podcast

From Zero to $100K: Your Getting Started Financial Game Plan

Whether you’re in your twenties and thirties just starting your financial journey, or you’re looking to get back on track with less than $100,000 in savings, this guide will walk you through the essential steps to build lasting financial security. With the right plan and automation, reaching your first $100,000 is more achievable than you might think.

The High Cost of Waiting

Here’s a sobering truth: procrastination costs you money. If you’re 25 years old and invest $1,000 per month at 9% for 40 years, you’ll accumulate $4.7 million. But wait just one year? That single year of delay costs you $416,000. Wait five years, and you’ve lost $1.75 million. Wait fifteen years, and the cost of waiting jumps to $3.5 million.

The lesson? Get started now. Time and consistency allow compounding to work in your favor, and every eight-year period at 9% doubles your money. The sooner you start, the more doubling periods you capture.

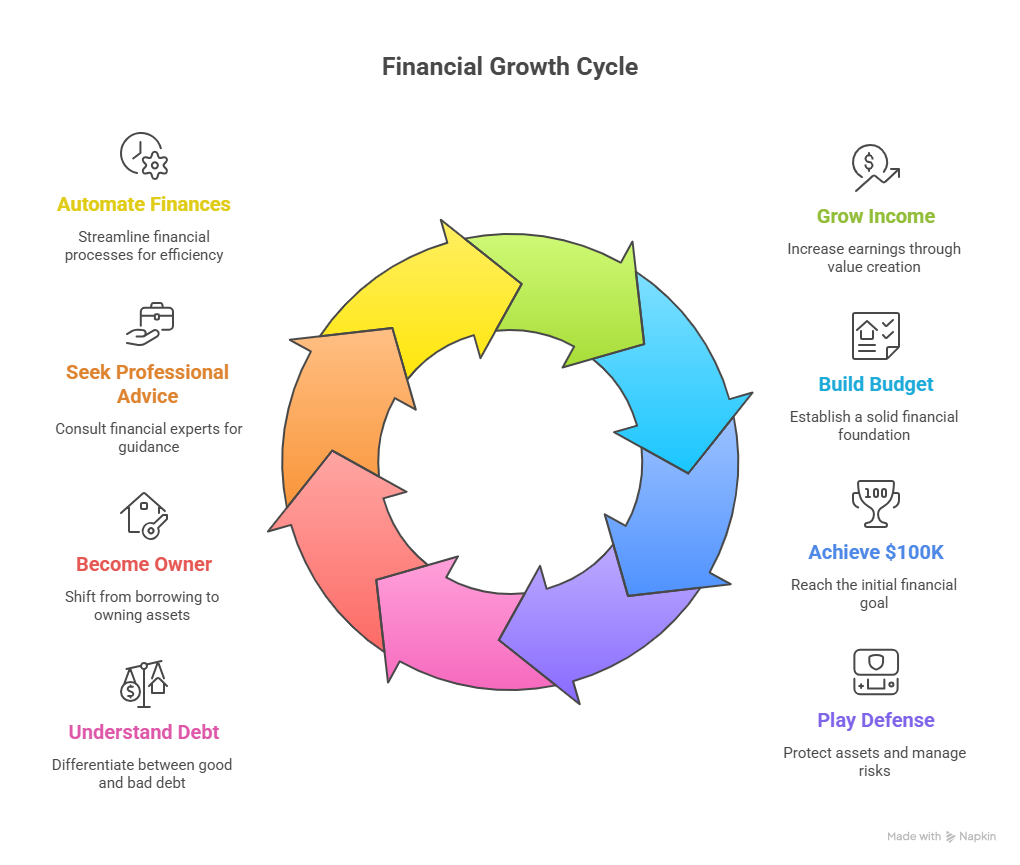

Financial Growth Cycle

Step 1: Grow Your Income Through Value

Before we dive into saving strategies, let’s address the foundation: your income. The most important thing you can do when you’re young is learn how to grow your income by increasing your skill set and value proposition.

Find something you genuinely like doing. When you enjoy your work, you’ll invest the time to become an expert. As your expertise grows, so does your income. Whether you’re working for someone else or building your own business, you want to be the type of person an employer would be scared to lose—or the type of entrepreneur who creates real value in the marketplace.

Target goal: Save and invest 25% of your income. In the worst case, aim for at least 10%, but 25% gets you to financial independence much faster, especially when your income is growing year after year.

Step 2: Build Your Budget Foundation

A budget isn’t an accounting system—it’s a decision-making tool that helps you plan in advance. Here’s how to set up a simple, effective budget:

The Draft Account System

- Total Income: Combine all household income into one account

- Automated Drafts: Set up automatic payments for all recurring expenses (rent/mortgage, utilities, insurance, savings, investments)

- Sinking Fund: Set aside money for predictable but irregular expenses (car maintenance, Christmas, vacations)

- Weekly Allowance: Transfer your remaining spending money to a weekly account with debit cards

This system makes budgeting manageable. You handle it once a week instead of stressing about every transaction daily.

Step 3: The Path to $100,000

So how do you actually get to that first $100,000? Here are your timeframes at 9% return:

- 5 years: $1,392 per month

- 10 years: $547 per month

Most people can achieve this by combining strategies like maximizing employer 401(k) matching funds, contributing to a Roth IRA, and automating their savings. The key is to make it automatic—pay yourself first by having contributions drafted directly from your paycheck or checking account.

