Building Wealth Through Diversification

Over the past few weeks, Roy Matlock Jr. has been walking through the complete A-to-Z financial plan. First came the defense — budgets, emergency funds, staying out of debt, and buying the right insurance to protect your income and assets. Then came the offense — retirement planning, asset allocation, and tax strategies. This week, Roy goes deeper into the investment side: diversification, different asset classes, tax buckets, and the specific retirement accounts you should be using to build real wealth.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy breaks down the complete investment strategy from money markets to stocks, bonds to annuities, and how to organize everything into tax-efficient buckets that maximize growth and minimize what you pay to the IRS.

Diversification — Don’t Put All Your Eggs in One Basket

The foundation of any solid investment plan is diversification. Diversification means you are always happy about something. No single asset class is the best performer every year. Sometimes money markets outperform everything else. Other years, bonds or stocks or annuities take the lead.

When you diversify, you spread your money across different buckets based on your time horizon and risk tolerance. If you are young and just getting started, Roy would put you almost entirely in the stock market with very little outside of growth funds. When the market drops, you are happy because you are buying at a discount through dollar-cost averaging.

But when you retire and start pulling income from your portfolio, market downturns become dangerous. If you are forced to sell shares during a crash to maintain your income, those shares never recover. That is where diversification across different buckets becomes critical. You might pull from bonds or money markets or annuities during down years, leaving your stock portfolio alone to recover.

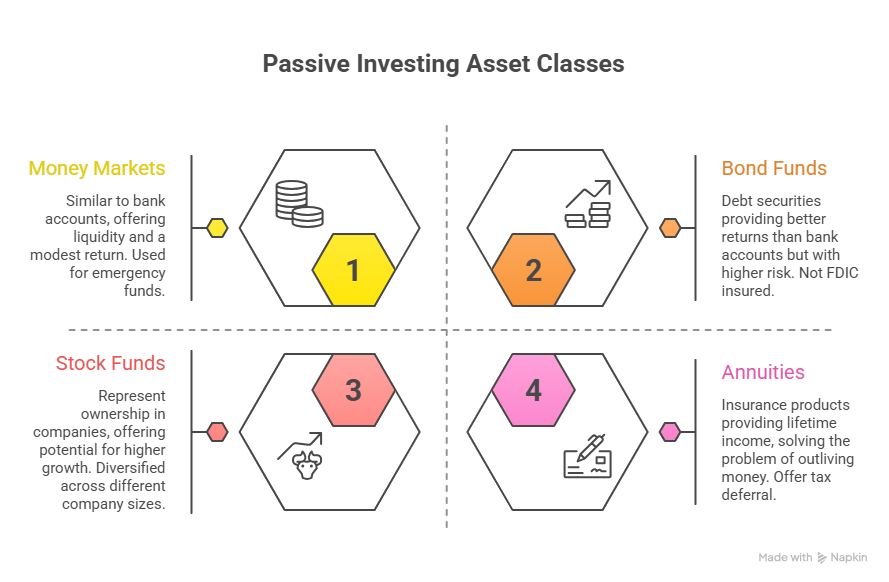

Passive Investing Asset Classes

The Four Main Asset Classes for Passive Investing

Roy organizes passive investing into four main categories: money markets, bond funds, stock funds, and annuities.

Money markets are almost like bank accounts. You can get around 3% right now at major brokerages like Fidelity with full access to your cash. Roy uses money markets for emergency funds and to support higher deductibles on insurance. You save thousands per year in premiums because you have the cash set aside to cover a higher deductible if something happens.

Bond funds are debt securities where companies, municipalities, or governments borrow money from the public. Bonds generally provide a better rate of return than a bank account, but they also carry risk. Unlike a bank account with FDIC insurance, bond funds are not guaranteed. However, bonds have more security than stocks. If a company goes under, bondholders get paid before stockholders. Roy uses bonds for capital preservation and to provide income during years when the stock market is down.

