The Retirement Red Zone: 7 Steps to a Confident Retirement Game Plan

As you approach the last five to ten working years, the rules change. You’re switching from the “growth at all costs” phase to preserve, position, and pay yourself. That final stretch is what Roy Matlock Jr. calls the Retirement Red Zone — close to the goal line, where a few smart decisions can carry you across, and a few mistakes can push you back yards.

Below is a practical blueprint you can put to work now: seven steps that integrate taxes, risk, guaranteed income, long-term care, final expenses, Social Security timing, and estate planning. Use this as a checklist, bring it to your annual review, and adjust as your life and the markets evolve.

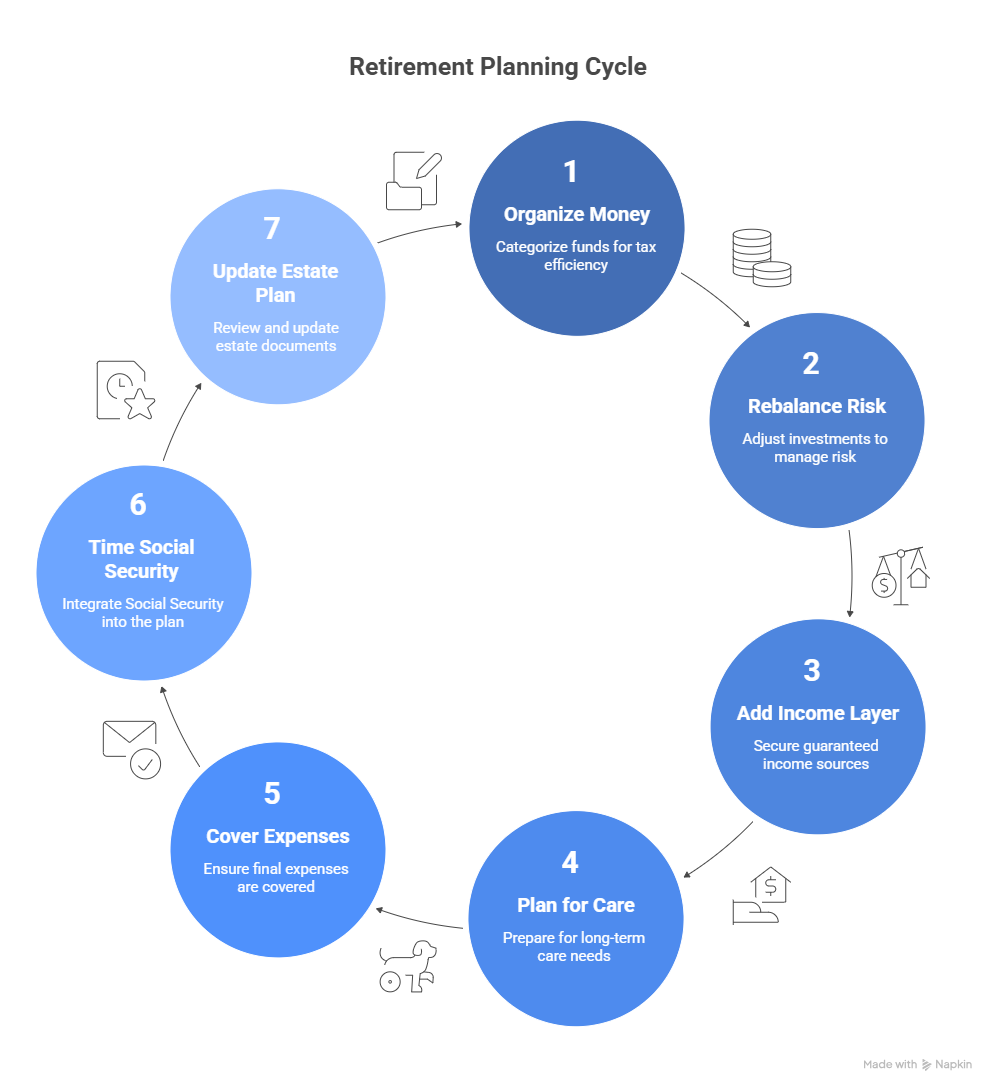

Retirement Planning Cycle

Step 1: Organize Money by Tax Buckets

Why tax buckets matter: Retirees don’t just need income — they need tax-efficient income. Arranging assets into buckets helps control lifetime taxes, reduce how much of your Social Security is taxable, and create flexibility year by year.

