The Financial Milestone That Changes Everything

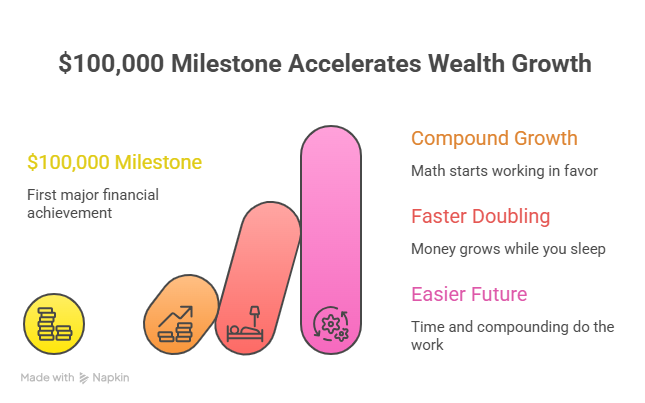

The first $100,000 is the hardest money you will ever save. It is also the most important. Once you hit that milestone, compound growth starts working harder for you. The doubling periods accelerate. The path toward long-term financial independence becomes much clearer.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy focuses on the single most important stage in anyone’s financial life: getting started. If you have not yet accumulated $100,000 in savings or investments, your primary mission should be building that first major milestone. This is where momentum begins.

Roy lays out a practical roadmap for listeners who may feel behind, overwhelmed, or unsure where to begin. The message is simple: building wealth does not require perfection. It requires action, consistency, and a plan. Whether you are young and just starting out or later in life trying to catch up, the same principles apply: grow your income, avoid costly mistakes, automate saving, and stay committed over time.

Why $100,000 Is the Most Important Financial Milestone

Roy has watched thousands of people build wealth over 40 years. The pattern is always the same. The first $100,000 takes the longest and requires the most discipline. But once you reach it, something changes. The math starts working in your favor.

At 10% annual returns, $100,000 doubles to $200,000 in about seven years. That $200,000 doubles to $400,000 in another seven years. Then $400,000 doubles to $800,000. The doubling periods stay the same, but the dollar amounts get larger. The first doubling earns you $100,000. The second earns you $200,000. The third earns you $400,000. You are making money while you sleep, and the amounts keep growing.

That is why the first $100,000 is so critical. It is the foundation that allows compound growth to take over. Everything after that gets easier because time and compounding are doing more of the work.

If you have not hit $100,000 yet, that is your target. Get there as fast as you can. Every dollar you save and invest now is worth more than any dollar you save later because it has more time to grow.

$100,000 Milestone Accelerates Wealth Growth

The Fastest Path Forward — Increase Your Income

Roy emphasizes one thing above all else when it comes to building wealth fast: grow your income. Earning more is often the fastest path to improving your finances. More income creates more opportunities to save and invest. It also creates margin in your budget so you are not constantly stressed about money.

How do you increase your income? Roy breaks it down into a few paths. First, sharpen your skills. Get better at what you do. Become more valuable in the marketplace. The more valuable you are, the more you will earn. Employers pay for results, not effort. If you can produce better results than other people, you will get paid more.

Second, seek promotions or raises. If you have been in the same position for years without a significant raise, it might be time to have a conversation with your boss. Show them the value you bring. Ask for what you are worth. If they will not pay you, someone else will.

Third, consider changing companies. Sometimes the fastest way to increase your income is to leave. Job hopping gets a bad reputation, but if another company will pay you 20% or 30% more to do the same work, that is a massive boost to your savings rate. Do not stay stuck out of loyalty if your company is not rewarding your value.

Fourth, start a side business. Roy has seen countless people increase their income by turning a skill or hobby into extra cash flow. Maybe you are good at graphic design, writing, photography, consulting, tutoring, or handy work. Whatever it is, there is someone willing to pay for it. A side business can add $500, $1,000, or $2,000 per month to your income. That extra money can go straight into investments.

Fifth, consider becoming self-employed. Roy has always said that self-employed people make three to five times as much as employees doing the same work. Why? Because they keep the upside. They do not have someone else taking a cut. The risk is higher, but so is the reward. If you are good at what you do and you are willing to hustle, self-employment can dramatically accelerate your path to $100,000.

The bottom line: income matters. The more you earn, the faster you can save. Focus on becoming more valuable, and your income will follow. If you need help figuring out your complete financial independence strategy, Roy’s blueprint walks you through every step.

Play Defense — Avoid the Mistakes That Slow You Down

Growing your income is offense. Playing defense means avoiding the financial mistakes that drain your money and slow your progress. Roy has seen people earn great incomes and still struggle because they made bad decisions with their money. Do not let that be you.