Stock funds represent ownership. Roy explains it like this: when you go to the bank, you loan them money at maybe 1% or 2%. They turn around and loan that money back to you on a credit card at 20% to 27%. Who makes the most money — you at 1%, or the bank making the spread between 1% and 20%? The answer is obvious. So why not own the bank instead of loaning money to the bank?

That is what stock funds do. You become an owner, not a loaner. You own shares in hundreds of companies that have been researched and selected by professional money managers. One fund might hold 200 different companies. You might own small-cap funds for newer high-growth companies, mid-cap funds for companies reinvesting profits instead of paying dividends, and large-cap funds for established companies that pay dividends and provide steady income.

You might also own international funds that invest outside the United States, global funds that invest across the U.S. and abroad, and U.S.-only funds. The whole idea is to diversify across different asset classes so when one sector underperforms, another picks up the slack.

Annuities are insurance products typically bought for income. They solve the problem of outliving your money. Most people buy annuities with the goal of securing lifetime income that never runs out, no matter how long they live. Annuities also offer tax deferral and optional long-term care benefits. Roy shops the insurance marketplace for the strongest companies with the best ratings, and he uses annuities as part of a diversified retirement income strategy.

Eight Different Accounts to Build Your Complete Plan

Roy identifies eight different types of accounts you might use for different purposes as you build wealth.

First is the emergency fund in a money market. This is three to six months of liquid cash you can access when life happens — job loss, health scare, unexpected expense. This is your stay-in-power fund.

Second are retirement funds. These include IRAs, 401ks, 403bs, and other workplace retirement plans. These are the core wealth-building accounts that get tax-advantaged treatment.

Third are college funds. These include 529 plans, Education Savings Accounts (ESAs), and custodial accounts like UTMAs or UGMAs that get favorable tax treatment for education expenses.

Fourth are opportunity funds. These are non-retirement accounts invested in something like a 60-40 stock-bond portfolio. The idea is to have money available for opportunities that come along. You can borrow against these accounts through a margin loan — typically up to 50% of the account value. Roy shares a client story: the client had an opportunity fund and used it to buy out a partner. The return on buying that income stream was far better than 12%. Opportunity funds give you flexibility to act when the right deal appears.

Fifth are non-retirement tax-deferred accounts. This is where annuities come in. You can buy variable annuities that are fully invested in the stock market with all the upside and downside. You can buy RILAs (Registered Index-Linked Annuities) that protect against some loss while giving you limited upside. You can buy fixed indexed annuities that are often used to create guaranteed income streams. All of these grow tax-deferred and are penalized if you withdraw before age 59.5, but they are not technically retirement accounts.

Sixth are funds that can be turned into income, like permanent life insurance policies with cash value. You can borrow against these policies tax-free, providing another income stream in retirement.

Seventh are funds set aside for healthcare and long-term care. You can buy policies with riders that pay out if you need nursing home care or in-home assistance.

Eighth are inheritance funds. These might be a group of ETFs (exchange-traded funds) with better tax treatment than mutual funds. ETFs generate very few taxable dividends, so you pay almost no taxes while the account grows. When you die, your heirs get a step-up in basis. If you put in $10,000 and it grew to $100,000, your heirs inherit it at $100,000 with no capital gains taxes owed. This is a powerful way to pass wealth tax-free to the next generation.

Three Tax Buckets — Organize Your Money by Tax Treatment

Roy organizes money into three tax buckets based on how it gets taxed.

The first bucket is taxable as ordinary income. This includes wages, business income, and withdrawals from pre-tax retirement accounts.

The second bucket is taxable as capital gains and dividends. This includes non-retirement investment accounts where you pay taxes on realized gains and dividend income. Long-term capital gains rates are typically lower than ordinary income rates, which is why ETFs and index funds can be tax-efficient in non-retirement accounts.

The third bucket is tax-deferred. You get a deduction now and pay taxes later. This includes traditional 401ks, 403bs, and traditional IRAs.

