Why People Go Broke in Retirement: Complete Financial Plan

There are two distinct phases of your financial life: accumulation (building wealth) and withdrawal (living on that wealth in retirement). Most people understand the accumulation phase reasonably well—save money, invest it, watch it grow.

But here’s where people fail: the withdrawal phase is far more complicated, and the mistakes you make here can destroy decades of careful saving in just a few years.

After 40 years of advising people, I’ve identified the exact mistakes that cause people to go broke in retirement—and more importantly, how to avoid them. Today, I’m giving you the complete blueprint for both phases of your financial life.

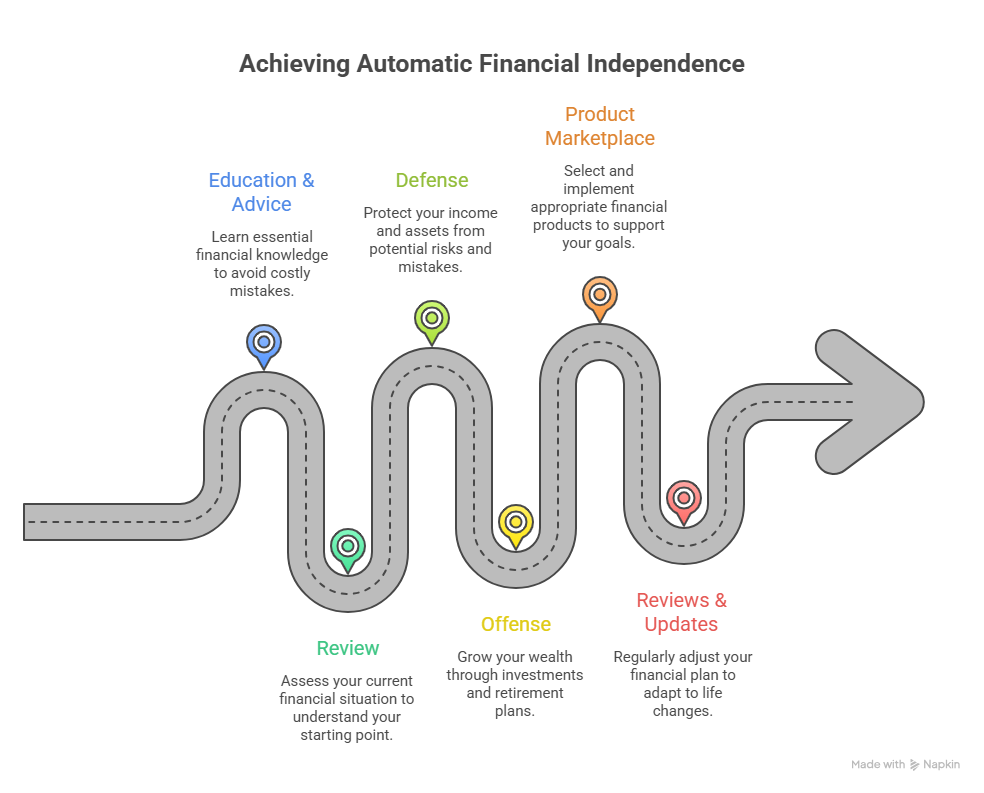

The Foundation: Six Components of Automatic Financial Independence

Everything I do is built around a system I call the Six Components of Automatic Financial Independence:

- Education & Advice – Learn what you don’t know (because what you don’t know WILL cost you)

- Review – Assess where you are today (what you have, what you owe, what you earn)

- Defense – Protect income and assets (avoid costly mistakes)

- Offense – Grow your wealth (investments, retirement plans, compound interest)

- Product Marketplace – Place appropriate financial products (insurance, investments, mortgages)

- Reviews & Updates – Adjust as life changes (money in motion)

The result: If you follow this system consistently, you’ll see progress. Guaranteed.

