Risk Buckets & Tax Buckets: Stay Calm at Market Highs

When stock markets are hitting all-time highs week after week, it is natural to wonder if you should be doing something different with your money. Should you sell and lock in gains? Should you hold off on new investments until things calm down? Should you move everything to cash and wait for a correction?

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy walks through the complete framework he uses to keep clients calm and on track regardless of what the market is doing. This is not about predicting what happens next. This is about having a system in place so that market highs, market lows, and everything in between become opportunities instead of threats.

Three Stages of Life — And What Matters Most at Each One

Roy breaks financial life into three stages, and each one requires a different mindset.

The early getting started stage is all about overcoming procrastination. The biggest mistake people make is never getting started at all. Even if you do nothing more than set up a $100 per month automatic investment into a mutual fund, you have crossed the line from intention to action. Roy works with clients who want their kids and grandkids on this track early — $50 or $100 or $200 per month automated before they are teenagers, so by the time they are in high school they can see how compound interest actually works in their own account.

The accumulation stage is where you start seeing real momentum. This is when people change jobs and have 401k rollovers to deal with, when income is moving up and cash starts sitting in bank accounts earning nothing. The key here is growing your income every year and bumping up that automatic draft to match. Fully fund your retirement plans, capture the employer match, and let consistency do the heavy lifting.

The retirement income stage is a completely different game. Now the focus shifts from growth to making sure your income lasts and does not run out. The way you handle withdrawals, the order you pull from different accounts, and the balance between growth and safety all become critical. This is where risk buckets and tax buckets earn their keep.

Investment Risk Buckets

Risk Buckets — Defense, Mid-Range, and Offense

Roy organizes investments into three risk buckets, and the goal is to have money in all three so that you are never forced to sell at the wrong time.

The defense bucket is cash, money markets, annuities, and CDs. Roy is not a fan of tying up money in CDs when you can get similar returns in a money market account with full liquidity, but the principle is the same — this is the money that does not go down when the market drops. When you are retired, this bucket provides fixed income you can count on every month along with Social Security. When the market is down, you pull from here and leave your growth investments alone.

The mid-range bucket is bonds, balanced funds, and maybe rental properties — anything designed for steady yield without the full volatility of stocks. This bucket smooths the ride and gives you something to pull from when stocks are struggling but you do not want to touch cash reserves.

The offense or growth bucket is stock funds and ETFs that drive long-term growth. Historically the stock market has averaged about 10% annually over the past 100 years, but that comes with a pattern: up three years, down one year. If you happen to invest a lump sum right before a down year, you could see your $100,000 drop to $80,000 or lower. That is why the other two buckets exist — so you never have to panic sell when growth investments are temporarily underwater.

The whole point of risk buckets is to keep you from buying high and selling low. When you have a plan that spreads money across all three buckets, market declines do not wreck you because you have other places to pull from. And when markets are up, you are pulling profits from the growth bucket and letting the rest ride.

Tax Buckets — Taxable, Tax-Deferred, and Tax-Free

The other dimension Roy uses to structure money is tax treatment. Most people do not realize that their biggest expense is not their mortgage or car payment — it is the difference between gross pay and take-home pay. That gap is taxes, and if you are a six-figure household or higher, you are likely paying more in taxes than anything else.

The government gives you tax laws designed to reduce your tax bill if you use them. But they do not call you up to remind you when you miss out. That is where tax buckets come in.

The taxable bucket is bank accounts and brokerage accounts that generate 1099 income — dividends, interest, capital gains. Taxable means accessible, so you need some money here for emergencies and opportunities. But Roy’s rule is simple: never pay taxes on money you are not currently using. If you have more sitting in taxable accounts than you need for an emergency fund and a little opportunity money, you are going to work every week just to pay the IRS on money you are not touching. That makes no sense.

The tax-deferred bucket is retirement plans like 401k, 403b, traditional IRAs, and annuities. These accounts grow without being taxed every year, and in many cases you get a tax deduction when you put the money in. Roy uses the buy-one-get-one-free analogy: if you put $20,000 into a 401k and you are in the 25% tax bracket, you get a $5,000 tax refund. You can take that $5,000 and put it into a Roth IRA. You just bought one and got one free — a $20,000 pre-tax account plus a $5,000 tax-free account, and if your employer matches contributions you are adding even more free money on top.