The fourth bucket is tax-free. This includes Roth IRAs, Roth 401ks, and cash value in life insurance policies that you can borrow against tax-free. You pay taxes upfront and never pay taxes on withdrawals.

The goal is to have money in all three buckets so you can control your tax bill in retirement. If you need to keep income low to avoid paying taxes on Social Security, you pull from tax-free accounts. If you have a year where income does not matter, you pull from tax-deferred accounts. This kind of flexibility can save tens of thousands of dollars over a 30-year retirement.

Why Stocks Keep Up With Inflation

Roy explains why stocks tend to keep up with inflation better than bonds or money markets. When you witness inflation, you see it everywhere. You walk into McDonald’s and a Big Mac costs more than it used to. If you own stock in McDonald’s, that price increase flows to the bottom line and the stock price reflects it. If you do not own the stock, you just pay more and get nothing in return.

Same thing with Starbucks. If you take the money you would spend on coffee and invest it in Starbucks stock instead, you benefit as inflation drives prices up. Companies price their products to maintain margins, and that shows up in stock prices over time. That is why retirees should always have a piece of their portfolio in stocks — to offset inflation risk. Your Social Security might stay flat, but your expenses keep rising. Stocks help bridge that gap.

But retirees cannot have all their money in stocks because of sequence of returns risk. If you retire and the market crashes, you are forced to sell shares at low prices to maintain your income. Those shares never recover. That is why Roy uses a mix of stocks, bonds, and annuities. When the market is down, you pull from bonds or annuities. When the market is up, you sell from stocks and rebalance. You are never selling at the bottom.

How Bonds Fit Into the Plan

Bonds pay interest and provide more predictable income at a lower rate of return with less volatility than stocks. The main purpose of bonds is capital preservation. If the stock market is down and you have a portion of your money in bonds, you have somewhere to pull income from without selling stocks at a loss.

Bonds carry inflation risk because bond interest rates do not go up when inflation goes up. They also carry interest rate risk. When rates were at historic lows a few years ago and you could get a 3% mortgage, bonds were very risky because if rates went up, bond prices would drop. Now bonds are in a different place. You can get a reasonable return, and if rates drop, you might even get some appreciation.

You can diversify within bonds just like you diversify within stocks. You can buy government bonds, municipal bonds, short-term bonds, long-term bonds, investment-grade bonds, or high-yield bonds (sometimes called junk bonds, though they are not actually junk — they are just companies with more risk than AAA-rated bonds). The whole idea is to spread risk so you are never overexposed to one type of bond.

Annuities — Lifetime Income Guarantees

A lot of people think of annuities as a bond alternative. You can get lifetime income guarantees, guaranteed principal, and tax deferral. Fixed annuities pay a set interest rate with guaranteed principal. Fixed indexed annuities are tied to the stock market with a floor of zero — if the market goes down, you lose nothing, and if the market goes up, you get a piece of the upside.

Roy uses annuities primarily for lifetime income. Around age 70, you can get about 8% for life. If you put in $100,000, you get $8,000 per year guaranteed for as long as you live. Roy tells people to buy lifetime income with the mindset that you hope there is nothing left when you die because that means you lived long and outlived your money. The annuity keeps paying no matter what.

The downside of annuities is surrender charges if you want out early. So when you buy an annuity, you need to go in with the idea that this is long-term money. You are not going to need it for 10 or 15 years, and you want the guaranteed income stream in retirement.

Retirement Plans — 401ks, IRAs, Roth Accounts

Roy walks through all the major retirement account types and how to use them.

401ks come in two flavors: traditional and Roth. Traditional 401ks give you a tax deduction now, and you pay taxes later. Roth 401ks are funded with after-tax dollars, and you never pay taxes on withdrawals. Most employers also offer matching contributions — free money. Roy is shocked by how many people do not even know what their employer match is. If your employer matches 3%, you put in $3 and they give you $3. That is a 100% return right off the bat, plus a tax deduction, plus investment growth. There is no reason not to max this out.

