The Offense: Build Wealth, Cut Taxes & Change Your Family Tree

Defense keeps you from losing. Offense helps you win. You need both. But if you only play defense, you never build wealth. Once you have the defense in place — the protection, the emergency fund, the proper insurance coverage — it is time to go on the offense.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy dedicates the entire show to the offense. This is about building wealth. This is about cutting taxes. This is about passing money along to the next generation and changing your family tree. Roy breaks down the exact system he has used for 41 years to help thousands of families build serious wealth through compound interest, diversification, professional money management, and strategic tax planning.

The message is simple but powerful: your income is the key to the outcome of anything you do with your money. But your income alone is not enough. You have to understand how to make your money work for you. And that is the offense.

Stagnant Wealth Growth

Step One — Grow Your Income and Become More Valuable

Roy learned this 41 years ago and has never forgotten it: you have to manage your income. Your income is the key to everything. The first step of the offense is always to grow your income.

How do you grow your income? You become more valuable in the workplace. If you are an employee, get more education. Get a different degree. Roy’s daughter went and got her master’s degree, and it allowed her to earn more money in her industry. If you are a business owner, get better at your skill set. Understand how to market yourself and put yourself out there in the right way.

Roy does radio as a business owner. Why? Because as a business owner, he gets his name out there more. People know who they are dealing with before they come to meet with him or any of his advisors. The whole idea is you have to always be learning. Constant learning. That is how you grow your income.

All things being equal, if you make more money, you have a better chance of being able to save more money. Roy calls this the 50-40-10 rule. You beat 50% of anybody you compete with in anything by a willingness to outwork them. You beat another 40% by just being an honest, above-board person that creates a reputation. And then lastly, you are in the top 10%. If you are in the top 10%, you are competing with people who are hard workers and good, honest people. But the good news is you are in the top 10%, and anything you do, if you get in the top 10%, you are doing well.

The Foundation — Live on 50%, Save 25%, Taxes Take 25%

Roy has always encouraged people to get good at something, become great at it, become an independent contractor doing it, then eventually expand it into a business. That is the starting point.

Then as you go along, be willing to live on 50% of what you earn. If you are making $100,000, you live on $50,000. You save $25,000, and the other $25,000 probably gets eaten up in taxes and Social Security.

Now, if you do that and then you say you want to raise your lifestyle, great. Raise your income. Keep that 25% savings mindset, and you are off to the races. The key is not to increase your lifestyle spending when you get a raise. Increase your savings. That is how you build wealth.

If your finances are not where you want them to be, ask yourself one question: am I making a profit on my income? A profit means you are spending less than you make. That is the foundation. Set your budget up. Have an emergency fund. All that stuff is defense. Then from there, you start automating outcomes.

Automation — The Key to Consistency

How do you automate outcomes? The first step is to automate your savings every month. If you are listening right now and you want to change your life, call Roy at 615-843-2999 and set up a phone call. Tell the advisor, “I want to change my life with my money.”

The advisor will say, “We need to set you up on an automatic draft coming out of your bank account.” Once a month, money will automatically be invested. Over time, it becomes a habit. You wake up one day and say, “Man, this is cool. I put $500 a month away. A year later, I have put $6,000 away, and I did not have to do anything other than just let it happen.”

That $6,000 starts growing. Ten years later, you have put $60,000 in, and if things go normal, you have $120,000. All you had to do was start. You just had to start it.

Roy set up his first draft on his checking account in 1985 and has had drafts coming out of his account since then. That is the key. It is not waiting until there is money to save. It is automating the savings so you do not have to think about it.

Think about how subscription companies work. They get you started on an automatic payment, and you forget about it. Then they keep charging you every month. If that is the case, why would you think that if you got started paying yourself into an investment every month that was automated, you would stop it? You would not. That is the power of automation.

Compound Interest — The Magic of the Rule of 72

The second part of the offense is understanding the magic of compound interest. Roy calls it magic because it truly is magical once you understand how it works.

The rule of 72 says: divide any interest rate into 72, and it tells you how long it takes your money to double. If you get 4%, your money doubles in 18 years. If you get 12%, your money doubles in 6 years. The better your rate of return, the quicker your money doubles.

Here is a comparison. If you put your money in at 1%, the rule of 72 says in 72 years, your $1,000 will grow to $2,000. But if you put it in at 10%, it doubles in 7 years. Would you rather have 70 years or 7 years? Then it doubles again. And doubles again. And doubles again.

Your money will work as hard as you ask it to work. If you want lazy money, just take it to the bank and put it in an account, and they will pay you maybe 1%. Your money will double in 72 years. If you want it to work harder, you might put it in a money market account at 3%, and your money will double in 24 years. If you put it in a bond fund at 5% or 6%, it will double in 14 or 15 years. If you put it in the stock market, historically it has averaged about 10%, and your money doubles every 7 years.

Do you want lazy money or do you want your money to work hard for you? That is the choice. And that is why compound interest is so powerful.

Time and Consistency — Not Timing

The third part of the offense is time and consistency. The most important thing you can do is give yourself time. How do you do that? You begin sooner rather than later.

