Build Your Foundation and Hit Your FIN Number

Most people start a new year with good intentions but no real plan. They think about saving more, spending less, or finally getting serious about retirement — but without a clear framework, those intentions fade by February. In this episode of The Roy Matlock Jr. Money and Business Hour, Roy walks through his complete financial foundation system — the same process he has been using since 1993 to make sure every year starts with momentum instead of wishes.

This is not about resolutions. This is about building a foundation, plugging the leaks, and mapping out your path to financial independence with a clear target number and a repeatable system. Whether you are starting fresh or course-correcting from last year, this is your roadmap.

Most People Don’t Plan to Fail — They Fail to Plan

Roy opens with the reality that it does not matter if you earn $50,000 or $500,000 — the principles are the same. You have to know where you are before you can decide where you are going. That starts with treating your finances like building a house: foundation first, then everything else.

The foundation includes four non-negotiables: a working budget, an emergency fund, debt elimination, and income protection. Skip any one of these and the whole structure becomes unstable. Get all four locked in and you are ready to grow.

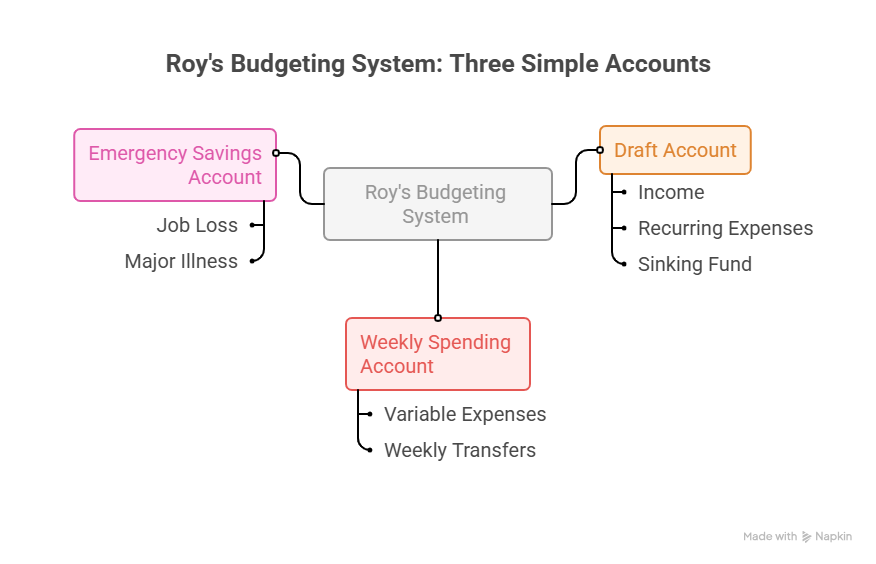

The Budget That Actually Works — Three Simple Accounts

Roy has been teaching this budgeting system for over 30 years, and it eliminates the biggest reason most budgets fail: they do not account for irregular expenses. Here is how it works.

You set up three accounts. First is the draft account where all income lands and all recurring expenses automatically draft out — mortgage or rent, utilities, insurance, retirement contributions, and monthly investment transfers. Inside this account you also build a sinking fund for things that do not happen monthly but always happen eventually: car maintenance, vacations, summer expenses, home repairs, tire replacements. The money builds up over time, and when those expenses hit, the cash is already there. No surprise. No credit card debt.

Second is your weekly spending account. If you are married, you each get one. You move a set amount into these accounts every week for variable expenses like gas, groceries, and eating out. When the week ends, you stop spending. Sunday you move the next week’s amount. This creates real-time awareness and eliminates the drift that kills most budgets.

Third is your emergency savings account — three to six months of expenses sitting in a money market account for true emergencies like job loss or major illness. This is what keeps you from raiding retirement accounts or going into debt when life hits.

Download the budget form at roymatlockjr.com and set aside two hours to build this system. Roy guarantees it will change how you feel about money.