Three core buckets to set up now:

-

Taxable bucket: Checking, savings, brokerage, and rental income. You’ll pay taxes on interest/dividends/gains as you go, but you gain liquidity and flexibility. In early retirement, drawing principal here can help keep adjusted gross income low — useful when coordinating IRMAA thresholds, Roth conversions, or capital gains harvesting.

-

Tax-deferred bucket: 401(k), 403(b), traditional IRA. You got a deduction on the way in; withdrawals are taxed as ordinary income later. This bucket is powerful, but unmanaged balances can balloon into higher RMDs and larger tax bills in your 70s and 80s.

-

Tax-free bucket: Roth IRA (plus certain properly structured life-insurance-based strategies). Qualified withdrawals are tax-free, which gives you control in down markets or high-tax years.

Action items in the red zone:

-

Map current balances by bucket.

-

Run a multi-year withdrawal and conversion plan (not just one year).

-

Consider partial Roth conversions in lower-income years or in the gap between retirement and RMD age.

-

Coordinate harvesting in the taxable bucket with your bracket management.

Step 2: Rebalance by Risk Buckets to Manage Sequence Risk

The risk you must respect: A string of poor returns early in retirement (while you’re taking withdrawals) can do disproportionate damage — the classic sequence-of-returns risk.

Build three risk buckets:

-

Conservative: Cash, T-bills, short-duration bonds, and money markets to fund near-term income needs. This is your buffer when markets stumble.

-

Moderate: Balanced funds, quality core bonds, or certain indexed annuities. This aims for steadier returns without giving up growth entirely.

-

Aggressive: Equity and growth assets for long-term inflation protection. You likely still need a growth engine for a 25–30+ year retirement.

Action items in the red zone:

-

Set aside 1–3 years of expected withdrawals in the conservative bucket.

-

Use the moderate bucket as a bridge for 3–7 years.

-

Keep a measured portion in growth for years 8+ to fight inflation.

-

Refill conservative assets from growth after up years; avoid selling stocks low to fund lifestyle.

Step 3: Add a Guaranteed Income Layer

Why guarantees help: Fixed expenses (housing, utilities, groceries, insurance) are easier to carry when they’re matched to guaranteed income streams. That’s less pressure on your investment portfolio, especially in choppy markets.

Core sources to consider:

-

Social Security: Your base lifetime income.

-

Pensions: If you have one, evaluate single vs. joint options and survivorship features.

-

Annuities: A way to convert a portion of savings into a personal pension. Options range from fixed annuities (principal protection) to fixed indexed annuities (principal protection with upside caps) to variable/RILA structures (more market linkage with guardrails and income riders).

Action items in the red zone:

-

Calculate your essential monthly number (core bills only).

-

Cover that number with Social Security + pension + annuity income where possible.

-

Leave investment accounts to handle discretionary spending and future inflation.

Step 4: Plan for Long-Term Care Before It’s Urgent

The reality to plan for: Roughly 7 in 10 retirees will need some form of long-term care — from in-home assistance to assisted living or skilled nursing. One spouse’s care can strain a household budget quickly.

Coverage frameworks:

-

Traditional LTC insurance: Pay premiums for a pool of LTC benefits.

-

Hybrid life + LTC riders: Permanent life insurance that can accelerate benefits for qualifying care needs.

-

Asset-based annuities with LTC multipliers: A lump sum can create a multiple of coverage for care, acting like a large deductible followed by insurer benefits.

Action items in the red zone:

-

Decide whether you’re transferring risk (insurance) or self-funding (assets).

