podcast

Second Opinion on Your Money: Find $50K-$500K Blind Spots

I recently saved someone’s life by performing the Heimlich maneuver at a restaurant. The scary part? I didn’t even know how to do it correctly—I just got lucky. After it happened, I Googled it to see what I was supposed to do.

Here’s the connection to your money: Just like that choking incident, financial emergencies happen when you least expect them. And just like I brought in an expert to demonstrate the proper technique at our next webinar, you need experts to help you avoid financial disasters before they happen.

After working with over 40,000 clients since 1985, I can tell you this with absolute certainty: A typical financial mistake costs between $50,000 and $500,000 over your lifetime. And most people are making these mistakes right now without even knowing it.

The $500,000 Mistake: How It Happens

Let me show you the math on how one mistake compounds into half a million dollars lost.

You and your buddy both make the same income. Here’s what happens:

Your Buddy (Makes Mistakes Early)

- Makes financial mistakes for 10 years

- Can’t save $500/month

- Finally digs out of the hole at year 10

- Has $0 saved

You (Gets It Right from the Start)

- Saves $500/month for 10 years

- Invests properly, money doubles

- Has $100,000 at year 10

Next 10 years (Both now saving $500/month):

- Your buddy: Adds $100,000 → Total: $100,000

- You: Your original $100,000 doubles to $200,000, plus new $100,000 → Total: $300,000

- Gap: $200,000

Next 10 years:

- Your buddy: Another $100,000 → Total: $200,000

- You: Your $300,000 doubles to $600,000, plus new $100,000 → Total: $700,000

- Gap: $500,000

Same income. Same effort now. But those early mistakes? $500,000 difference.

That’s why you need a second opinion—to catch these mistakes before they compound.

Why People Avoid Financial Second Opinions

Here’s what’s interesting: We have no problem getting second opinions on medical issues. Walk into a doctor’s office and we tell them everything—highly personal information in private settings.

But when it comes to money? People clam up. They don’t want anyone knowing their financial situation. They’re embarrassed. They’re private. They avoid help.

The result: They go through life making $50,000-$500,000 mistakes that could have been prevented with a simple conversation.

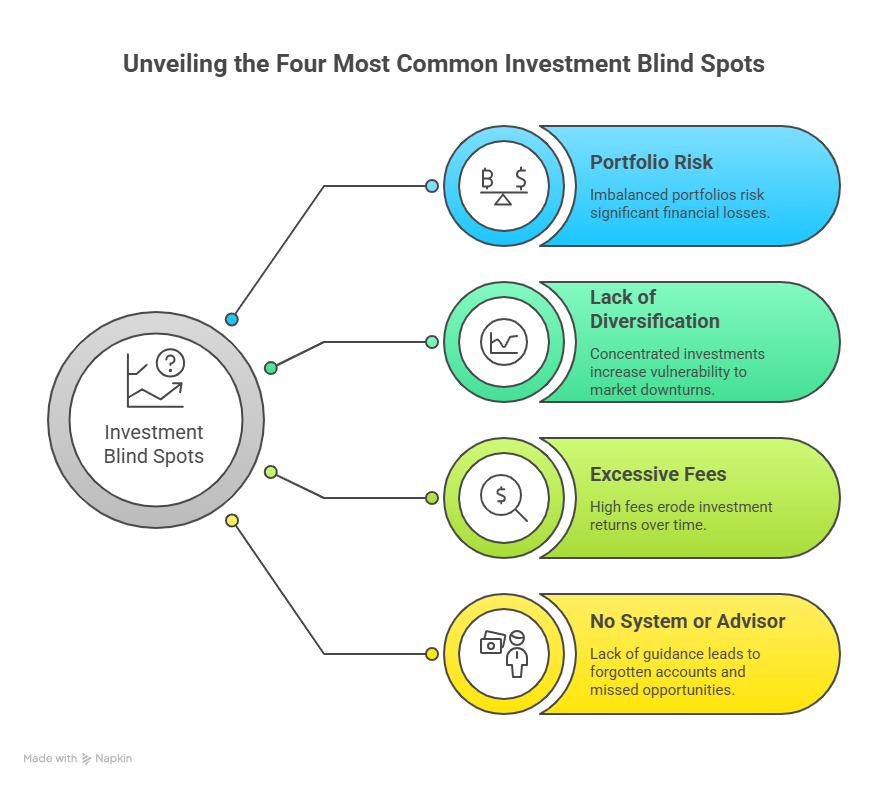

Unveiling the Four Most Common Investment Blind Spots

The Four Most Common Blind Spots

After reviewing tens of thousands of portfolios, I see the same four blind spots repeatedly:

Blind Spot #1: Portfolio Too Risky or Too Conservative

Too Conservative Example:

A person came in who left their 403(b) at a previous employer 20 years ago. It sat in a “guaranteed” account earning minimal interest.