For 2026, you can contribute $24,500 to a 401k if you are under 50. If you are over 50, you get an $8,000 catch-up contribution, bringing your total to $32,500. You can put that into a traditional 401k and deduct it, or you can put it into a Roth 401k and let it grow tax-free.

IRAs also come in traditional and Roth versions. For 2026, the contribution limit is $7,000 if you are under 50, and $8,600 if you are over 50. If your income is under $240,000 for married couples, you can contribute directly to a Roth IRA. If your income is higher, you can use the backdoor Roth strategy.

Here is how the backdoor Roth works. You open a traditional non-deductible IRA and contribute $8,600. Then you immediately convert it to a Roth IRA. Now you just put $8,600 into a tax-free account even though your income was too high to contribute directly. Roy’s high-earning clients do this every year on top of maxing out their 401ks.

Roy also teaches the buy-one-get-one-free strategy. If you max out your traditional 401k at $32,500 and you are in the 25% to 30% tax bracket, you save about $8,000 in taxes. You take that $8,000 tax savings and put it into a Roth IRA. Now you funded a pre-tax retirement account and a tax-free Roth IRA with the same income. You bought one and got one free.

For self-employed people, Roy recommends SEP IRAs or solo 401ks. With a SEP IRA, you can contribute up to 25% of your profit, with a limit of about $70,000 for 2026. If you made $280,000, you could put in $70,000 and deduct it from your income. This is great for independent contractors, realtors, or anyone paid on 1099 commission-only.

Solo 401ks allow even higher contributions on lower incomes because they combine employee and employer contributions. If you are self-employed, this is one of the best tools available.

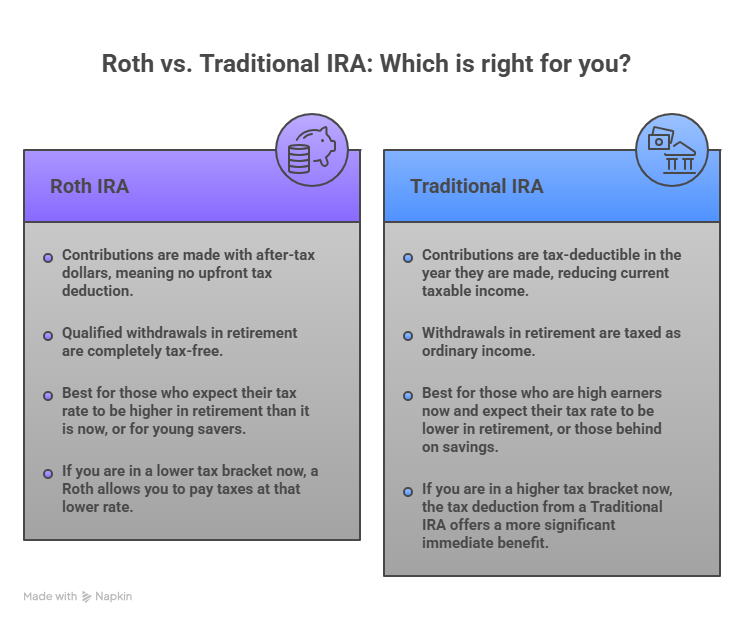

Roth vs. Traditional IRA: Which is right for you?

Roth vs Traditional — How to Decide

Roy’s general rule: if you are young, do Roth. If you are older and a high earner, do traditional and take the deduction.

Why? If you start young and save consistently for 35 to 40 years, your income in retirement might actually be higher than your income now because you accumulated so much wealth. Roy has clients who made more money on their investment accounts last year than they made from their jobs. If that is your future, a Roth makes sense because you pay taxes at a low rate now and never pay taxes again.

But if you are behind on savings and you are a high earner now, the tax deduction is more valuable today than tax-free withdrawals later. You might be in the 30% bracket now and the 15% bracket in retirement. Take the deduction now, save 30%, and pay 15% later. That is a 15-point spread in your favor.

