A Simple Plan for Financial Independence

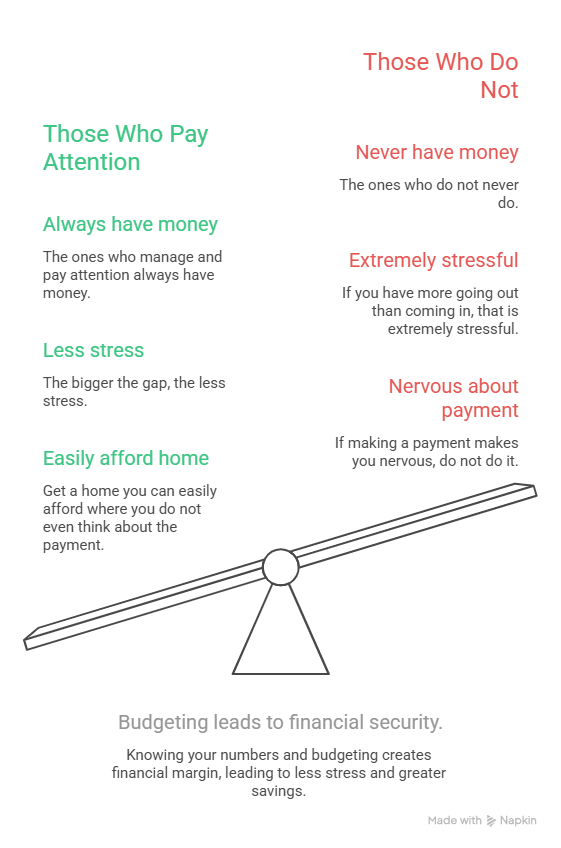

After 40 years of advising people on money, Roy Matlock Jr. has learned one undeniable truth: the people who manage and pay attention to their money always have money. The ones who do not pay attention never do. It is that simple.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy breaks down a simple plan for financial independence that anyone can follow. This is not about complicated strategies or getting lucky with Bitcoin. This is about basic understandings of money, systematic planning, and automation that builds wealth over time whether you think about it or not.

The 10% Rule — Save a Dime for Every Dollar You Earn

Roy remembers reading books like The Millionaire Next Door early in his career. One concept stuck with him: the 10% rule. You save 10% of what you make. Period.

When you save 10% of your income, you are telling yourself that you are going to be profitable on your work. If you spend every dollar you make year after year with nothing left to show for it, you are working for free. Sure, you are eating and maybe you have a roof over your head, but you are working for everyone else — not for yourself.

The mindset is simple. If you get a dollar, you keep a dime. If you get $10, you keep a dollar. If you get $100, you keep $10. That is the baseline. As you get better at managing money and your income grows, you can crank that percentage higher. All that does is speed up the time it takes to reach financial independence.

Budgeting leads to financial security.

Start With a Budget — Know Your Numbers

The number one thing Roy has found in 40 years of working with people is this: the ones who manage and pay attention always have money. The ones who do not never do.

Roy shares a story about a recent call with a client who has $700,000 saved and a paid-off house. They are getting ready to retire, and the husband gave Roy a point-by-point breakdown of exactly what it costs them to live. They know their numbers. That is why they have $700,000 saved.

If you go to roymatlockjr.com and download the budget form under Resources, it will walk you through everything. You list all your expenses — recurring bills, irregular expenses like car maintenance and vacations, everything. Then you compare that to your income and make sure there is a gap.

That gap between your income and your outgo is what Roy calls the quality of life gap. The bigger the gap, the less stress. If there is no gap, that is stressful. If you have more going out than coming in, that is extremely stressful. The goal is to create margin so you can breathe and save.

When you buy a house, go conservative. Lenders will tell you that you can spend 33% of your income on your mortgage and debts. If you do that, you will be broke all the time. Get a home you can easily afford where you do not even think about the payment. If making a payment makes you nervous, do not do it. Get something cheaper. That way, you will have money left over to save.

Automate Everything — Set It and Forget It

Once you have your budget set up and you know you can save at least 10%, the next step is automation. You automate your bills. You automate your savings. You do not rely on willpower or motivation. You set it up once, and it happens every month whether you think about it or not.

Roy remembers his early days calling clients and asking how the year was going. If they said they were making more money than last year, he would say, “Let’s bump your draft.” They would agree, and he would increase their monthly investment by $100. Eventually, clients knew what was coming. When Roy called, they would just say, “Yep, go ahead and bump it.”

That is how simple it should be. One phone call. One adjustment. Done.

Roy started with $50 per month into a mutual fund and $100 per month into an emergency fund. He bumped it as his income grew. That is all it takes.

