How to Handle Inheritances the Right Way

Every single week, one of our clients passes away. It’s not morbid—it’s reality. The Great Wealth Transfer is here, and it’s massive.

Baby boomers and the Silent Generation will pass down an estimated $68 to $84 trillion in assets over the next few decades. That includes investments, real estate, retirement accounts, and businesses. The baby boomers alone hold 64% of all wealth in this country.

But here’s the sobering truth: without proper planning, inheritances can be lost to taxes, poor management, lawsuits, and family disputes. After 40 years in this business, I’ve seen it all—and today, I’m going to show you how to handle inheritances correctly, whether you’re leaving one behind or receiving one.

The Reality of Inheritances

The average anticipated inheritance is about $320,000—but that number is extremely skewed. Here’s the reality:

- Top 1%: Control 25% of all inherited wealth

- Bottom 50%: Get just 2.6%

For most people nearing retirement, the challenge isn’t leaving a massive estate—it’s figuring out how to survive their own retirement without becoming a burden.

The #1 Rule: Don’t Depend on Inheritances

My mother just turned 102 years old. She’s doing great. But think about this: I have sisters who are 11 to 17 years older than me. That means some of them are now 81 years old and haven’t received an inheritance yet.

Why you can’t rely on inheritances:

- People are living longer – Your parents might need every penny for their own care

- Healthcare costs are exploding – Long-term care can drain estates quickly

- Life is unpredictable – Divorces, lawsuits, bad investments can wipe out estates

- You need your own plan – Financial independence cannot depend on someone else dying

Even though trillions will change hands, there’s no guarantee you’ll get anything. That’s why you must plan for yourself and put your money to work now.

For Those Leaving an Inheritance: The Jar Story

Let me tell you a story that perfectly illustrates what happens without proper planning.

A man had a big jar on his mantle. Every night when he came home, he’d reach into his pocket and throw his quarters into the jar. Over time, the jar filled up with all those quarters—visible proof of his hard work and sacrifice.

People would visit and see the full jar. “Can you spare a quarter?” they’d ask. “Sure, go grab one,” he’d say.

One day, he looked at his jar. It was empty. People had taken all the money, and he was sad.

Think about that. Wouldn’t you be sad if you worked your entire life, built something meaningful, and then watched people take it without appreciation or understanding of the sacrifice it required?

Your role as the giver is to plan in advance so conflicts don’t arise. Your role as the receiver is to honor the legacy and steward the gift responsibly.

The Mindset of Receiving an Inheritance

Inheritances come from the passing of a loved one. You’re dealing with two conflicting emotions:

- Grief over losing someone you care about

- Sudden wealth you weren’t necessarily prepared for

First rule when you inherit money: CHILL.

Don’t move too quickly. You’re in an emotional state that’s not conducive to good decision-making. Slow down.

The First 90 Days: Collection Mode

The first three months after an inheritance should focus on gathering and protecting:

What to Collect

- Account statements from all financial institutions

- Legal documents (wills, trusts, deeds)

- Insurance policies

- Multiple death certificates (you’ll need more than you think)

- Business documents (if applicable)

What to Avoid

- Large purchases

- Hasty investment decisions

- Loaning money to friends and family

- Telling everyone about your inheritance

The Defense Against Takers

People will come out of the woodwork when they discover you’ve inherited money. The have-nots try to take from the haves—that’s just reality.

Your simple response: “My funds are managed by my financial advisor. Everything is tied up. If you really think you need something, you should call him.”

This deflects the request and puts a professional barrier between you and people trying to guilt you into bad decisions.

Assembling Your Professional Team

If you haven’t already, you need three key advisors:

- Fiduciary Financial Advisor – Someone legally required to act in your best interest (that’s what we do)

- Estate Attorney – To update or create wills, trusts, and legal documents

- Tax Professional – To minimize tax consequences and navigate complex rules

These professionals work together to protect your inheritance and help it grow responsibly.

Asset Allocation for Inherited Money

Once you’ve collected everything, organize assets by class:

- Stocks (growth)

- Bonds (stability)

- Cash (liquidity)

- Real estate (property)

- Business interests

Critical question: Should your allocation be the same as the person who left you the money?