Roy’s daughters are young and have retirement plans through work. He tells them to do Roth. They get started young, let it compound for decades, and retire with tax-free income. That is the power of starting early with the right account type.

The Power of Starting Now — Doubling Periods

The biggest mistake people make is procrastination. Roy shares a simple truth: if you accumulate $200,000 over 25 years and then let it sit for one more doubling period (about seven years at 10%), you end up with $400,000 instead of $200,000. That final doubling period is worth as much as the previous 25 years combined.

Roy has a friend who retired early because he started putting money into the Fidelity Magellan fund when he was 20 years old. Back then, Peter Lynch was managing the fund and averaging about 20% per year. Money doubled every three years. By the time Roy’s friend was 30, he had accumulated serious wealth just by starting young and staying consistent.

Roy tells people: if you can get $100,000 saved by age 30, you have basically secured your retirement. Everything you save after that just shortens the timeline to financial independence.

How do you get $100,000 by 30? Save about $400 to $500 per month for 10 years. Rule of thumb: whatever you put in monthly over 10 years should double if you invest in typical growth funds. So $400 per month is $4,800 per year. Over 10 years, that is $48,000 in contributions. At 10%, that grows to about $96,000. Close to $100,000. That is the goal.

Managing Your 401k Without an Advisor — Target Date Funds

If you do not have an advisor helping you manage your 401k, Roy recommends using target date funds. Here is how they work.

You take your birth year and add 65. Roy was born in 1961. Add 65, and you get 2026. He would choose a 2025 target date fund. If you were born in 1980, you would choose a 2045 target date fund. If you are very young, you might choose a 2070 target date fund.

Target date funds automatically adjust your allocation as you age. When you are young, they are aggressive — mostly stocks. As you get closer to retirement, they shift to bonds and more conservative investments so you do not get crushed by a market crash right before you retire.

Roy also uses a more advanced strategy with clients. He looks at the lump sum you have already saved versus the monthly contributions you are making. If you are near retirement with $1 million saved and contributing $20,000 per year, the $1 million is far more important than the $100,000 you will add over the next five years.

So Roy gets conservative with the lump sum — maybe a 2030 target date fund — but stays aggressive with the monthly contributions, using a 2060 target date fund. If the market drops, those monthly contributions buy at a discount and recover when markets come back. This protects what you have while still taking advantage of dollar-cost averaging with new money.

The GPS for Your Retirement Plan

Everything comes back to Roy’s Financial GPS — Goal, Plan, Schedule.

The goal is where you want to end up. Maybe you want $100,000 per year in retirement. The schedule is when you want to get there — maybe 20 years from now. The plan is how much you need to save each month to hit that target.

Let’s say you already have some money saved, you expect 9% returns, and the calculator tells you that you are short $462 per month. There is your plan. Automate $462 per month into your retirement account, and you just automated your financial independence.

Roy drove out to South Hall last night. He plugged the address into his GPS, and 56 minutes later, he was there. Your retirement plan works the same way. Plug in your destination, follow the directions, and you will get there. The only difference is you have to start the engine. You have to take the first step.

Ready to Build Your Complete Plan?

Roy and his team are fiduciaries who provide comprehensive financial advice. You pay based on the size of your account — typically around 1% to 1.25% for smaller accounts, less for larger accounts. What you are buying is advice, planning, tax strategy, and ongoing portfolio management.

If you want help building your complete investment plan, reach out for a 15-minute phone call. Tell Roy’s team what your goal is, and they will give you answers and advice. If it makes sense to go further, you will meet one-on-one or through Zoom to build a complete plan.

Visit roymatlockjr.com or call 615-843-2999. You can also download the Best Retirement Workbook (12 pages), access budget sheets, open investment accounts for as little as $50 per month or $250 to start, and use the financial calculators to figure out exactly how much you need to save.

Listen to the Full Podcast

This episode covers the complete diversification strategy across asset classes, tax buckets, and retirement accounts. Listen to the full February 28, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: February 28, 2026

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.