Achieving Automatic Financial Independence

Phase 1: Accumulation – Building Wealth

The GPS System: Your Navigation for Financial Independence

I read “Think and Grow Rich” 40 years ago. Page 36 changed my life. It explains how to turn desires into riches through a written plan that programs your subconscious mind.

Here’s your GPS:

G = Goal

Two critical goals you need:

- Income Goal: What do you make now? What do you want to make? How will you get there?

- Financial Independence Number: Multiply your desired annual retirement income by 20

Example:

- Need $100,000/year in retirement

- $100,000 × 20 = $2 million

- At 5% return, $2 million generates $100,000 annually forever

P = Plan

From your goal to your plan:

- How much must you save monthly?

- What rate of return do you need?

- Which accounts will you use?

- What’s your tax strategy?

S = Schedule

When will you reach your goal? 10 years? 20 years? 40 years?

Real story: In 1986, I wrote down my 10-year goals—income targets, savings amounts, everything. Having that schedule created accountability and motivated my subconscious to make it happen.

The Brutal Math of Procrastination

Let me show you exactly what waiting costs:

Scenario: $500/month invested at 10%

| Years Invested | Total Accumulated |

|---|---|

| 20 years | $347,000 |

| 30 years | $995,000 |

| 40 years | $2,700,000 |

By waiting 10 years (starting at 30 instead of 20):

- Cost: $2,700,000 – $995,000 = $1.7 million lost

By waiting 20 years (starting at 40 instead of 20):

- Cost: $2,700,000 – $347,000 = $2.35 million lost

You’re side-by-side with your buddy. Same job. Same income. Only difference: one has $500/month automatically deducted into investments. The other doesn’t.

40 years later:

- Your buddy: $0 (or still working)

- You: $2.7 million (financially independent)

Procrastination will kill your financial future. Start NOW. Not next year. Not next month. TODAY.

The Power of Rate of Return

Time isn’t the only factor. WHERE you invest matters dramatically.

Same $500/month, same 40 years:

| Return Rate | Total Accumulated |

|---|---|

| 6% | $900,000 |

| 10% | $2,700,000 |

Difference: $1.8 million

Getting your money out of the bank and into proper investments triples your outcome.

Over 30 years:

- 6%: $477,000

- 10%: $995,000

- Difference: 100% more wealth

The lesson: You need professional money management, not savings accounts.

Top 10 Accumulation Mistakes (And How to Avoid Them)

Mistake #1: Living Beyond Your Means

Test: How much have you saved vs. how much do you owe?

If you owe more than you’ve saved, you’re spending more than you make.

Bad debt:

- High interest rates (credit cards at 21%)

- Tied to depreciating assets (cars, consumer goods)

Good debt:

- Easily affordable

- Tied to appreciating assets (home, business equipment)

Mistake #2: Procrastination (Not Starting Early)

We already showed the math. Every year you wait costs hundreds of thousands.

Action: Set up automatic deductions TODAY. Even $100/month beats $0/month.

Mistake #3: Failing to Take Employer Match

This is free money.

Typical 401(k) match:

- You contribute 6%

- Employer matches 3%

- Instant 50% return on your money

- Plus tax deduction

I see people all the time not even contributing to their 401(k). It’s leaving tens of thousands on the table.

Mistake #4: Chasing Hot Investments

Observation: The people with the least money have the most Bitcoin.

Why? Because they think they’ll get rich without working, saving, and giving it time.

I’m not anti-Bitcoin. But I can’t value it. I can value a business. If my business earns $100,000/year and you offer me $100,000 to buy it, no deal. Offer me $1 million (10 years of earnings)? I’ll consider it.

Stick to what you can value: Stocks in real companies with real earnings.

Mistake #5: Ignoring Asset Allocation

Asset allocation = where you invest (stocks, bonds, cash, etc.)