Probably not. A 90-year-old retiree and a 45-year-old accumulator have completely different needs.

Dollar Cost Averaging for Lump Sums

When inheriting a large sum, we don’t dump it all into the market at once. We use dollar cost averaging over about 12 months.

Why? We don’t want to hope the market doesn’t go down or pray it goes up. We want to remove timing risk by entering the market gradually.

Investment Philosophy for Inherited Wealth

Resist Hot Tips and High-Pressure Pitches

When people know you have money, the pitches come fast and furious. Resist them.

Warning signs:

- “This opportunity won’t last!”

- “You’re going to miss out!”

- “My friend made 300% on this!”

- Anything promising guaranteed high returns with no risk

Get a Written Plan

Your plan should include:

- Risk tolerance assessment

- Timeline to retirement or major expenses

- Asset allocation strategy

- Tax optimization approach

Match Investments to Goals

If you’re checking the stock market every day and feeling anxious, you’re allocated incorrectly.

It’s like walking into the office every morning wondering, “Is my boss going to fire me today? Is my income secure?” That’s no way to live in retirement.

Proper allocation means you sleep well at night regardless of daily market fluctuations.

For Parents: Protecting Your Legacy

If you’re the one leaving money behind, here’s how to protect what you’ve built:

Keep Beneficiaries Updated

Common disasters I’ve seen:

Divorce scenario: Someone forgets to change beneficiaries after a divorce. They die, and the ex-spouse gets everything—even though they’d been remarried for 20 years.

No plan scenario: Second marriage, both with children. First spouse dies with no plan. Second spouse gets everything. Second spouse dies. Their children get everything. Original spouse’s children get nothing.

Adult child scenario: 40-year-old single son has an accident. Parents can’t make medical decisions because there’s no healthcare power of attorney. They have to go to court just to help their own son.

I could go on and on. These scenarios are preventable with proper planning.

Use Trusts to Control Distributions

Spendthrift Clauses are powerful tools. Here’s how they work:

“My children will receive 25% of their inheritance at my death. The remaining 75% will be managed by [advisor] and distributed after 10 years—or sooner if needed for education, medical emergencies, or home purchase.”

Why this matters: I don’t take a lot of advice from people in their twenties—not because they’re not smart, but because they haven’t had enough experience to learn from mistakes yet.

A spendthrift clause protects young heirs from making catastrophic financial decisions before they’re ready.

Special Needs Trusts

If you have a child who will never be able to manage money independently, a special needs trust ensures they’re cared for without disqualifying them from government benefits.

Discuss Your Plan Openly

The biggest gift you can give your heirs is clarity. Tell them:

- What your plan is

- Where documents are located

- Who your advisors are (introduce them)

- What your wishes are

This prevents confusion, reduces conflict, and ensures your legacy is protected.

Understanding Critical Account Types

POD and TOD Accounts

POD (Payable on Death) – Bank accounts that transfer directly to beneficiaries

TOD (Transfer on Death) – Brokerage accounts that transfer directly to beneficiaries

Benefits:

- Bypass probate

- Faster access to funds

- Privacy (not public record)

Limitation: These don’t work until you have death certificates—which can be delayed if there’s an autopsy or any question about cause of death.

Living Trusts vs. After-Death Documents

Here’s what people don’t realize: A living trust is called “living” because it operates while you’re alive. The moment you pass away, it’s no longer a living trust.

At death, you need:

- Death certificates (multiple copies)

- Executor or trustee to act

- Legal procedures to follow

New problem we’re seeing: Funeral homes (many now owned by private equity) won’t proceed without cash up front. But death certificates can be tied up for weeks if there’s an autopsy.

Solution: Beneficiary liquidity plans provide $25,000-$50,000 within 24-48 hours to handle immediate expenses while death certificates are processed.

For Business Owners: Succession Planning

Business transfers are one of the biggest parts of the wealth transfer—and one of the most complex.

