actual inability to save.

Why Procrastination Is the #1 Wealth Killer

Most people don’t fail financially because of bad investments. They fail because they never get started.

Procrastination is the most expensive habit you can have. It’s costing you money right now. Today. This month. This year.

The Real-World Cost of Waiting 10 Years

Let’s make this concrete. If you wait 10 years to invest $500/month:

At 10% return (money doubles every 7 years):

- Years 1-10: Invest $60,000 → Grows to $120,000

- Years 11-17 (first doubling): $120,000 → $240,000

- Years 18-24 (second doubling): $240,000 → $480,000

- Years 25-31 (third doubling): $480,000 → $960,000

By waiting 10 years, you missed four doubling periods:

- What you could have had: $960,000+

- What you’ll actually have: $120,000

- Cost of procrastination: $840,000

That’s not a typo. Waiting 10 years cost you nearly a million dollars.

Good Intentions vs. Implementation

Here’s what I know after 40 years: People have great intentions. What they lack is implementation.

Systems are the key, not willpower.

When I first got started in 1985, the number one thing that caused me to have money was a simple bank draft from my checking account into investments:

- $50/month into a mutual fund

- $100/month into a money market account (emergency fund)

Forty years later, I don’t worry about money because of those early automations. My bills go out automatically. My investments go out automatically. The system works whether I think about it or not.

Wealth Is Built by Habits, Not by Hoping

You will not become financially independent by hoping for it. You need:

- Auto savings

- Auto 401k contributions

- Auto bill pay

- A system that removes daily decisions from the equation

Remember: “Someday” mentality never works. “Someday” never happens.

The Three Money Buckets

Understanding where to put your money is critical. Here’s the framework:

Bucket #1: Taxable and Liquid (Emergency/Opportunity Fund)

Rule: If it’s easily accessible, it’s probably taxable.

Emergency Fund

- 3-6 months of expenses

- Money market account (not a bank)

- Target: $15,000-$30,000 depending on income

The real “return” on emergency funds:

- Raise car insurance deductibles (save 15-30% on premiums)

- Raise homeowner’s insurance deductibles (save 20-40%)

- Lengthen disability income waiting period (save on premiums)

- Raise health insurance deductibles (if self-employed)

- Avoid credit card debt at 20% interest

- Avoid retirement plan penalties and taxes

Effective return: 15-20% when you account for everything it enables.

Opportunity Fund

- Balanced stock/bond fund

- Liquid but growing

- Available for unexpected opportunities

Real story: I had a client with opportunity money set aside. His business partner wanted out. He bought him out using the opportunity fund—and got a 100% return on that money because of the value of owning the entire business.

What happens if you procrastinate on this?

- Every car repair becomes a crisis

- Medical bills create panic

- You rely on 20% credit cards to survive

- You raid retirement accounts and pay penalties

Bucket #2: Tax-Deferred and Tax-Free (Retirement Accounts)

Rule: If it’s not easily accessible (locked until 59½), it probably has tax benefits.

Uncle Sam’s deal: “We’ll give you powerful tax incentives if you save for retirement.”

Think about this: Would you pay double on your electric bill? Double on your water bill? Of course not.

But when it comes to taxes, I see it 8 out of 10 times—people paying way more than necessary just by ignoring simple strategies.

Tax-Deferred Options (Deduct Now, Pay Later)

401k/403b

- Pre-tax contributions

- Employer match (FREE MONEY)

- Up to $30,500/year if over 50

Example math:

- Contribute 6%, employer matches 3% = 9% going in

- Tax deduction at 25% bracket means it only costs you 5% to invest

- You put in 5%, you get 9% ← That’s a no-brainer

Traditional IRA

- Tax-deductible now

- Tax-deferred growth

- Pay taxes when you withdraw

SEP IRA / Solo 401k (Self-Employed)

- Up to 25% of profit (SEP)

- Up to $30,500+ (Solo 401k)

- Massive tax deductions

Recent real example: I had three self-employed clients in the last few weeks who weren’t contributing to retirement plans. If you’re making $200,000, you could shelter $50,000 and save $15,000 in taxes (at 30% bracket).