Ask yourself: are you saving all the money you want to save? If the answer is no, would you like to save more money? Yes. When would be the best time for you to start saving? Today, tomorrow, or 10 years from now?

The answer should be today. But instead of thinking about it, you have to act. You start automating the outcome. You set up automatic withdrawals from your checking account into a Roth IRA. You set up automatic withdrawals out of your paycheck into a 401k or 403b where you get matching funds and tax deductions. You have to automate it.

The key is consistency. Not timing the market. Time in the market. You have to be willing to invest every month, in good markets and bad markets. You do not stop investing when the market goes down. You keep going. That is consistency.

Diversification — Own the Bank, Not Loan to It

The fourth part of the offense is diversification. Roy learned early on something called “become an owner, not a loaner.” Here is how he learned it.

When you were a kid, your parents told you to go open a bank account. You went to the bank and opened a savings account. You thought you were saving money. But what you were really doing was loaning money. You walked into the bank and said, “Here, Mr. Bank, I am going to loan you $100.” They put it in the savings account. Roy asked them, “How much are you going to pay me to borrow my money?” They said, “We are going to pay you 0.25 of 1%.”

Then the next person walked in and said, “I need to buy a car.” The bank said, “Okay, we will loan you that at 13%.” So the bank borrowed it from Roy at 0.25 of 1% and loaned it to the next person at 13%, making 12.75% on the money Roy loaned them.

Roy asks: would you rather own the bank or would you rather loan your money to the bank? Everyone agrees: own the bank. Roy would rather have people loan him money at 0% to 1% and loan it back to them on a car at 13% or on a credit card at 24%, making the spread. It is pretty simple.

So what is the answer? Just buy the bank. That is all you have to do. How do you buy the bank? You own stock in the bank. You own a share of stock, and you get to share in the earnings of what that bank makes. When they start making more money, the stock goes up because it is making more money, and your shares go up.

Roy gives another example. People go to Vegas with a predetermined amount of money they are willing to lose. They say, “I am only going to lose $1,000.” But would you not rather go there and say, “I am only going to make money?” The reason people lose is because it is rigged. The casino has figured out that the odds are in their favor. Blackjack, roulette — they know they are going to win.

So the question is: would you rather be the gambler or own the casino? Roy would rather own the casino. Well, you cannot buy a casino. But you can own stock in a casino. You can own stock in dozens of casinos through a professionally managed fund.

Professional Money Management — The Experts Do Better

Roy learned early on that if you think you are going to outperform professional money managers over a long period of time by picking your own stocks, it is not going to happen. Not going to happen.

Professional money managers have access to research that most individuals will never have. They go on site and meet with C-level executives and employees. They visit research and development departments. For pharmaceutical companies, they go to doctor conventions and meet with patients to find out how drugs are doing. They send information to DC and track regulatory changes. They use tools like Bloomberg to research trends and analyze companies.

Roy visited Capital Group, one of the largest fund groups in the world. He learned that professional money managers do massive amounts of research. They have access to information that individuals do not have. As a result, they consistently do well.

If you put your money with them and concentrate not on trying to hit a home run, but on putting more money in consistently, you will be successful. The key is to raise your income, save 25%, and let professional money managers do what they do best.

Diversification — Different Buckets of Risk

When it comes to your investments, think about business. If you are on the beach and occasionally it rains, you could sell umbrellas. When it is sunny, you could sell sunglasses. When it is raining, you make money. When it is sunny, you make money. That is diversification.

In your investments, you want to have different buckets. You can have stocks, bonds, cash, money markets, and annuities. You can have U.S. companies and international companies. You can have Mercedes Benz (non-U.S.), Chevrolet (U.S.), Mitsubishi (non-U.S.), or Apple (U.S.). You can have small companies, mid-size companies, and large companies. You can have companies that pay dividends and some that do not. You can have high-yield bonds or government bonds.

When you have all these different things, you get diversified. No matter what happens, generally there is something you are happy you had. And when you buy a professionally managed fund, you are not putting it in one stock or one bond. You are putting it into a fund that might have 200 companies that are professionally managed. That is diversification.

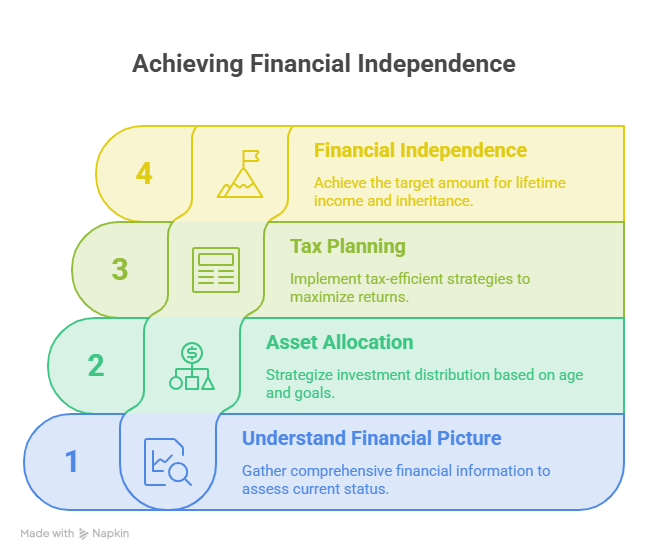

Asset Allocation — Based on Your Age and Goals

When Roy meets with people, he asks a series of questions to understand their complete financial picture. Do you own your home? What is it worth? Do you have a mortgage? What is the rate? Do you have bank cash or CDs? Do you have retirement plans set up? Do you have rental properties? Do you have any other debt? Do you have college plans? How many children? Do you have beneficiaries? Do you have a will or trust? What life insurance? Disability insurance? Health insurance?