Accumulation phase (young):

- Aggressive growth funds

- Want market to go DOWN so you buy at discounts

- Long time horizon to recover from dips

At/near retirement:

- More conservative allocation

- Want market stability

- Can’t afford major drops when withdrawing

Mistake #6: No Emergency Fund

Emergency fund (3-6 months of expenses) prevents:

- Borrowing at 20% credit card rates

- Raiding retirement accounts (penalties + taxes)

- Selling investments at market lows

Bonus: Lets you raise insurance deductibles and cut premiums.

Mistake #7: Not Protecting Income

Two critical insurances:

Term Life Insurance

- Low cost, high coverage

- Protects income for your family

- Rule of thumb: 10x annual income

- New feature: Living benefits (access 90% of death benefit if critically ill)

Cost for 30-35 year old: Less than $100/month for $1 million coverage

Disability Income

- Replaces 60-70% of income if you can’t work

- Available through work or individual policies

Think about this: If you don’t protect income and something happens, everything else collapses.

Mistake #8: No Written Plan

Without a written plan, hitting your goals is an accident.

Write down:

- Income goal and steps to achieve it

- Financial independence number

- Monthly savings target

- Timeline

Your subconscious will work toward written goals automatically.

Mistake #9: Poor Investment Selection

Story: I had someone with their 401(k) in five different funds. Looked diversified, right?

Wrong. All five funds owned the same companies. No real diversification.

Proper diversification:

- Small-cap stocks

- Mid-cap stocks

- Large-cap stocks

- International stocks

- Bonds (as you age)

Simple allocation for accumulators:

- 25% small-cap

- 25% mid-cap

- 25% large-cap

- 25% international

Want more conservative? Add balanced fund or bonds.

Want more aggressive? Remove large-cap, increase small-cap.

Mistake #10: Not Understanding Professional Money Management

Here’s the story I’ve used a thousand times:

Become an Owner, Not a Loaner

The Bank Scenario:

You walk in with $1,000 cash (ten $100 bills).

You: “I’d like to open a savings account.”

Bank: “We pay 2% interest.”

You: Hand over your money

Next person in line:

Customer: “I want a car loan.”

Bank: “13% interest.”

Next person:

Customer: “I want a credit card.”

Bank: “21% interest.”

Who makes more money—you at 2% or the bank?

The bank borrows from you at 2%, loans it out at 13-21%, and makes the spread.

Better idea: OWN the bank. Buy bank stock.

The Starbucks Example

I go to Starbucks every morning. Every second, millions of transactions happen worldwide at Starbucks locations.

Question: Will you make more money loaning to a bank at 2% or owning Starbucks stock?

Answer: Own Starbucks.

How to Become an Owner

Problem: You don’t know which stocks to buy.

Solution: Hire professional money managers (mutual funds, ETFs).

Professional managers:

- Research companies full-time

- Diversify across industries, sectors, countries

- Monitor markets constantly

- Have teams of analysts

Your $500/month gets the same expertise as someone investing $100 million.

The Real Estate Reality Check

I had a lady this week buying rental properties.

Her: “It’s passive income!”

Me: “No, it’s not.”

Passive income: Money deposited in your account monthly while you do nothing.

Rental income: You advertise, rent, maintain, repair, manage tenants, sign leases, collect rent, evict non-payers.

Rentals are great investments—but they’re NOT passive.

True passive income = mutual funds, money managers doing everything while you sleep.

Phase 2: Retirement – The Withdrawal Phase (Where Most People Fail)

Accumulation is relatively simple: automate savings, invest properly, protect income, wait.

Retirement is FAR more complicated. Here’s where people go broke.