Here is how you set it up. All your bills get automated out of what Roy calls a draft account. All your savings get automated. Then you manage your weekly spending. You are not managing everything. You are just managing what you spend week to week, and the rest takes care of itself.

The Quality of Life Gap — Live Below Your Means

Roy talks about firing your expenses and only rehiring the ones you really need. Go through every line item in your budget. If you did not have this expense, would you rehire it? If the answer is no, cut it.

Cost-cutting is not about being cheap. It is about creating margin. The bigger the gap between your income and your outgo, the less stress you carry. That gap is your quality of life gap, and it is what allows you to save, invest, and build wealth.

Roy tells the story of buying suits at a consignment shop in his early days. There was a doctor who wore the exact same size, and every year, the doctor would hand off expensive, tailored suits. They were dry-cleaned, pressed, and perfect. Roy got designer suits for a fraction of the cost. Eventually, Roy met the doctor — his name was embroidered inside the jacket. Years later, Roy passed those same suits to one of his reps who wore the same size.

That is the mindset. Never pay retail for anything, and you will start seeing money free up. Then you call your advisor and say, “Bump my draft. I want to save more.”

Pay Yourself First — The Foundation of Wealth

Paying yourself first means your savings come out before you pay anyone else. Before the mortgage. Before the car payment. Before anything. You pay yourself.

If you have a 401k at work and your company matches 3%, you put in 3% and they give you 3%. That is a 100% return before the money even starts growing. Then you get a tax deduction. If you are in the 25% tax bracket, that deduction saves you about another dollar for every three you put in. So you put in $3, it only costs you $2 after the tax savings, but your account has $6 in it — $3 from you, $3 from the match. That is a pretty good deal.

At minimum, you should always capture the full employer match. That is free money. There is no reason not to take it. That is 3% of your 10% right there.

You can also invest in a Roth IRA or a traditional IRA. The decision depends on your age and income. If you are young, Roy recommends Roth. You pay taxes now at a low rate, and the money grows tax-free forever. If you start young and retire with a big Roth IRA, you might never pay income taxes in retirement.

If you are older and in a higher tax bracket, a traditional IRA might make more sense. You take the deduction now and pay taxes later when your income is lower.

For high earners who make too much to contribute directly to a Roth IRA, Roy teaches the backdoor Roth strategy. You contribute to a traditional non-deductible IRA — $8,600 if you are over 50 in 2026 — and immediately convert it to a Roth. Now you just funded a tax-free account even though your income was too high to contribute directly.

Roy has young clients in their 30s who are high earners maxing out their 401ks and funding backdoor Roth IRAs every year. They are building serious wealth because they started early and automated the process.

Eliminate Bad Debt — Only Keep Good Debt

Bad debt has three characteristics. First, you cannot afford the payment. It stresses you out. Second, it is tied to something that goes down in value. Third, it carries a high interest rate. Car loans, credit cards, financing depreciating assets — all bad debt.

Good debt has opposite characteristics. You can easily afford the payment. It is tied to something that appreciates. The interest rate is reasonable. A mortgage on a home you can afford is good debt. Borrowing for equipment that grows your business is good debt. Financing rental property that cash flows is good debt.

Roy shares a client story. The client called and said he was buying another motorcycle. He could pay cash, but the dealer offered 3.9% financing. Should he take the financing or pay cash? Roy said take the financing and invest the cash instead. Anytime you pay off a debt, the interest rate is the rate of return you are getting. At 3.9%, the client can do better by investing that cash. Keep the low-rate debt and invest the difference.

Roy also tells his own story. In his early twenties, he bought two new cars. He was strapped. He finally got out from being upside down, sold both cars, and bought two junkers. He still had to finance them, but he paid them off in one year instead of four. That was the last car payment he ever had.

Years later, Roy turned 40 and bought a new Porsche 911 for about $80,000. Twenty thousand miles later, it was worth $50,000. He said he would never do that again. The next Porsche he bought had 5,000 miles on it and cost $30,000 to $40,000 less than buying new. You are driving a used car anyway the second you drive it off the lot. Why pay new-car prices?

Build an Emergency Fund — Your Financial Shock Absorber

An emergency fund is three to six months of expenses sitting in cash. If you are married and both working, three months is probably fine. If only one of you works, you want six months.

The emergency fund is not about earning a big return. It is about keeping you from borrowing money, cashing out retirement accounts, or going into debt when life happens. It keeps you from paying penalties and interest. That is your return.

Your first goal is $1,000. Then you work up to three months of income. Once you are completely out of bad debt, you can really start cranking up your savings.