Step 4: Play Defense First

Before you focus on growing wealth, you need to protect what you’re building. Here’s your defensive game plan:

Emergency Fund

Build 3-6 months of liquid cash. This safety net allows you to:

- Raise deductibles on insurance (saving money on premiums)

- Drop collision coverage on older paid-off vehicles

- Avoid raiding retirement accounts during emergencies

Insurance Protection

Health Insurance: No excuses. Even health share plans cost just a couple hundred dollars a month.

Term Life Insurance: The cheapest financial protection you can buy. Rule of thumb: 10 times your income. A healthy person in their thirties can get $1.5 million in coverage for around $100 per month. Many policies now include living benefits that allow you to access up to 90% of the death benefit if you develop a chronic illness.

Liability Coverage: Protect your assets with proper home, auto, and umbrella liability policies. Think of an umbrella policy as a “cheap lawyer”—it’s the insurance company’s big-time attorneys protecting you if you’re ever sued.

Step 5: Understand Good Debt vs. Bad Debt

Bad Debt:

- Debt you can’t afford to pay

- Debt tied to things that go down in value (credit cards, car loans)

Good Debt:

- Debt you can afford

- Debt tied to appreciating assets (a house you can comfortably afford, business equipment that generates income)

Pro Tips:

- The best car is a used one you pay cash for

- The best credit card is one that auto-pays from your checking account each month (no interest)

- Never lock yourself into payments you can’t comfortably handle—be conservative

Step 6: Become an Owner, Not a Loaner

Think about Las Vegas. Would you rather be the gambler or own the casino? The casino always wins in the long run. The same principle applies to your money.

When you put money in a bank at 3% but carry credit card debt at 21%, you’re loaning money to the bank at 3% and borrowing it back at 21%. Instead, become an owner by investing in stocks, mutual funds, and businesses.

The Rule of 72

Divide 72 by your interest rate to see how long it takes your money to double:

- 3% doubles in 24 years

- 6% doubles in 12 years

- 12% doubles in 6 years

There are mutual funds with 95-year track records averaging 12% returns. When you’re young and accumulating wealth, you need your money in ownership positions—not sitting in low-interest savings accounts.

Step 7: Work With Professional Money Managers

Professional fund managers have medical degrees, MBAs, and teams of analysts. They attend industry conventions, interview executives, monitor patient responses to drugs, track political environments, and rank investments systematically. They count foot traffic in malls at Christmas with their own counters.

You’re not going to beat these professionals by day-trading on Robinhood. Over the long term, professional money managers deliver consistent results. That’s why young investors should focus on quality mutual funds and let the professionals do what they do best.

Step 8: Automate Everything

The secret to financial success isn’t willpower—it’s automation. Set up:

- Automatic 401(k) contributions with employer matching

- Automatic Roth IRA contributions

- Automatic emergency fund deposits

- Automatic bill payments

When everything runs on autopilot, you remove the temptation to skip contributions or “wait until next month.” You make financial progress whether you think about it or not.

The 11-Point Action Plan

- Grow your income by developing valuable skills

- Create a budget using the draft account system

- Build an emergency fund (3-6 months of expenses)

- Get proper insurance (health, term life, liability)

- Eliminate bad debt (credit cards, unaffordable payments)

- Maximize retirement plans (401k with matching, Roth IRA)

- Buy a home you can comfortably afford

- Set up an estate plan (will, trust, beneficiaries)

- Become an owner (invest in stocks/mutual funds)

- Automate your savings (pay yourself first)

- Work with a financial advisor to create your GPS (Goal, Plan, Strategy)

Your GPS: Goal, Plan, Strategy

- Goal: When do you want to quit working? How much do you need? (Rule of thumb: 20x your annual expenses gives you “do nothing money” at 5% return)

- Plan: How will you get there? How much do you need to save monthly at what interest rate?

- Strategy: Where will you invest? What accounts will you use? What’s your tax strategy?

Common Mistakes That Cost $50K-$500K Over Your Lifetime

- Turning away free money (not taking employer 401k match)

- Paying too much in taxes (not using retirement accounts)

- Carrying bad debt (high-interest credit cards)

- Being under-insured (risking lawsuit or medical bankruptcy)

- Procrastinating (losing years of compounding)

- Keeping too much in low-interest savings

- Not having an emergency fund (forced to raid retirement accounts)

The Bottom Line

You have enough worries in life—why not take money problems off the table? When you spend less than you make and automate your savings, you create what I call a “quality of life gap.” The more months of expenses you have set aside, the more security you feel. Eventually, you’ll have enough months saved that you never have to worry about grinding it out again.

Financial independence isn’t about getting rich quick. It’s about making smart decisions consistently, automating good behavior, and giving compound interest time to work its magic. Whether you’re 25 or 45, whether you have $0 or $75,000 saved, the principles are the same: start now, automate everything, protect what you’re building, and become an owner instead of a loaner.

Your financial future is waiting. The question isn’t whether you can do this—it’s whether you’ll take the first step today.

Listen to the Full Podcast

Want to dive deeper into these strategies? Listen to the complete episode where Roy breaks down each step in detail, answers common questions, and provides real-world examples of how these principles have helped thousands of families build lasting financial security.

Listen to the full podcast episode: “From Zero to $100K: A Getting Started Financial Game Plan”

In this episode, Roy shares personal stories from his 40 years in the financial industry, walks through detailed calculations on the high cost of waiting, and explains exactly how professional money managers pick winning investments. Don’t miss this comprehensive guide to taking control of your financial future.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.