Roy’s Budgeting System: Three Simple Accounts

Fire All Your Expenses and Rehire the Ones That Matter

One of Roy’s most powerful exercises: look at your total income for the year and imagine you had zero expenses. Then go through every single line item on your budget and ask yourself if you would rehire that expense knowing what you know now. Most people who do this save 10 to 15 percent immediately just by cutting subscriptions they forgot about, services they never use, and spending that never mattered in the first place.

This is how you create the gap between income and expenses — what Roy calls your quality of life gap. The bigger that gap, the less stress you carry and the faster you build wealth.

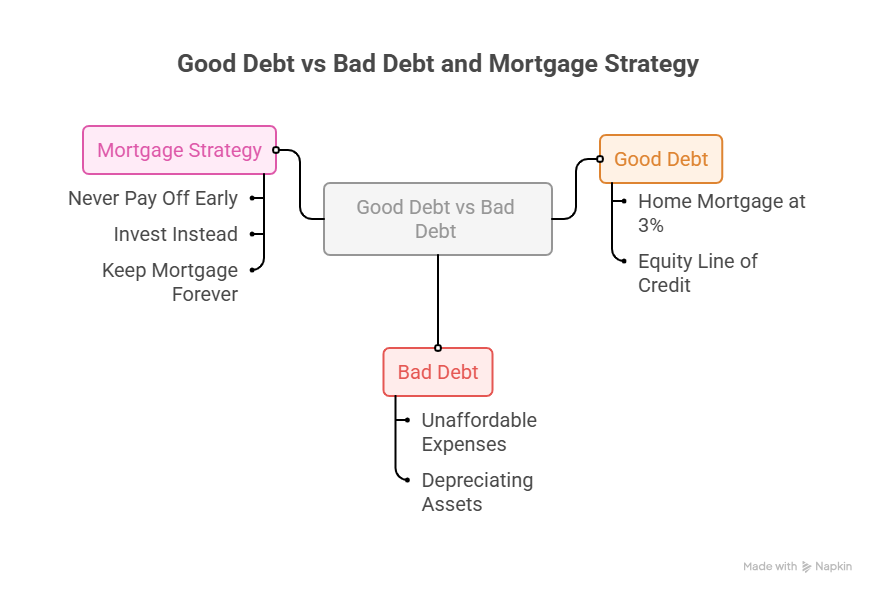

Good Debt vs Bad Debt — And Why You Should Never Pay Off a 3% Mortgage

Bad debt is anything you cannot afford or anything tied to something that loses value. Good debt is affordable and tied to something that appreciates — like a home mortgage at 3%.

Roy is direct on this: do not rush to pay off a low-interest mortgage. You will never see rates like that again in your lifetime. The money you would use to pay it off early is better deployed in investments that earn more than 3%. Keep that mortgage forever.

If you have equity in your home, Roy recommends setting up an equity line of credit even if you do not need it right now. It gives you access to emergency funds and opportunity money when the right investments or situations come along. Just make sure your budget is locked in first before tapping into it.

Good Debt vs Bad Debt and Mortgage Strategy

Seven Quick Ways to Free Up Money to Save

Roy breaks down the practical moves that create immediate breathing room in your finances.

Pay yourself first by setting up an automatic draft to an investment or money market account — as little as $50 a month gets you started. Once it is automated, you forget about it and it just keeps building. Adjust your lifestyle slightly by questioning whether you really need a two-year-old car replaced every cycle or whether the mall trips are adding value to your life. Use the written cashflow plan to bring clarity to what actually matters. Prioritize what is most important and cut what is not.

If you are motivated, earn extra income on the side. Roy mentions that his firm has more demand for financial advisors than people to fill the roles — visit the Join the Team section at roymatlockjr.com if you want to learn the business from the inside while helping people fix their finances.

Realign or sell unused assets. Go through your house and get rid of everything you are not using. Never buy retail again — buy used and immediately cut your personal and business expenses. Roy shares his own story of buying two vehicles new in 2000, immediately regretting it, and never buying new again. His last car was a Mercedes he paid $60,000 for with 20,000 miles on it — the original owner paid $110,000 to drive it that far. That is $50,000 in depreciation someone else absorbed.