First, avoid oversized car payments. A brand-new car with a $600 or $800 monthly payment is one of the fastest ways to destroy your ability to save. Cars lose value the second you drive them off the lot. Roy has always bought used cars. He paid cash for a Porsche with 5,000 miles on it and saved $30,000 to $40,000 compared to buying new. You are driving a used car anyway. Why pay new-car prices?

Second, avoid credit card debt. High-interest debt is poison to wealth building. If you are paying 18% or 20% interest on credit cards, you are working for the credit card company, not yourself. Pay off that debt as fast as possible. Once it is gone, do not go back into it.

Third, avoid unnecessary monthly expenses. Subscriptions, memberships, and services add up fast. Go through your bank statements and cut anything you do not use or need. Every $50 per month you free up is $600 per year you can invest. Over 20 years at 10% returns, that $600 per year turns into about $34,000. Small cuts add up to big wealth.

Fourth, avoid insurance gaps. Roy has seen families wiped out because they did not have proper insurance. If you have a family and kids, you need term life insurance. Period. Roy recommends 10 times your income as a minimum. If you make $75,000 per year, you need $750,000 of coverage. Term life is cheap when you are young. There is no excuse not to have it.

You also need disability insurance. If you cannot work because of an injury or illness, disability insurance replaces about 60% of your income. Without it, you are one accident away from losing everything. Roy covers the complete defense strategy in detail — all the insurance, protection, and systems you need to keep your wealth safe.

Fifth, avoid waiting too long to start. Procrastination is the number one enemy of wealth building. The longer you wait, the harder it gets. A 25-year-old who invests $300 per month for 40 years at 10% returns will have about $1.9 million at age 65. A 35-year-old who invests the same amount for 30 years will have about $680,000. Waiting 10 years costs over $1.2 million. Start now.

Build an Emergency Fund — Your Financial Shock Absorber

An emergency fund is three to six months of expenses sitting in cash. Roy has said this for decades. You need a cushion. Life happens. Cars break down. Medical bills hit. Jobs get lost. If you do not have an emergency fund, you will be forced to go into debt or cash out retirement accounts when those things happen.

The emergency fund is not about earning a big return. It is about keeping you from borrowing money, cashing out investments, or paying penalties and interest. That is your return. It keeps you from going backward.

Your first goal is $1,000. Once you have that, work up to one month of expenses. Then three months. Then six months. If you are married and both working, three months is probably fine. If only one of you works, you want six months.

Where do you keep it? A high-yield savings account or money market account. Somewhere you can access it quickly but not so easily that you are tempted to spend it on things that are not emergencies.

Automate Your Investing — Pay Yourself First

Roy has one rule when it comes to saving: if you wait to save money when you have money, you will never have money. Willpower does not work. Automation does.

Set up automatic contributions into your retirement accounts, Roth IRAs, or investment accounts. Have the money drafted from your checking account or payroll every month. You do not think about it. You do not decide whether to save this month. It just happens.

Roy started with $50 per month into a mutual fund and $100 per month into an emergency fund. That was it. Then he bumped it as his income grew. He has been doing that for 40 years. Money goes in automatically. He forgets about it. The account grows.

That is how wealth is built. Small monthly amounts, invested consistently over time, grow into significant wealth. Just as importantly, automation removes the mental burden of having to decide whether to save every month. You set it up once, and it happens whether you think about it or not.

Max Out Your Employer Match — Free Money

If you have a 401k at work and your employer matches contributions, you need to capture the full match. Roy calls this the easiest money you will ever make. It is a 100% return before the money even starts growing.

Here is how it works. Let’s say your employer matches 3% of your salary. You put in 3%, they give you 3%. That is a 100% return immediately. Then you get a tax deduction. If you are in the 25% tax bracket, that deduction saves you about another dollar for every three you put in. So you put in $3, it only costs you $2 after the tax savings, but your account has $6 in it — $3 from you, $3 from the match.

That is free money. There is no reason not to take it. At minimum, you should always capture the full employer match. That is the easiest part of your 10% savings rate right there.

Invest in Low-Cost, Diversified Funds

Once you are saving money, where do you put it? Roy has always believed in professional money management. He does not think individual investors will outperform the professionals over the long run. He learned that lesson the hard way when he was buying tech stocks in the 1990s.

Put your money into highly diversified, professionally managed funds with low costs. Let the professionals do what they are best at. You focus on earning income and living your life. Over time, those funds will grow. The market has averaged about 10% per year for the last 100 years. Some years are up. Some are down. But over time, it grows.

Roy also emphasizes diversification. Do not put all your money in one stock or one sector. Spread it across stocks, bonds, and different asset classes. That reduces your risk and smooths out the returns over time.