Cost: We calculated they lost $200,000 in potential growth.

Another example: Someone had $300,000-$400,000 in their 401(k)—they weren’t even sure which. Why? They’d left it behind at a previous job, unmanaged and forgotten.

Too Risky Example:

Someone at or near retirement with 100% stocks, no bonds, no guaranteed income. One market crash could devastate their retirement plans.

The fix: Proper asset allocation based on your age, timeline, and risk tolerance.

Blind Spot #2: All Eggs in One Basket (No Real Diversification)

I reviewed a portfolio yesterday with five different funds. Looked diversified, right?

Wrong. All five funds owned the same stocks. It appeared diversified because of different fund names, but it was concentrated risk.

Other concentration issues I see:

- No international diversification (100% U.S. stocks)

- Entire 401(k) in company stock

- All real estate, no liquid investments

- All bonds when inflation is rising

The fix: True diversification across asset classes, geographies, and investment types.

Blind Spot #3: Excessive or Hidden Fees

Over 30 years, I’ve worked with investment groups that spend more on research than anyone else while maintaining some of the lowest expenses in the industry.

Why does this matter? Because every 1% in fees costs you massive amounts over time.

Example:

- $500,000 portfolio

- 2% total fees (advisor + fund expenses)

- Over 20 years: $200,000+ in fees

The fix: Low-cost index funds or actively managed funds with institutional pricing. We clear through major firms with access to 9,000+ investment choices—like opening an Amazon account for investments.

Blind Spot #4: No System, No Advisor, Left to Hang

The biggest blind spot of all: Going it alone without professional guidance or a systematic approach.

What I see:

- Forgotten 401(k)s at old employers (some companies no longer in business)

- “Orphan accounts” where the advisor retired and no one took over

- No beneficiary updates after divorce or remarriage

- No estate planning (62% of Americans)

- Missed tax opportunities costing thousands annually

The fix: A fiduciary advisor who implements systems and reviews regularly.

Missed Opportunities That Cost You Thousands

Almost every time I meet with someone for an initial review, I find they’re paying too much in taxes or missing opportunities. Here are the most common:

Not Maxing Out Tax-Advantaged Accounts

Self-Employed/Independent Contractors:

I recently reviewed tax returns for someone who’d been self-employed for years making good income. Never opened a SEP account.

A SEP (Simplified Employee Pension) allows independent contractors to contribute up to 25% of profit pre-tax.

Example:

- $200,000 income

- Could shelter $50,000 in SEP

- Tax savings: $15,000 (at 30% bracket)

We set up last year’s SEP AND this year’s SEP. Instant tens of thousands in tax savings.

Solo 401(k) is another option with even higher contribution limits ($69,000+ for 2024).

Only Contributing the Match

“I’m putting in 6%, and they match 3%.”

Me: “But you could contribute $30,500 per year, and you’re only putting in $10,000.”

Lost opportunity:

- Could contribute additional $20,000

- Tax deduction: $6,000-$7,000

- That tax savings could fund a Roth IRA—free money

Ignoring Health Savings Accounts (HSAs)

If you have a high-deductible health plan, HSAs are like “super IRAs”:

- Tax-deductible contributions

- Tax-deferred growth

- Tax-free withdrawals for medical expenses

- After 59½, works like a regular IRA (but with triple tax benefits)

Most people with high-deductible plans aren’t maxing these out. That’s free tax savings.

Missing Backdoor Roth Opportunities

High earners often think they can’t contribute to Roths. Wrong.

Backdoor Roth strategy:

- Contribute to non-deductible traditional IRA

- Immediately convert to Roth IRA

- Pay minimal tax on the conversion

- Decades of tax-free growth

Not Taking Advantage of Employer Benefits

Forgotten or unused:

- Employer stock purchase plans (often 15% discount)

- Flexible Spending Accounts

- Dependent Care FSAs

- Commuter benefits

- Education assistance programs

Insurance Blind Spots

Raising Deductibles Could Save Thousands

If you have an emergency fund, you can raise deductibles significantly:

Example savings per year:

- Home insurance: $300

- Auto insurance: $200

- Health insurance (if self-employed): $500+

Total annual savings: $1,000+

What to do with the savings: Invest it automatically.

$200/month invested at 8% for 20 years = $120,000+

That’s $120,000 you gave to insurance companies unnecessarily.

Missing Liability Coverage

You have assets. Do you have adequate liability protection?