The rule: own assets that pay you to own them. Avoid liabilities that cost you money to keep.

Define Your FIN — Your Financial Independence Number

The FIN is the amount of money you need accumulated so that your investments generate enough income for you to live on for the rest of your life without ever working again. Roy’s rule of thumb: 20 times your desired annual income. If you want $100,000 per year in today’s dollars, your target is $2 million.

The path to your FIN is made up of three variables: time, money, and rate of return. You control the first two. Time means starting today instead of waiting. Money means how much you can save each month based on the budget work you just did. Rate of return is where professional money management comes in.

Roy shares a stat from one of the fund families he works with: over 7,517 different 10-year periods going back nearly a century, their funds made a profit 99.8% of the time. They at least doubled the money 80% of the time, tripled it 46% of the time, and quadrupled it 21% of the time. Roy’s takeaway: you are not going to beat professional money managers over the long run. Let them do what they wake up every day to do — grow your money — and pay them a fee for results you could not replicate on your own.

The Secret to Becoming a Millionaire — Get to $100,000 First

Roy breaks down the math on accumulating $1 million at a 10% return. If you have 40 years, it takes $188 per month. If you have 30 years, it takes $500 per month. If you have 20 years, it takes $1,400 per month.

But here is the secret: if you get to $100,000 first and let it sit for 40 years at 10%, you end up with $4.5 million without saving another dollar. If you have 30 years, that $100,000 becomes $1.7 million with no additional contributions. If you have 20 years, you only need to add $476 per month to hit the million-dollar mark.

Roy’s advice for young couples: live on love alone for a few years. If one of you is making $30,000 and the other is making $50,000, live on the $50,000 and bank the entire $30,000 for three years. In three years you have $90,000 to $100,000 saved, and you have set yourself up for life. Stay home, watch TV, sacrifice now, and let compound interest do the rest.

Protect Against Dying Too Soon and Living Too Long

Two risks devastate families financially: premature death and running out of money in retirement.

Term life insurance handles the first risk. Roy ran the numbers: a 30-year-old can get $1 million in coverage for $60 to $106 per month. A 40-year-old pays $100 to $180 per month. A 50-year-old pays $300 to $500 per month for a 20-year term. This is income replacement, not permanent insurance. If something happens five years into the policy and you have paid in $20,000, your family gets $1 million. There is no excuse not to have this in place.

Living too long means not running out of money before you run out of life. The solution is hitting your FIN and structuring withdrawals so your portfolio lasts. That is where diversification across asset classes and professional guidance becomes essential.

Starting the Year off on a Stronger Note — Your Action Checklist

To start this year strong, Roy recommends you complete the following: review all insurance coverages and beneficiaries to make sure everything is current. Max out retirement contributions and at a minimum capture the full employer match — if they match 4%, you put in 4% and you just turned it into 8% with a tax deduction on top. Fund your emergency account and lock in your budget so you are not spending more than you make going forward. Set up automatic drafts for your Roth IRA or investment accounts so savings happens without thinking.

If taxes are a concern, work with a tax advisor to align your deductions and retirement contributions throughout the year. Taxes are the only big bill most people pay without thinking about it in advance — so get a plan in place now.

Ready to Execute Your Plan?

Roy calls himself an implementer of financial independence. The difference between a plan that sits in a notebook and one that changes your life is execution. If you want help building and executing your financial GPS, reach out to Roy’s team for a quick phone call to see if it is a match. Visit roymatlockjr.com or call 615-843-2999.

Listen to the Full Podcast

This episode covers the complete financial foundation process Roy has been refining for over 30 years. Listen to the full November 8, 2025 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: November 8, 2025

Roy walks through every step with real numbers, client stories, and the exact framework he uses to help people build financial independence. This is one of the most actionable episodes you can listen to.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.