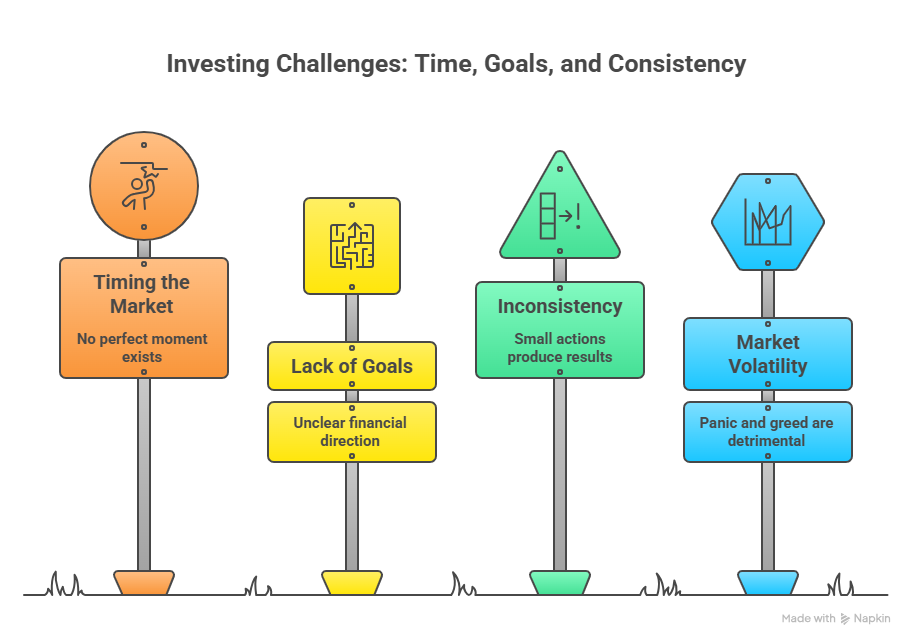

Investing Challenges: Time, Goals, and Consistency

Time Matters More Than Timing

Roy has said this for decades: time in the market beats timing the market. Do not wait for the perfect moment to invest. There is no perfect moment. The best time to start is today. The second best time is tomorrow. Just start.

A 25-year-old who invests $300 per month for 40 years at 10% returns will have about $1.9 million at age 65. A 35-year-old who invests the same amount for 30 years will have about $680,000. A 45-year-old who invests the same amount for 20 years will have about $227,000.

The difference is time. The 25-year-old put in $144,000 over 40 years. The 45-year-old put in $72,000 over 20 years. The 25-year-old ended up with eight times as much money even though they only put in twice as much. That is the power of compounding. The earlier you start, the less you have to put in, and the more you end up with.

Waiting costs you. Every year you delay is a year of growth you can never get back. Start now.

Written Goals and a Clear Plan Accelerate Results

Roy has kept written financial goals since 1986. He knows exactly where he wants to go and what it will take to get there. That clarity makes all the difference.

If you do not have written financial goals, sit down and write them out. What is your financial independence number? How much do you want to have saved? What does your perfect life look like? How much income do you need per month to live the way you want?

Once you have those goals written down, build a plan to reach them. How much do you need to save per month? How long will it take? What rate of return do you need? Break it down into actionable steps.

Roy has a financial independence calculator on his website at roymatlockjr.com under Resources. It will show you with inflation what you need to do. Plug in your numbers. See where you stand. Then build your plan from there.

Wealth Building Is About Consistency, Not Perfection

Roy has said this for years: you do not need to be perfect to build wealth. You just need to be consistent. Small actions taken consistently over time produce massive results. Missing a month here and there is not going to destroy your plan. Quitting will.

Stay committed. Keep saving. Keep investing. Ignore the noise. Do not panic when the market drops. Do not get greedy when the market runs up. Just stick to the plan. Time and compounding will do the rest.

The Best Day to Start Is Today

Roy ends every show the same way: if you want help, reach out. Do not wait. The best day to take control of your money is today.

If you have not started saving, start today. Open an account. Set up a $50 per month draft. Do something. If you already have $10,000 saved, keep going. Get to $20,000. Then $50,000. Then $100,000. Once you hit $100,000, the compounding takes over and the wealth starts building on itself.

But you have to start. No one is going to do it for you. Your future self is depending on the decisions you make today. Make the right ones.

Ready to Build Your First $100,000?

If you want help building your plan, automating your savings, or calculating your financial independence number, reach out to Roy and his team. They are implementers. They do not just give advice — they execute plans and make sure everything is set up correctly.

Visit roymatlockjr.com or call 615-843-2999. You can download free guides, use the financial independence calculator, and open investment accounts for as little as $50 per month.

Everything you need to get started is at roymatlockjr.com/resources.

Listen to the Full Podcast

This episode breaks down the exact steps to build your first $100,000 and create real financial momentum. Listen to the full April 25, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: April 25, 2026

Watch the full video on YouTube: Why Is $100K the Most Important Financial Milestone?

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.