Protect Your Income — Life Insurance and Disability Insurance

Roy read an article recently that said because of inflation, about 100 million people are either underinsured or without life insurance. If you have a family and kids, you need life insurance. Period.

The best way to start is with term life insurance. It is designed to be cheap and protect your family if you die unexpectedly. Roy had a client getting a term policy — $500,000 of coverage for about $30 per month. When you are young, coverage is incredibly affordable.

Roy’s firm has a 10-minute term life insurance product that can issue up to $2 million of coverage if you are in good health. It even includes a will and trust. There is no reason to leave your family in shambles if something happens to you. Visit roymatlockjr.com to get it set up.

Rule of thumb: buy 10 times your income in term life insurance as a minimum. If you and your spouse each make $75,000 per year, you each need about $750,000 of coverage. That money would replace your income over time and allow your family to stay in the house and maintain their lifestyle.

Many term policies now come with living benefits. If you are diagnosed with a chronic, critical, or terminal illness, you can access most of the death benefit while you are still alive. This is not just death insurance anymore — it is life insurance.

Disability insurance is also critical. If you cannot work because of an injury or illness, disability insurance replaces about 60% of your income. You protect your income so your family does not lose everything if you cannot earn.

Professional Money Management Process

Where to Put Your Money — Professional Money Management

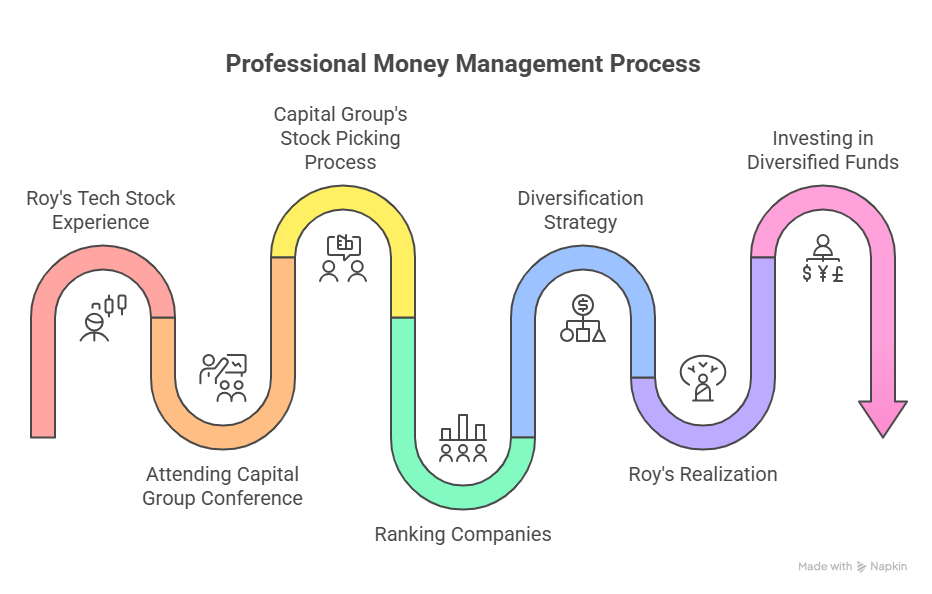

Roy does not believe that individual investors will outperform professional money managers over the long run. He learned this lesson the hard way.

Back in the 1990s, right before the tech crash, Roy was buying tech stocks on his own. He put in $40,000, and it grew to $300,000. He thought he was a genius. Then the tech crash happened. By the time he got out, he doubled his money — he ended up with about $80,000 — but he had been sitting at $300,000.

During that same period, Roy attended a conference in California with Capital Group, the largest active fund manager in the world. They walked him through how they pick stocks. They visit companies on-site and meet with C-level executives. They talk to employees. They meet with research and development to find out what products are in the pipeline. For pharmaceutical companies, they go to doctor conventions to find out what doctors are prescribing. They even talk to patients. They send analysts to Washington, D.C., to track regulatory changes.

Then they rank companies A, B, C, D, or E based on what the stock is trading for versus what they think it is worth. Even then, they will not put more than 5% of the fund into any single company.

Roy sat there and thought, “I am not going to beat that.” And he was right. Professional money managers do 21,000 company visits worldwide every year. They have research, resources, and information that individual investors do not have. They spend every day looking for opportunities and avoiding risks.

Your best path to financial independence is to put your money into highly diversified, professionally managed funds with low costs. Let the professionals do what they are best at, and you focus on what you are best at — earning income and living your life.