The tax-free bucket is Roth IRAs, Roth 401ks, and loans. You can borrow against your house with a home equity line of credit, borrow against life insurance, or borrow against your brokerage account, and none of that creates taxable income. Real estate investors use this constantly — as rents and equity go up, they refinance and pull tax-free cash out while the rental income covers the new payment. That is how people with high net worths avoid paying taxes. They are not cheating. They are using the tax code the way it was designed.

Putting Risk Buckets and Tax Buckets Together

When you combine risk buckets with tax buckets, you get a complete financial safety system. If the market is down and you need income, you pull from your conservative buckets — maybe a money market account in your taxable bucket or guaranteed income from an annuity in your tax-deferred bucket. If the market is up, you pull from growth accounts that have appreciated and maybe rebalance by moving some profits into more conservative positions.

Every year Roy and his team meet with clients to decide where withdrawals are coming from. This year it might be required minimum distributions from a traditional IRA. Next year it might be from a taxable brokerage account where part of the withdrawal is return of principal and does not count as income. The goal is to control the tax impact while keeping the portfolio balanced and letting growth continue where it makes sense.

This is what creates the calming effect Roy talks about. When you have a plan, market drops do not scare you because you have buckets that are not affected. Market highs do not stress you out because you know you can take profits and rebalance without creating a huge tax bill. You stop checking your account every day wondering what happened, and you start thinking in terms of years and decades instead of daily noise.

Time in the Market Beats Timing the Market

Roy is blunt about this: no one knows how to time the market consistently. The people who try to jump in and out, waiting for the perfect moment, almost always underperform the people who just stay invested and ignore the noise.

Research shows that if you miss just the 10 best days in the market over a 20-year period, your return gets cut roughly in half. The problem is that those best days often happen right after the worst days, so if you are out of the market trying to avoid losses, you also miss the recoveries. The math does not work in your favor.

Time in the market is what matters. You invest consistently, you leave the money in, and you ignore the daily headlines. Corrections are normal. Crashes are opportunities if you have a plan. And the market always recovers — it has never failed to do so over any 20-year period in history.

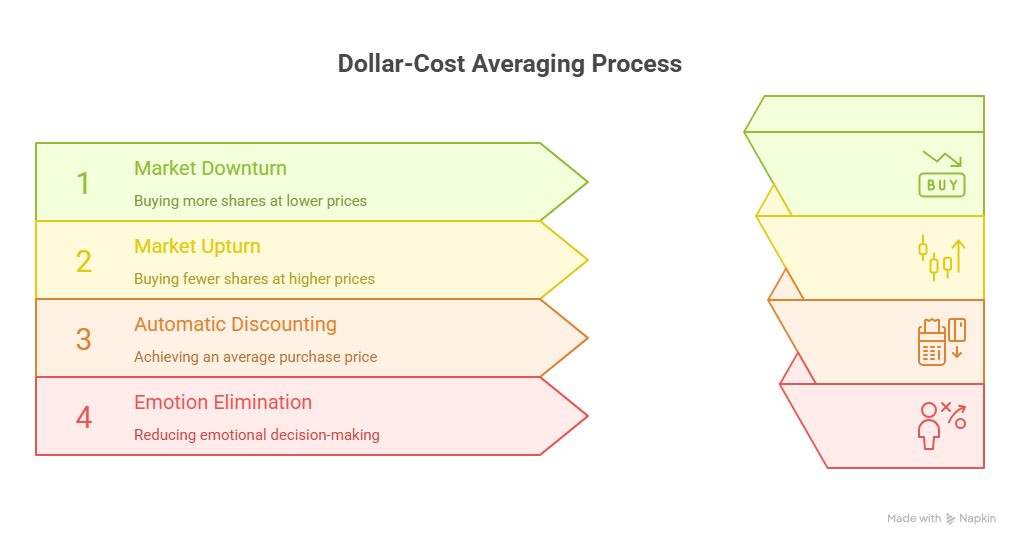

Dollar-Cost Averaging Eliminates Emotion

One of the simplest and most powerful tools in Roy’s system is dollar-cost averaging — investing the same amount of money every month regardless of what the market is doing.

When the market is down, your fixed monthly contribution buys more shares. When the market is up, it buys fewer shares. Over time, this means you automatically buy more at lower prices and less at higher prices. You get an automatic discounting system without having to think about it or time anything.

This is exactly what happens when you contribute to a 401k every paycheck. The money goes in whether the market is at an all-time high or in the middle of a crash, and over the long run that consistency wins. It removes emotion, reduces regret, and creates the foundation of long-term wealth.