Once Roy understands the complete picture, he works on asset allocation. If you are younger, you will be more growth-oriented. If you are older, you will be more preservation-oriented. When you are pulling money for retirement, it is entirely different than when you are investing money.

The goal is to get you to a point where your financial independence number is hit. That is the amount of money needed to provide you a lifetime income that will never run out, and in many cases will have inheritance to pass along.

Achieving Financial Independence

Tax Planning — Multiple Ways to Win

There are different types of tax treatment. You can have tax deferral. You can have tax deductions. You can have tax-free. You can have capital gains tax treatment. There are different ways to organize your money.

Tax-free, for example, a Roth IRA. Tax-deductible, you might do a deductible IRA or 401k where if you put money in, you get to take it off your income taxes. Whether you should do that or a Roth depends on where you are at in life and what your tax bracket is.

Roy looks at retirement accounts from SEPs to 401ks to solo 401ks for self-employed people. He looks at retirement plans through work and helps you choose. He looks at college plans like 529s where you can gift money to kids. He looks at ETFs which have favorable tax treatment. If you buy an ETF today and it grows, when you pass it to your kids, it steps up in value, and they basically get tax-free money with very little taxes.

There are all these different types of things that go into the offense. Tax planning is critical.

Retirement Withdrawal Strategies — Know the Best Way to Pull Money

Once you have built your wealth, you need a withdrawal strategy. Where should you pull money from? What is the best option? Roy had a client yesterday who just retired and was getting his first check. Roy looked strategically at what the best place was to pull money from based on taxation and whether the market is up or down.

You might want to make charitable contributions. Roy had a client who made a charitable contribution to the church but did it as a direct gift from the IRA. That way they avoided having to pay taxes on the IRA. If they had withdrawn the money from the IRA, paid taxes on it, and then made the donation, they would have paid more taxes. A direct donation avoids that.

There are all these different things that go into winning the money game.

Change Your Family Tree — A Family Financial Workshop

Roy did something remarkable with his family. His parents did well. His siblings did well. But he thought about all the kids and grandkids and nieces and nephews. How would they learn? So he created something called a family financial workshop.

He had his nieces and nephews and teenagers come around, and 27 people showed up. Roy told them: “If we do not have a fund set up for you, I am going to gift that to you.” He gifted money to all of his family to set up investment accounts for all the kids, grandkids, nieces, and nephews. Then they did a family financial workshop on Zoom where all the teenagers and young adults and families got together and learned.

Roy has done this many times now. And it has changed family trees. If you want to do a family financial workshop for your entire family, no matter where they live, you can call Roy. You can do it on Zoom. Roy will help you get all your kids going in the right direction.

Teaching Your Kids Early — The Real Wealth Builder

Roy did something similar with his own kids. He had a son who got a job at Wendy’s at age 14 or 15. Roy set up a mutual fund account for him. The son could put as little as $50 a month in. When he made more money, he would send it in. In his early 20s, he had accumulated about $20,000 just from his odd jobs.

Years later, at a seminar, the son raised his hand. He said: “I started when I was 14, 15, 16 years old saving my money, and I was able to take that money and buy a house and put the down payment down. I still have more money in it than I originally invested, and now I am in a home.”

He got started just because his parents said, “Let us get started investing money rather than just going to the bank and doing something boring.”

Roy did the same thing with all his kids. Now, one day he started looking. His parents did really well. His sisters and brother all got started. Then they have big families. His mother just passed away at 102. They have five generations. His mother was born in 1923, and a fifth generation was born in 2023.

That is what happens when you start young and stay consistent. That is how you change your family tree.

The Money Game — You Can Win If You Want To

Roy went on the radio many years ago with Dave Ramsey and started a radio show called The Money Game. It came from a seminar Roy did called “How to Win the Money Game.” It is a money game. If you want to play it to win, you can.

What is the key? There are several keys. The first is you have to get educated. Roy compliments his listeners for listening to the podcast. One listener told him he takes a walk around the block and listens. That is good. That is how you start.

Once you get educated a little, call Roy. If you have not been educated at all, if this is your first time, call him. Roy and his team will get you educated and help you implement a plan.

Visit roymatlockjr.com or call 615-843-2999. Listen to the podcast. Get educated. Then take action. That is how you win the money game.

Listen to the Full Podcast

This episode is a complete walkthrough of the offense — how to build wealth, cut taxes, and pass money to the next generation. Listen to the full June 6, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: June 6, 2026

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.