-

If insuring, underwriting is generally easier in your 50s/early 60s; don’t wait until health issues appear.

-

Coordinate with your spouse’s plan to protect household cash flow if one of you needs extended care.

Step 5: Cover Final Expenses and Protect Survivors

Costs to anticipate: End-of-life care and burial can run into the tens of thousands. Additionally, a surviving spouse may see income fall (e.g., one Social Security benefit drops off) while some expenses continue.

Practical protection:

-

Term life during working years for income replacement.

-

Permanent life later for legacy and to handle final expenses efficiently.

-

Beneficiary reviews to prevent expensive mistakes and delays.

Action items in the red zone:

-

Re-run survivor income projections (mortgage, utilities, medical, taxes).

-

Right-size life coverage: enough to keep the survivor financially stable without over-insuring.

-

Confirm beneficiaries across all accounts; align them with your estate plan.

Step 6: Time Social Security with the Whole Plan (Not in Isolation)

It’s not only “when,” it’s “how it fits”: Filing early reduces the monthly check; delaying to 70 raises it. But the best choice depends on health, work status, taxes, spousal coordination, and portfolio structure.

Common patterns we see:

-

If still working near full retirement age (≈67), many households claim and invest the benefit, or delay strategically if the numbers favor it.

-

Coordinating spousal benefits can raise lifetime household income.

-

Smart timing can also reduce the years your benefit is exposed to taxation or IRMAA surcharges.

Action items in the red zone:

-

Run a household-level Social Security analysis (not just individual).

-

Overlay tax projections, Roth conversion windows, and portfolio withdrawals.

-

Revisit annually; one change (inheritance, job, health) can alter the optimal choice.

Step 7: Update Your Estate Plan and Paperwork (Every 2–3 Years)

Documents that do real work:

-

Will or Revocable Living Trust to direct assets efficiently and privately.

-

Financial Power of Attorney so someone you choose can act if you can’t.

-

Health-Care Proxy/Directives to guide medical decisions and reduce family stress.

-

Beneficiary Designations that supersede wills on retirement accounts and life insurance.

Common pitfalls to correct now:

-

Out-of-date beneficiaries (ex-spouse still listed, grandchildren unintentionally excluded).

-

No contingent beneficiaries (causes delays and probate involvement).

-

Titling mismatches (assets titled inconsistently with the trust/plan).

-

Adult children away at college without a health-care proxy on file.

Action items in the red zone:

-

Organize a single “Where Everything Lives” file (digital and physical).

-

Confirm per stirpes vs. per capita choices align with your intent.

-

Share the high-level plan with your trusted contacts so they can execute calmly if needed.

How the Pieces Work Together

A durable retirement plan combines defense and offense:

-

Defense: Insurance (health, life, disability where applicable, LTC), emergency cash, proper titling and documents, tax-smart bucket management, and a withdrawal policy that avoids selling risk assets after big drops.

-

Offense: A calibrated growth sleeve to outpace inflation, deliberate Roth conversion timing, and disciplined rebalancing that skims gains in good years to refill your conservative bucket.

Think of your annual review as your “game film.” Measure what changed (markets, taxes, health, income), update allocations, confirm your guaranteed income is covering essentials, and rebalance risk so one bad quarter doesn’t derail the next decade.

Quick Checklist for the Retirement Red Zone

-

Inventory every account by tax bucket (taxable/deferred/free).

-

Segment investments by risk bucket (conservative/moderate/aggressive).

-

Match guaranteed income to essential expenses.

-

Decide LTC approach: insure vs. self-fund (or a blend).

-

Right-size life insurance for survivor needs and final expenses.

-

Run a household Social Security analysis (with tax overlays).

-

Refresh estate documents and beneficiaries; centralize key info.

-

Set 1–3-year cash buffer and define a refill rule after up markets.

-

Schedule an annual strategy session; treat it like a financial physical.

Listen to the Full Podcast

Want to hear Roy explain how to prepare for retirement in the critical years before you stop working?

🎧 Listen to the complete episode here.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.