Dollar-Cost Averaging Process

What to Do With Lump Sums at Market Highs

Roy gets this question constantly: I have $100,000 in cash and the market is at an all-time high — should I invest it all at once or wait?

Statistically, lump sum investing wins about 75% of the time. If you put the money in all at once, three out of four times you will do better than if you had dollar-cost averaged it in over 12 to 24 months. But that does not help you if you happen to be in the 25% of cases where the market drops right after you invest.

Roy’s approach: blend the two strategies. Put some of the lump sum into a bond fund or money market where it earns more than a bank account, and then dollar-cost average into the stock market over 12 to 24 months. If the market keeps going up, you are still participating because you are buying in every month. If the market drops, you are not sitting there watching $100,000 turn into $75,000 — you are buying more shares at lower prices with the cash you held back.

The key is protecting against the downside while still staying in the game. You do not have to get it perfect. You just need a plan that you can stick with regardless of what happens next.

Asset Allocation Determines 90% of Your Long-Term Return

The mix of stocks, bonds, and cash in your portfolio — what Roy calls asset allocation — determines about 90% of your long-term return. Individual stock picks and market timing account for the other 10% at most, and most people are terrible at both of those.

Asset allocation starts with age. If you are young, you can afford to be more aggressive because you have decades to ride out market cycles. If you are near retirement, you need to be more conservative because you do not have time to recover from a major loss right before you start pulling income.

But age is just the starting point. Roy also looks at risk tolerance. If someone comes in with all their money sitting in the bank, that tells him they are conservative by nature, and he is going to ease them into a more growth-oriented portfolio slowly. If someone has been riding the S&P 500 for years without blinking, they have a higher risk tolerance, but Roy might still dial them back a bit if they are close to retirement.

Time horizon matters too. If you need the money in five years, you cannot afford to take the same risk as someone who does not need it for 20 years. And income needs play a role — if you are pulling 5% per year to live on, the portfolio has to be structured to support that without forcing you to sell stocks in a down market.

Studies show that a 60% stock, 40% bond portfolio has historically delivered the best risk-adjusted returns over time. It is not the highest return — 100% stocks would beat it in a long bull market — but it is the allocation most people can actually stick with when things get rough. And sticking with the plan is what matters most. Visit our Calculators section to model different allocation scenarios and see how they would perform over time.

Rebalancing Keeps You Disciplined

Markets do not move in straight lines, and over time your asset allocation will drift. If stocks go up and bonds stay flat, you might end up with 70% stocks and 30% bonds even though your target was 60-40. That means you are taking more risk than you planned.

Rebalancing means selling some of what has gone up and buying more of what has stayed flat or gone down. It forces you to sell high and buy low, which is exactly what you are supposed to do but almost no one actually does without a system.

Roy and his team review portfolios regularly and rebalance when allocations drift too far from the target. If you are retired and required minimum distributions are coming out this year, they decide which bucket to pull from. If the market is up, they take profits from growth accounts. If it is down, they pull from conservative buckets and let the growth investments recover.

This is the opposite of what most people do on their own. Most people sell when they are scared and buy when they feel confident, which means they sell low and buy high. A rebalancing system flips that script and keeps you disciplined.

The Big Lesson — Stay Invested, Diversify, and Stick to the Plan

Market highs feel like peaks, but they often turn into new lows later. The all-time high from 2000 looked insane at the time, and then the market dropped 50%. But if you stayed invested, the market eventually recovered and went on to hit new highs. The same thing happened in 2008. And 2020. And every other correction and crash in history.

The people who won were the ones who stayed invested, kept their asset allocation in check, and used corrections as opportunities to buy at a discount. The people who lost were the ones who panicked, sold everything, and then sat on the sidelines too scared to get back in.

If you have a system in place with risk buckets, tax buckets, dollar-cost averaging, and regular rebalancing, you do not have to predict what the market does next. You just follow the plan, and the plan works regardless of whether markets go up, down, or sideways. Download the free resources and tools at roymatlockjr.com/resources to start building your own system today.

Ready to Build Your System?

Roy and his team are fiduciaries who work with clients to build personalized financial plans using this exact framework. If you want help putting risk buckets and tax buckets in place, reach out for a 15-minute phone call to see if it is a good fit. Visit roymatlockjr.com or call 615-843-2999.

Listen to the Full Podcast

This episode covers the complete risk bucket and tax bucket framework in detail, with real examples and client stories. Listen to the full November 22, 2025 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: November 22, 2025

You can also watch the full episode on YouTube: Watch on YouTube

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.