Annuities

- Tax-deferred growth

- No contribution limits

- Multiple types (fixed, indexed, RILA, variable)

Tax-Free Options (Pay Tax Now, No Tax Ever Again)

Roth IRA

- After-tax contributions

- Tax-free growth

- Tax-free withdrawals forever

- Best for young people with decades to compound

Roth 401k

- Same as Roth IRA but through employer

- Higher contribution limits

Backdoor Roth

- For high earners who can’t contribute directly

- Contribute to non-deductible IRA, then convert to Roth

The Buy-One-Get-One-Free Strategy:

- Max out 401k (get the tax deduction)

- Take the tax savings ($2,500 at 25% bracket on $10,000)

- Put that $2,500 into a Roth IRA

- Now you have both: tax-deferred AND tax-free accounts

Who Should Use Which?

Roth (Tax-Free):

- Young people with decades to grow

- People currently in low tax brackets

- Those who want tax-free income in retirement

Traditional (Tax-Deferred):

- High earners in peak earning years

- People behind on savings who need bigger deductions

- Those expecting lower income in retirement

Often the answer is BOTH through the buy-one-get-one strategy.

The Power of Compounding + Tax Savings

Compounding + Tax Savings = Exponential Wealth Building

Let me show you with numbers:

$500/month for 30 years:

- At 3% (bank account): $286,000

- At 8%: $684,000

- At 10%: $995,000

- At 12%: $1,476,000

Same $500. Same 30 years. Different results:

- Best case: $1,476,000

- Worst case: $286,000

- Difference: $1.19 million

The difference between putting money in a bank versus working with professional money managers? Over a million dollars in this example.

What Procrastination Actually Costs You

Missing employer match = Leaving free money on the table

If your employer matches 3% and you don’t contribute, you’re throwing away thousands per year.

Delaying contributions = Losing compounding periods

Start with $400,000 at age 50. Wait 7 years (one doubling period at 10%). You could have had $800,000 instead.

Cost of waiting: $400,000.

Retiring with only Social Security = Severely limited lifestyle

Social Security replaces about 40% of pre-retirement income. Without other sources, your quality of life drops dramatically.

Delaying insurance = Higher premiums or becoming uninsurable

Life insurance, disability insurance, long-term care—all get more expensive with age. Some people wait too long and become uninsurable.

The Implementation System: How to Stop Procrastinating

Step 1: Schedule a Call

Visit RoyMatlockJr.com or call 615-843-2999. Get on our calendar.

Step 2: The Review

We assess where you are financially—what’s working, what’s not, what you’ve done right, what you’ve missed.

Step 3: Build Your GPS

- Goal: When do you want financial independence? What do you need?

- Plan: How much do you save monthly? What rate of return?

- Schedule: Timeline to achieve the goal

Step 4: Implementation

We don’t just tell you what to do. We make it happen.

- Set up automatic drafts

- Open the right accounts

- Choose appropriate investments

- Implement insurance coverage

- Create estate documents

Step 5: Automation

Here’s what happened yesterday: I set up a new client with $1,500/month going into automatic draft.

Think about that. What do they have to do? Nothing. Just have the money in their checking account.

- Money gets direct deposited (already happening)

- We automatically move it to investments

- They’re on their way to wealth

It’s that simple. Have it in your account. We move it out. You get wealthier.

The Defense: Protecting What You Build

You can’t play offense without defense. One big illness, accident, or lawsuit can wipe out years of growth if you’re not protected.

Budget: The Foundation

Download the budget form at RoyMatlockJr.com, then:

- Look at last year: “I made $100,000”

- Fire all your expenses (pretend you have zero)

- Ask: “Which would I NOT rehire?”

- Too-expensive car? Fire it.

- Unused subscriptions? Fire them.

- Too-large house? (Can’t fire immediately, but plan to downsize)

- Create a gap that allows saving

My story: I had $637/month in car payments in the 1980s. Bought two junkers, eliminated the payments, and put $637/month into mutual funds automatically.

That’s when everything changed.

Life Insurance: Two Types

Term Insurance (If You Die)

- Low cost, high coverage

- Protects income for a specific period

- Rule of thumb: 10x your income

Permanent Insurance (When You Die)

- Indexed Universal Life or Variable Life

- Tax-free growth and withdrawals

- Death benefit for life

- Uses: Estate planning, legacy, replacing lost Social Security for surviving spouse

I used to tell people never to buy permanent insurance. I’ve changed my mind. The right products, used correctly, are powerful tax-free wealth-building tools.