The Power of Compounding — How $500 Per Month Becomes $1 Million

If you put in $300 per month for 10 years, you will have about $58,000. That does not seem like a big deal. But keep going. Twenty years gets you $200,000. Thirty years gets you $500,000.

Here is where it gets interesting. That $500,000 is going to double in seven to nine years at 9% to 10% returns. You just made $500,000 without putting in another dime. Then that $1 million doubles again in six to eight years. Now you made another million. The compounding accelerates every time you hit a new doubling period.

What do you need to do? Get to $100,000 as fast as possible. Once you have $100,000, the doubling periods start working in your favor. The first doubling is $100,000. The second is $200,000. The third is $400,000. The wealth starts building on itself.

How do you get $100,000 in 10 years? About $500 per month. That is $100 per week. Think about that. One hundred dollars per week gets you to $100,000 in 10 years. While your friends are blowing their money, you call your advisor and say, “Set up a $500-per-month automatic draft and make sure it goes into investments every month.” Ten years later, you have a foundation. Twenty years later, you have serious wealth.

Find Work You Love — The First Step to Financial Independence

Roy believes the first step to financial independence is finding something you like doing. If you wake up every day and love what you do, you will naturally get better at it. You will earn more. You will be valuable to your employer or your clients. That is job security.

Roy found financial advising when he was 25. He just turned 65, and people ask him when he is going to retire. His answer: never. Why would he retire? This is fun. He gets to help people get financially independent. When clients call him excited and appreciative of what he has done for them, it makes him feel good. That is worth more than any paycheck.

Your job is to get better and more valuable. If your company would be concerned about losing you, you have job security. From there, you save your money, and one day you might go into business for yourself. Being an entrepreneur is a risk, but as Roy’s friend Chuck McDowell says, “Entrepreneurs are risk takers, and taking a risk is fun.”

The bottom line: work at getting your income solid doing something you like. You will always grow your income if you are in a growing market and you love what you do. Then you manage what you earn. You take part of it and put it into things that do not require your effort. That is do-nothing money. That is the money that makes money while you sleep.

The Complete Simple Plan — Step by Step

Here is Roy’s complete simple plan for financial independence from start to finish.

Step one: Set up a budget with the intention of saving 10% of your income. Download the budget form at roymatlockjr.com under Resources.

Step two: Determine if you have an income problem or an outgo problem. If your income is the issue, work on increasing it — get more education, find a better job, start a side business. If your outgo is the issue, cut expenses and create margin. The good news is it takes a lot less time to fix the problem than it took to create it.

Step three: Build an emergency fund. First goal is $1,000. Then work up to three months of expenses. Once you are out of bad debt, push it to six months.

Step four: Eliminate bad debt. Bad debt is tied to something that goes down in value, has a high interest rate, and you cannot afford it. Good debt is tied to something that appreciates, has a reasonable interest rate, and you can easily afford it.

Step five: Protect your income. Buy term life insurance — 10 times your income is the minimum. Buy disability insurance to replace 60% of your income if you cannot work. Buy proper health insurance. Roy likes high-deductible plans with health savings accounts. You get tax deductions and tax-free growth.

Step six: Protect your assets. Buy home and auto insurance. Raise your deductibles as your emergency fund grows to save on premiums. Buy an umbrella policy for extra liability coverage. If you are at or near retirement, make sure you have a plan for long-term care.

Step seven: Set up a will and trust. This includes healthcare and financial powers of attorney and a living will. A living trust lets you avoid probate. There is no reason to give the probate court or attorneys your money when you can give it to whoever you want.

Step eight: Automate your investing. If you wait to save money when you have money, you will never have money. Set up automatic drafts from your checking account or automatic contributions through your payroll. You can start with as little as $50 per month.

Step nine: Use Roth IRAs to grow tax-free income. Max out your 401k to get matching funds and tax deductions. Use 529 plans or custodial accounts for college savings.

Step ten: Diversify with professionally managed funds. Put your money into funds that are highly diversified with low costs. Let the professionals manage it while you focus on earning income and living your life.

That is the complete simple plan. You check off the boxes. You move along. You build your financial independence step by step.

Ready to Build Your Simple Plan?

Roy and his team are implementers. They do not just give advice — they execute plans and make sure everything is set up correctly. If you want help building your simple plan for financial independence, reach out for a free consultation.

Visit roymatlockjr.com or call 615-843-2999. You can download free guides, access the budget form, and use the financial calculators. You can also open investment accounts for as little as $50 per month or $250 to start.

Everything you need to get started is at roymatlockjr.com/resources.

Listen to the Full Podcast

This episode walks through the complete simple plan for financial independence from start to finish. Listen to the full March 14, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: March 14, 2026

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.