Retirement Mistakes and Solutions

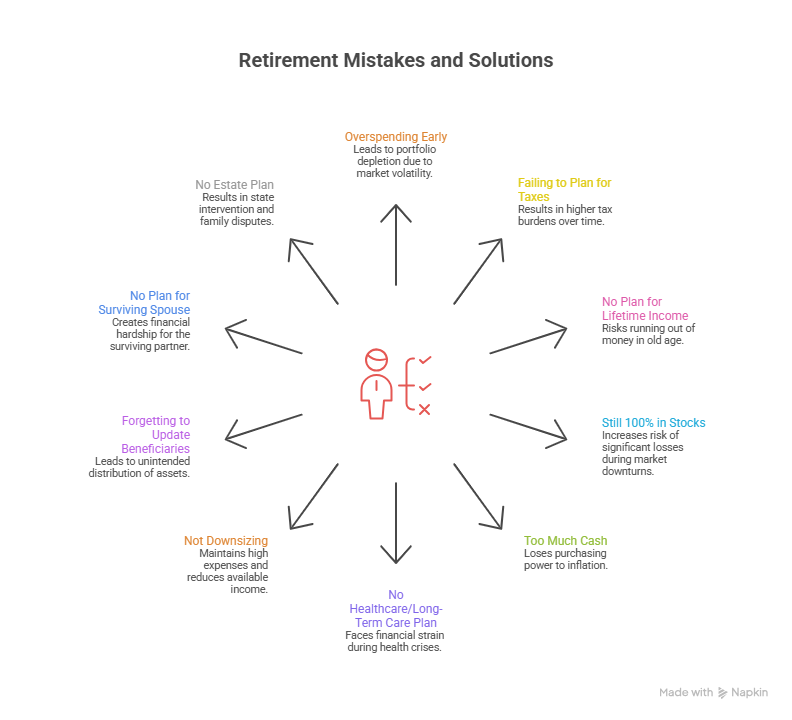

Top 10 Retirement Mistakes (The Ones That Destroy You)

Mistake #1: Overspending Early (Sequence of Return Risk)

You’re used to a paycheck. You retire. Spending continues at the same pace.

Problem: If markets drop early in retirement while you’re withdrawing heavily, you can permanently damage your portfolio’s ability to recover.

This is called sequence of return risk—the ORDER of returns matters in retirement, not just the average.

Solution: Budget carefully in early retirement years. Don’t go wild just because you have a lump sum.

Mistake #2: Failing to Plan for Taxes

Most people miss this entirely.

When I meet with retirees, they have multiple income sources:

- Social Security

- 401(k) rollovers (taxable)

- Roth IRAs (tax-free)

- Taxable brokerage accounts

- Annuities

- Life insurance cash value

Question: Which do you withdraw from first? The answer determines how much you pay in taxes over 20-30 years.

Strategic Withdrawal Order Example

Client scenario:

- Social Security: $5,000/month

- Need: $8,000/month total

- Gap: $3,000/month

- Has: $100,000 in bank savings

My strategy:

Years 1-3: Withdraw $3,000/month from the $100,000 savings.

Why? It’s mostly return of principal. Minimal tax. Avoids:

- Taxation on Social Security

- Higher Medicare premiums

- Forced RMDs (Required Minimum Distributions)

Years 4-6: Withdraw from Roth IRAs (tax-free).

Meanwhile: Convert traditional IRA funds to Roth during low-income years. Pay taxes now at lower rates, avoid bigger taxes later.

Result:

- Social Security remains untaxed (or minimally taxed)

- Medicare premiums stay low

- RMDs reduced through conversions

- Tax-free Roth withdrawals for life

This strategy saves tens of thousands in taxes over retirement.

The Reverse Mortgage Strategy

Another client scenario:

- $800,000 house (too big, hard to maintain)

- Sold house, bought $400,000 condo

Option 1: Pay cash for condo ($400,000), invest $400,000

Option 2 (What we did):

- Put $200,000 down on reverse mortgage

- $200,000 reverse mortgage (no payment)

- $600,000 cash available

Result: $600,000 generating income instead of tied up in the house.