The Partnership Problem

Imagine this scenario:

- You and your brother own a business 50/50 for 35 years

- You have two sons active in the business who will take over

- Your brother has one son with no interest (or worse, problems)

- Your brother dies

What happens? You’re now in business with people who are uninterested, unqualified, or problematic. Or you’re forced to buy them out when you don’t have liquidity.

Buy-Sell Agreements: The Solution

A buy-sell agreement funded with life insurance solves this:

- Each partner buys life insurance on the other (business is beneficiary)

- Agreement specifies business valuation method (usually average of two appraisals)

- When one partner dies, insurance pays out

- Money buys out deceased partner’s share

- Any excess owed is financed to the family

Additional considerations:

- Key person insurance (if one partner drives all the sales)

- Business continuity plans

- Qualified family members who want to continue

- Training succession candidates now

Real Estate Partnership Example

Two partners own properties together. They’ve worked them for decades. One partner dies.

Without a plan, the surviving partner is now in business with a spouse or children who might want to cash out immediately—forcing a sale at the worst possible time.

With a buy-sell agreement and proper insurance, the transition is smooth and planned.

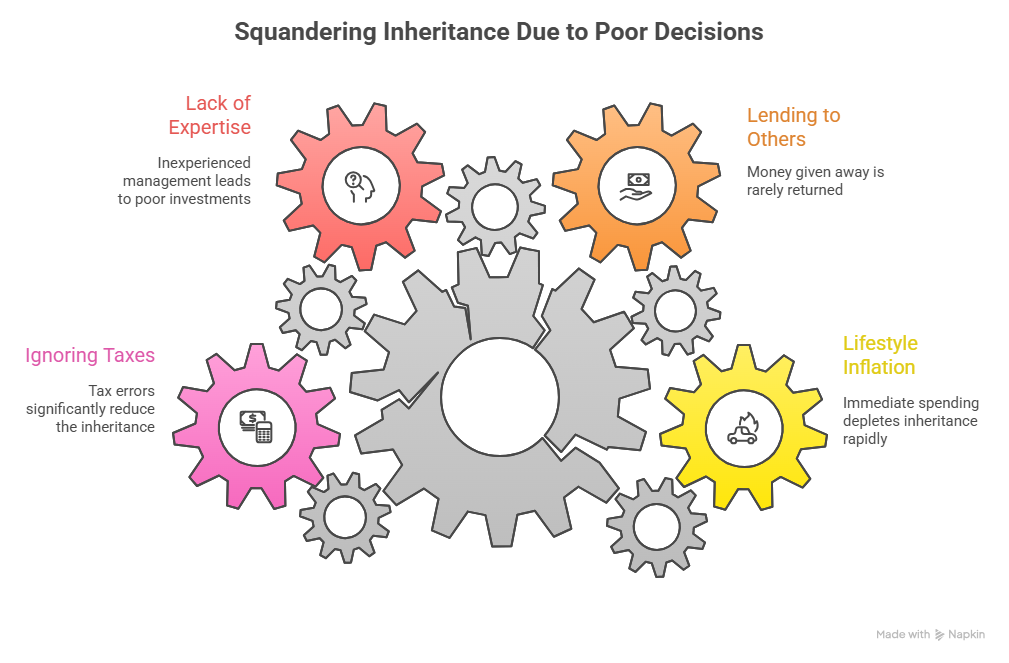

Squandering Inheritance Due to Poor Decisions

Common Inheritance Mistakes

Mistake #1: Immediate Lifestyle Upgrade

I had two schoolteachers come in after inheriting money. About a third was left—the other two-thirds went to two new Corvettes.

They were schoolteachers with no retirement savings. I was heartbroken.

Don’t do this. Just because money appears doesn’t mean your lifestyle should instantly inflate.

Mistake #2: Loaning to Family and Friends

“Can I borrow some money?” will become a constant refrain.

Remember: You’re honoring someone else’s sacrifice. That money wasn’t earned by the people asking for it. Protect it.

Mistake #3: No Professional Guidance

Trying to manage a large inheritance without expert help is like performing surgery on yourself. Technically possible, but incredibly risky.

Mistake #4: Ignoring Tax Consequences

Inherited IRAs have special rules. Different accounts have different tax treatments. One wrong move can cost you tens of thousands in unnecessary taxes.