Health Insurance

Medical bankruptcies are preventable. There’s no excuse not to have coverage.

Options:

- Health share plans

- High-deductible plans with HSAs

- Employer coverage

Disability Insurance

Being disabled is worse than dying. If you die, your family gets life insurance. If you’re disabled with no coverage, you can’t work, can’t earn, and can’t fix it.

Get disability coverage through work or buy it privately.

Property & Casualty

What we protect:

- Home (or renters insurance)

- Auto

- Personal liability

- Business assets (if applicable)

Personal umbrella policy:

- $1-2 million in additional liability coverage

- Cost: $500-1,000/year

- Protects against lawsuits

Bottom line: We buy insurance to protect income OR assets. Life insurance = income. Health insurance = assets. Disability insurance = income. Property/casualty = assets.

Developing Multiple Income Streams: Bulletproof Retirement

Would you rather have one retirement income stream or ten?

The more income streams, the more secure you are. If one dries up, you have others.

Possible Retirement Income Streams:

- Social Security (automatic if you worked)

- Pension (if you have one—rare these days)

- 401k/IRA withdrawals

- Roth IRA (tax-free withdrawals)

- Annuities (lifetime income guarantees)

- Life insurance cash value (tax-free policy loans)

- HSA (tax-free for medical, regular retirement account after 59½)

- Part-time work/hobby income (do what you love)

- Business income (own a company, consult, franchise)

- Rental real estate

- Royalties (intellectual property)

- Brokerage accounts (taxable investments)

- Business succession (sell or transfer your business)

- Inheritance (don’t count on it, but it might happen)

- Reverse mortgage (if needed)

How do you get these income streams? You implement them. You don’t wait. You don’t hope. You act.

The Only Excuse That Doesn’t Work Anymore

“I don’t know how.”

You’re reading this blog post. You have access to:

- 200+ podcast episodes at RoyMatlockJr.com

- Free budget forms

- Monthly educational webinars (second Saturday of every month)

- Searchable podcast database

- Free 30-minute phone consultations

- Professional advisors ready to help

There’s absolutely no reason you should not become financially independent.

The information is there. The tools are available. The systems work.

If you’re not doing it, it’s your fault. (I’m saying this with love—tough love—but it’s true.)

Stop Procrastinating. Start Today.

It’s almost nine months into 2025. We can’t let another month, another week, another day pass.

Here’s what to do right now:

Immediate Actions:

- Visit RoyMatlockJr.com

- Schedule a free phone call

- Download the budget form

- Sign up for the next webinar

- Listen to relevant podcast episodes

What We’ll Do Together:

- Implement your plan (not just discuss it—implement it)

- Set up automations

- Open the right accounts

- Get insurance in place

- Create your GPS (Goal, Plan, Schedule)

What You’ll Get:

- One less financial worry

- Automated wealth building

- Protection for your family

- Peace of mind

- A clear path to financial independence

The Bottom Line

Procrastination destroys more wealth than bad markets ever could.

Good intentions without implementation mean nothing. Systems beat willpower every time.

The high cost of waiting is measured in hundreds of thousands—even millions—of dollars over a lifetime.

You don’t have a money problem. You have a procrastination problem.

And procrastination has a cure: Implementation.

Let us be your financial implementer. Like a personal trainer who shows up at 8 AM and makes sure you do the work, we make sure your financial plan gets executed.

No more excuses. No more “someday.” No more procrastination.

Today is the day.

Listen to the Full Podcast

Ready to hear the complete breakdown of how procrastination is costing you and exactly what to do about it? Listen to the full episode where I walk through real client examples, specific automation setups, and the exact systems that have worked for 40 years.

Listen to the full podcast episode: “The High Cost of Procrastination”

In this episode, I share the brutal math on waiting, break down all the income streams available in retirement, and explain exactly how our implementation process works. Plus, I’ll tell you about the client who went from procrastination to $1,500/month in automated savings in a single meeting.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.

Ready to stop procrastinating and start building wealth? Visit roymatlockjr.com to schedule your free consultation. We’ll implement your plan, set up automations, and get your money working for you. No more excuses. No more waiting. Let’s make 2025 the year you finally took control of your financial future.

Call us at (615) 843-2999 or visit roymatlockjr.com. Stop procrastinating. Start today.