Reverse mortgages can also fund:

- Roth conversions

- Long-term care reserves

- Emergency access to home equity

Mistake #3: No Plan for Lifetime Income (Outliving Your Money)

My mother is 102 years old. The best part? She didn’t run out of money at 85.

The biggest retirement fear: Running out of money when you’re too old to do anything about it.

Solution: Create guaranteed income streams

- Social Security (guaranteed for life)

- Pension (if you have one—rare these days)

- Annuities with lifetime income riders (you can’t outlive them)

- Systematic withdrawal plans from investments

The goal: Never run out. Ever.

Mistake #4: Still 100% in Stocks at Retirement

I see this constantly.

Someone retires with $1 million—100% in aggressive growth stocks.

Problem: Market drops 30%. Now they have $700,000. They’re withdrawing $50,000/year. They’re selling at huge losses to fund living expenses.

This accelerates portfolio depletion.

Solution: The Four-Bucket System

The Four-Bucket Retirement Strategy

This keeps you happy whether markets go up OR down.

Bucket 1: Cash/Money Market (1-2 years of expenses)

- Immediate access

- No market risk

- Use when markets are down

Bucket 2: Bonds/Fixed Income (3-7 years of expenses)

- More conservative than stocks

- Better returns than cash

- Low correlation to stock markets

Bucket 3: Stocks (8+ years out)

- For inflation protection

- Long-term growth

- Can ride out volatility

Bucket 4: Annuities (Lifetime guaranteed income)

- Can’t outlive it

- Predictable income

- Reduces longevity risk

How it works:

- Market up? Withdraw from stocks (sell high)

- Market down? Withdraw from bonds/cash, let stocks recover (don’t sell low)

- Always: Base income from annuities/Social Security

Result: You spend without panic. You’re confident in any market.

Mistake #5: Too Much Cash

If you have more than 6 months of expenses in cash, you’re losing money to inflation.

Example: $200,000 sitting in bank at 2%.

At 3% inflation, you’re losing 1% per year in purchasing power = $2,000/year.

Over 20 years: $40,000+ lost to inflation

Better strategy: Dollar-cost average into investments over 6-12 months. Get that money working.

Mistake #6: No Healthcare/Long-Term Care Plan

The two biggest retirement fears:

- Running out of money

- Going into a nursing home

Options for long-term care:

Hybrid Life Insurance with LTC Riders

- Pay premiums during working years

- If you need long-term care, rider pays benefits

- If you don’t need it, heirs get death benefit

Annuities with LTC Riders

- Guaranteed income for life

- Enhanced benefits if you need nursing home care

Self-insure with Reverse Mortgage

- Tap home equity if care is needed

- Preserve investment accounts

Mistake #7: Not Downsizing When It Makes Sense

$800,000 house → $400,000 condo = $400,000 freed up for income.

Don’t stay in a too-large, too-expensive house out of stubbornness.

Mistake #8: Forgetting to Update Beneficiaries

Horror story: Client divorced. Died 10 years later. Never updated beneficiaries. Ex-wife got the entire 401(k) even though he’d remarried.

Another: “All children equally” clause. One child died. Their kids (the grandchildren) got nothing because of how it was worded.

Check beneficiaries:

- After divorce/remarriage

- After births/deaths

- Every 3-5 years minimum

Mistake #9: No Plan for Surviving Spouse

When one spouse dies:

- Lose one Social Security payment

- May lose pension income

- Living expenses don’t drop by 50%

Solution: Permanent life insurance that pays death benefit to surviving spouse, replacing lost income.

Mistake #10: No Estate Plan

62% of Americans have NO:

- Will

- Trust

- Financial Power of Attorney

- Healthcare Power of Attorney

What happens without these:

- State decides who gets your assets

- Courts appoint guardians

- Probate eats 5-10% of estate

- Family fights destroy relationships

Not complicated if:

- Married once, stayed married

- Kids together

- No business/partners

- Modest estate

Very complicated if:

- Second marriages with kids from both sides

- Business partners

- Significant assets

Dollar-Cost Averaging for Retirees

If you retire with a lump sum (401(k) rollover, inheritance, sold business), don’t dump it all into the market at once.