Real-Life Success Story: My Mother

Forty-two years ago, my father sold his business. He and my mother were the same age. I had just entered the financial business.

We took proceeds from rental properties and started investing. We created a comprehensive plan including:

- Asset allocation appropriate for their age

- Wills and trusts

- Financial and healthcare powers of attorney

- Regular reviews and updates

My father passed away ten years ago. My mother just turned 102.

She has never worried about money. Not once.

Why? Because we took care of business from day one. We had a plan, we stuck to it, and we adjusted as life changed.

That’s the power of proper planning.

The Discipline of Wealth Building

Here’s what I’ve learned after 40 years: Accumulating money requires discipline over time.

It’s not luck. It’s education and action.

Find What You Love

Every successful person I know—from Nashville country music stars to NFL athletes to self-made millionaires—found something they love to do.

When you love what you do, it’s not a job. You naturally get good at it because you put time into it without resentment.

Survive the Feast and Famine

I’ve been through it all:

- Started making no money

- Built up to making a lot

- Hit 2002, 2007-2008 crashes (stock market tanked)

- Survived because I always saved during the good times

Many people didn’t survive those downturns. The difference? I had discipline and savings to weather the storms.

Be Proud of What You’ve Built

If you’ve accumulated wealth through hard work and sacrifice, be proud of it. Hold onto it. Don’t let guilt or pressure cause you to blow through what took decades to build.

And if you’re receiving wealth, don’t do anything embarrassing with it. Honor the sacrifice it took to create it.

Estate Planning Checklist

If you haven’t done this yet, schedule it now:

Essential Documents

- Living Trust

- Will (backup to trust)

- Healthcare Power of Attorney

- Financial Power of Attorney

- Living Will (end-of-life decisions)

- Beneficiary designations (all accounts)

For Business Owners

- Buy-sell agreement

- Business valuation method

- Key person insurance

- Succession plan

- Training next generation

Account Review

- List all assets (homes, accounts, property)

- Update all beneficiaries

- Review “all children equally” clauses (they may not work as intended)

- Set up POD/TOD accounts where appropriate

- Consider spendthrift clauses for young heirs

Taking Action Today

Whether you’re preparing to leave an inheritance or expecting to receive one, the time to act is now.

If You’re Building Wealth to Pass On:

Visit roymatlockjr.com to:

- Schedule a comprehensive estate planning review

- Set up trusts and legal documents

- Create buy-sell agreements (business owners)

- Introduce your heirs to your advisors

- Plan family financial workshops

If You’re Inheriting Money:

- Take 90 days to collect and organize

- Assemble your professional team

- Resist pressure and hot tips

- Create a written plan

- Honor the legacy through responsible stewardship

For Everyone:

Don’t depend on inheritances for your own financial security. Build your own wealth through:

- Paying yourself first (automate savings)

- Maximizing retirement accounts (tax advantages)

- Finding work you love (natural motivation)

- Living below your means (discipline over time)

The Bottom Line

The Great Wealth Transfer represents the largest movement of assets in human history. But without proper planning, this wealth can vanish in a single generation through taxes, poor decisions, and family conflicts.

I’ve spent 40 years helping people protect what they’ve built and steward what they’ve received. The principles don’t change:

For givers: Plan ahead. Protect your legacy. Educate your heirs.

For receivers: Honor the sacrifice. Get professional help. Make wise decisions.

For everyone: Don’t wait for an inheritance to build your own financial security.

The jar can fill up with quarters over a lifetime, or it can be emptied by thoughtless hands in a moment. Which story will yours be?

Listen to the Full Podcast

Want to hear more real-life stories, detailed estate planning strategies, and business succession examples? Listen to the complete episode where I share 40 years of experience helping families navigate the complex world of inheritances.

Listen to the full podcast episode: “The Great Wealth Transfer”

In this episode, I share specific case studies of inheritance disasters, the exact documents you need in place, and how to set up buy-sell agreements that protect your business. I also discuss family financial workshops and how to educate the next generation while you’re still here to guide them.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.