I see people with:

- $100,000 in liability coverage

- $500,000 in assets

One lawsuit and they’re wiped out.

The fix: Umbrella policy ($1-2 million in coverage for $500-1,000/year)

Not Updating Beneficiaries After Life Changes

Horror stories I’ve seen:

Divorce scenario: Client got divorced, never updated beneficiaries. Died. Ex-wife received the entire 401(k) even though he’d remarried.

“All children equally” clause: One child passed away. The clause excluded that child’s spouse and kids because the language wasn’t specific.

Unmarried partner: Couple lived together 20 years. Not married. Partner died. Because they weren’t legally married, the surviving partner got nothing—state laws gave everything to distant relatives.

The Diversification-Asset Allocation Strategy

Diversification = Reducing Risk Across Asset Classes

Stocks, bonds, cash, real estate, different geographies

Historical sweet spots:

- 70% U.S. / 30% International stocks

- 60% stocks / 40% bonds (classic balanced portfolio)

Asset Allocation = Right Mix for Your Age/Timeline

Young (20s-40s):

- Aggressive (80-90% stocks)

- Long time horizon

- Can ride out volatility

- Want market dips (buying opportunity)

Mid-Career (40s-50s):

- Moderate (60-70% stocks)

- Balancing growth with stability

- Beginning to protect what you’ve built

At/Near Retirement (55+):

- Conservative (40-50% stocks)

- Protection becomes priority

- Need accessible cash/bonds

- Don’t want to sell stocks when market is down

Dollar-Cost Averaging

Accumulation phase: You WANT the market to go down when contributing monthly. You’re buying at a discount.

Retirement phase: You DON’T want the market down when withdrawing. You need buckets.

The Bucket Strategy for Retirement

This is how you stay happy whether markets are up or down:

Bucket 1: Cash/Money Market (1-2 years of expenses)

- Immediate access

- No market risk

- Low return, but high peace of mind

Bucket 2: Bonds/Fixed Income (3-7 years of expenses)

- Moderate stability

- Better returns than cash

- Low correlation to stocks

Bucket 3: Stocks (8+ years out)

- Growth for inflation protection

- Ride out volatility

- Doesn’t matter if it’s down short-term

Bucket 4: Annuities/Guaranteed Income (Lifetime)

- Can’t outlive it

- Predictable income

- Reduces longevity risk

How it works:

- Market up? Pull from stocks

- Market down? Pull from bonds/cash, let stocks recover

- Always have income from annuities/Social Security

Result: You can spend without panic. You’re happy whether markets rise or fall.

Social Security Strategy Blind Spots

When should you take Social Security? It depends.

Questions rarely asked:

- Do you hate your job? (Maybe work 2-3 more years, max out 401k, delay SS)

- Should you take SS at full retirement age and invest it? (Sometimes yes)

- What’s your break-even age?

- How does your decision affect your spouse’s survivor benefits?

No one-size-fits-all answer. But most people make this decision without professional analysis.

Estate Planning Disasters

62% of Americans don’t have:

- Will

- Trust

- Financial Power of Attorney

- Healthcare Power of Attorney

- Living Will

What happens without these:

- State decides who gets your assets

- Court appoints guardian for your kids

- Medical decisions made by strangers or distant relatives

- Probate costs eat up 5-10% of estate

- Family fights destroy relationships

Recent real example:

Client had adult son in accident at age 40. Single. No healthcare power of attorney.

Result: Family had to go to court just to make medical decisions for their own son.

When it’s NOT complicated (inexpensive estate planning):

- Married once, stayed married

- Have kids together

- Don’t own a business

- No partners

When it IS complicated (need attorney):

- Second marriages with kids from both sides

- Business partners

- Significant real estate holdings

- Blended families

Tax Strategy Blind Spots

Your biggest expense as income grows? Taxes.

Yet people shop endlessly for groceries but let the IRS take whatever it wants.

Taxable vs. Tax-Advantaged Buckets

Taxable (Accessible):

- Savings accounts

- Brokerage accounts

- Emergency funds

Tax-Deferred (Locked until 59½):

- Traditional 401(k)/IRA

- SEP/Solo 401(k)

- Annuities

Tax-Free:

- Roth IRA/401(k)

- HSAs

- Life insurance cash value

Strategy: Have money in ALL three buckets for maximum flexibility in retirement.

Roth Conversion Strategy

When you retire but before RMDs (age 73):

- Income might drop

- Lower tax bracket temporarily

- Perfect time to convert traditional IRA to Roth

- Pay taxes now at lower rate

- Future growth is tax-free

This requires planning. Most people miss this window.

The Big Tax Refund Trap

“I got a $6,000 tax refund!”