Why? If the market drops right after, you just lost 20-30% immediately.

Better: Dollar-cost average over 6-12 months.

Example:

- $500,000 lump sum

- Invest $40,000-$50,000 per month over 10-12 months

- Smooths out market volatility

- Removes timing risk

The Complete Plan: Putting It All Together

Accumulation Phase (Building Wealth)

- Set GPS (Goal, Plan, Schedule)

- Protect income (term life, disability)

- Automate savings ($500/month minimum)

- Professional money management (mutual funds, diversification)

- Max employer match (free money)

- Build emergency fund (3-6 months)

- Avoid bad debt (credit cards, depreciating assets)

- Increase income (skills, education, career moves)

Retirement Phase (Preserving & Withdrawing)

- Four-bucket system (cash, bonds, stocks, annuities)

- Tax-efficient withdrawals (minimize taxation over lifetime)

- Guaranteed income (Social Security + annuities)

- Update allocations (more conservative than accumulation)

- Plan for healthcare (LTC riders, reverse mortgage backup)

- Don’t overspend early (sequence of return risk)

- Update beneficiaries (after life changes)

- Estate planning (will, trust, powers of attorney)

The Six-Component System in Action

1. Education & Advice

When we’re done working together, you’ll be able to explain your plan to your best friend at lunch. That’s real understanding.

2. Review

We assess:

- What do you have?

- What do you owe?

- What do you earn?

- What are your goals?

3. Defense (Protect Income & Assets)

- Life insurance (term + permanent)

- Disability income

- Health insurance

- Property & casualty

- Umbrella liability

4. Offense (Grow Wealth)

- Retirement plans (401k, IRA, Roth)

- Professional money management

- Asset allocation

- Diversification

5. Product Marketplace

As fiduciaries, we access 9,000+ investment options and multiple insurance carriers. We’re not tied to one company—we find what’s best for YOU.

6. Reviews & Updates

Life changes (money in motion):

- Marriage/divorce

- Kids/grandkids

- Job changes

- Deaths

- Retirement

We adjust the plan as your life evolves.

Taking Action Today

Whether you’re accumulating or approaching retirement, the time to act is NOW.

For Accumulators:

- Set up automatic $500/month deduction (minimum)

- Max employer 401(k) match

- Get term life insurance (under $100/month)

- Write down GPS (Goal, Plan, Schedule)

For Retirees:

- Implement four-bucket strategy

- Plan tax-efficient withdrawals

- Set up guaranteed income streams

- Update estate documents

For Everyone:

- Download budget forms at RoyMatlockJr.com

- Schedule free consultation (615-843-2999)

- Watch monthly webinars (educational, not sales)

- Search our podcast library (200+ episodes)

The Bottom Line

Accumulation is about time and consistency. Start early, invest properly, protect income, let compound interest work.

Retirement is about strategy and preservation. Wrong moves here destroy decades of saving in just a few years.

Most people fail in retirement because they treat it like accumulation. It’s not. It’s far more complex.

That’s why you need a fiduciary advisor who implements complete plans—not just someone who sells you products.

After 40 years and working with thousands of clients, I can tell you: The system works. But you have to work the system.

Are you ready to build your plan?

Listen to the Full Podcast

Want to hear more detailed examples of retirement strategies that work (and disasters that don’t)? Listen to the complete episode where I walk through real client scenarios.

Listen to the full podcast episode: “Most People Fail Here and Go Broke in Retirement”

In this episode, I share the exact withdrawal strategies that saved clients hundreds of thousands in taxes, explain how my 102-year-old mother never ran out of money, and detail the reverse mortgage strategy that freed up $600,000 for one client. Don’t miss these real-world examples.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.