Me: “How much interest did you earn on that money?”

Them: “Huh?”

You gave the IRS an interest-free loan. You could have:

- Raised exemptions

- Received money in paycheck monthly

- Invested it throughout the year

- Earned returns

Better strategy: Adjust withholding, invest the difference automatically.

How We Work With Clients: The Review-to-Implementation System

Step 1: Education & Advice

“When we’re done, you’ll be able to explain your plan to your best friend at lunch.”

We don’t just tell you what to do—we educate you on WHY.

Step 2: Initial Review

We assess from birth to today:

- What do you have?

- What do you know?

- What do you make?

- What are your goals?

We review:

- All accounts

- Insurance coverage

- Tax returns

- Beneficiaries

- Estate documents

Step 3: Defense (Protecting Income & Assets)

Insurance marketplace review:

- Life (term and permanent)

- Disability

- Health

- Property & Casualty

- Umbrella liability

- Long-term care

We shop multiple carriers. Not tied to one company.

Step 4: Offense (Growing Wealth)

Investment strategy:

- Retirement plans

- College savings (529s)

- Asset allocation

- Diversification

- Professional money management

Access to 9,000+ investment choices through major clearing firms.

Step 5: Product Marketplace

Think Amazon for financial products. We’re fiduciaries—we find the best fit for YOU, not what pays us the most commission.

Step 6: Implementation

This is where we’re different.

We don’t just give advice. We implement:

- Set up accounts

- Establish automatic drafts

- Change allocations

- Update beneficiaries

- Order estate documents

You leave with systems running, not homework to do.

Step 7: Reviews & Updates

Money in motion happens when life changes:

- Marriage/divorce

- Having kids

- Job changes

- Someone passes away

- Kids graduate college

- You get older

We review regularly and adjust as life evolves.

For Business Owners: Special Opportunities

If you own a small business, you have massive opportunities others don’t:

Retirement plans with tax credits:

- Setting up a 401(k) now gets you tax credits

- Even with 5-10 employees, it’s possible and affordable

- Makes you competitive in hiring

SEP vs. Solo 401(k) vs. Simple IRA:

- Each has different contribution limits

- Different administrative requirements

- We help you choose based on your situation

Buy-sell agreements:

- What happens if partner dies?

- How do you fund the buyout?

- Life insurance strategies

Key person insurance:

- Protect business if critical employee dies or becomes disabled

The Referral Partner Program

If you’re a connected individual who likes learning about money, we have a program where you can:

- Partner with us

- Introduce financial services to your network

- Potentially make a career change

- Learn from the inside of a 40-year-old firm

Visit RoyMatlockJr.com and look for “Join Our Team.”

Why You Need a Second Opinion NOW

Even if you have an advisor, get a second opinion. Here’s why:

75-80% of Our Business Comes From Other Advisors’ Clients

Why? Because many advisors are B, C, or D players. Even D players can stay in business, but they’re not serving you well.

Signs you might have a mediocre advisor:

- Annual review is just performance numbers (no tax planning, no estate review)

- They never bring up opportunities (Roth conversions, tax strategies)

- You haven’t updated beneficiaries in years

- They don’t return calls promptly

- You don’t understand your own investments

Even A-Players Can Miss Things

No one is perfect. A fresh set of eyes often catches opportunities or risks the first advisor missed.

No downside to a second opinion. Only upside.

Taking Action Today

Visit RoyMatlockJr.com or call 615-843-2999 to:

- Schedule a free phone consultation (low-pressure, high-value)

- Access 200+ podcast episodes (searchable by topic)

- Download free resources (budget forms, retirement calculators)

- Register for monthly webinars (second Saturday of every month)

- Explore the referral partner program (if you’re interested in the business)

The Bottom Line

You get second opinions on major surgery. You get second opinions on legal issues. You get second opinions on home repairs.

Why wouldn’t you get a second opinion on the thing that determines your entire quality of life?

One financial mistake costs $50,000-$500,000 over your lifetime. How many mistakes are hiding in your current plan?

Procrastination is the #1 killer of financial success. Don’t wait another day, another month, another year.

The blind spots are there. The question is: Will you uncover them before they cost you a fortune?

Listen to the Full Podcast

Want to hear more real-life examples of financial blind spots and how they were fixed? Listen to the complete episode where I share stories from 40 years and 40,000+ client reviews.

Listen to the full podcast episode: “Why You Need a Second Opinion on Your Money”

In this episode, I walk through the exact review process we use, share the most common mistakes by age group, and explain how our bucket strategy keeps retirees happy in any market condition. Plus, I’ll tell you the choking incident story and how it relates to financial emergencies.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.