The Complete Money Game Plan That Wins Every Time

Most people do not fail with money because they are lazy. They fail because nobody ever sat down with them and showed them a plan. Roy Matlock Jr. has watched this pattern repeat for 40 years. People work hard, earn good money, and still end up struggling because they made bad decisions along the way.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy breaks down his complete money game plan — the defense and offense strategy he has used for 35 years to help thousands of families build wealth and financial independence. This is the same system Roy uses with every client who walks through the door.

The concept is simple. Defense keeps you from losing. Offense helps you win. You need both. If you only play defense, you never build wealth. If you only play offense without protecting what you have, one mistake can wipe you out. Roy learned this from sports, and it applies perfectly to money.

Why Most People Struggle With Money

Just because you know how to make money does not mean you know how to handle the money you make. Roy sees this at every income level. People making $50,000 struggle. People making $500,000 struggle. The income is different, but the mistakes are the same.

The average American has pieces put together but not a complete plan. Maybe they have the right insurance but no investment plan. Maybe they started a 401k but have no idea if it is in the right allocations. Maybe they are saving money but have no emergency fund. Maybe they have investments but no protection if something happens to them.

People are overwhelmed by retirement planning, taxes, insurance, debt, college savings, and everything else that comes with handling money well. They want to do the right thing, but they do not know where to start. That is where Roy and his team come in.

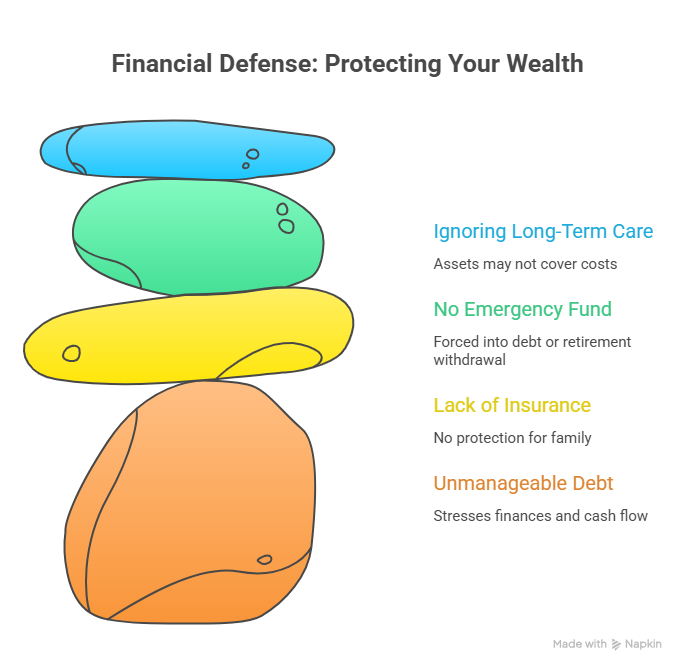

The Defense — Protecting What You Have

Roy always starts with defense. Defense is about keeping you from losing. It is about not giving away points to the other team. In golf, Roy’s philosophy is simple: do not make a big number. Do not take a chance when you should just get yourself back into position and take what you get. The same applies to money.

What is a big number with money? Getting into debt you cannot afford. Buying a house with a payment that stresses you out every month. Buying cars with payments that drain your cash flow. Then when maintenance comes up or an emergency hits, you do not have the money, so you pull out the credit cards. Before you know it, you are underwater. You are spending more than you make every month, and you have no idea how to get out.

Roy lived that reality before he got into the financial business. He had two car payments and a house payment he could not afford. What did he do? He got out from under the two car payments and bought two old cars. He cut three years of car payments into one year of payments. Eventually, he got rid of car payments altogether. That was 1987. Roy has not had a car payment since.

When you do not have a car payment, you make a payment to yourself. When it is time to replace your car, you pay cash and move on. Roy also learned not to buy new cars. Why give away 25% to depreciation driving off the lot? A few months later, you are driving a used car anyway. Buy used from the start and pocket the difference.

Roy learned how to budget. Once he understood how to set up a budget and manage money, he put himself in a good spot. That is the foundation. That is where defense starts.

Defense Part One — Term Life Insurance

The first thing Roy tells people is you have to have term life insurance. That is the starting point. Term life is the cheapest insurance you can buy. If you have kids, debt, a mortgage, and responsibilities, you need coverage. It will blow your mind what $100 per month will do for someone in decent health.

Roy’s firm has a service right now where you can get term insurance up to $2 million if you are healthy. No blood work. No physical. AI does the underwriting, and you get issued in about 10 minutes. That policy includes a do-it-yourself will and trust, plus financial and medical powers of attorney. There is no excuse not to take care of your family.

A lot of insurance policies today have living benefits. That means if you get sick with a critical, chronic, or terminal illness, you can get up to 90% of the death benefit while you are still living. If you are incapacitated and cannot do anything, you can get that money when you need it. That is powerful protection.

Defense Part Two — Protect Your Income and Assets

If you have an income, you may need disability insurance. If you cannot work because of an injury or illness, disability insurance replaces about 60% of your income. Without it, you are one accident away from losing everything. Many employers offer it as part of your benefits package. If you are self-employed, you buy an individual policy.

Health insurance is another critical piece. Roy always bought high-deductible health insurance. Then he switched to health share. Now that he is 65, he is on Medicare. The point is you have to protect yourself. A major medical event without insurance can bankrupt you.

Home and auto insurance matter too. Roy recommends getting the right deductibles, getting rid of junk fees, and buying proper liability coverage. If you have assets, you need an umbrella policy for extra liability protection. If someone sues you, you want to be covered.

As you get older, long-term care becomes important. If your assets are not big enough to withstand a nursing home scenario, especially if you are married, you need a plan. When one spouse goes into a nursing home, it is like getting a divorce but not getting a divorce. One person is home, the other is being taken care of somewhere else. That costs money. You need protection.

Roy covers all of this in his complete defense strategy episode, where he walks through every protection you need to keep your wealth safe.

Defense Part Three — Budgets and Emergency Funds

Defense also means having a budget and an emergency fund. A budget is not an accounting system. It is a planning system. You plan in advance what you are going to do with your money. You can download Roy’s budget form at roymatlockjr.com under Resources. It includes everything — maintenance, car replacement, vacations, emergencies, all the things people forget to account for.

Roy recommends setting up two bank accounts. Account one is a draft account. All your income goes in, and all your bills and savings come out automatically. You pay yourself first. Then you manage your weekly spending. The rest takes care of itself.

An emergency fund is three to six months of expenses sitting in cash. Life happens. Cars break down. Medical bills hit. Jobs get lost. If you do not have an emergency fund, you will be forced to go into debt or cash out retirement accounts. The emergency fund keeps you from going backward.

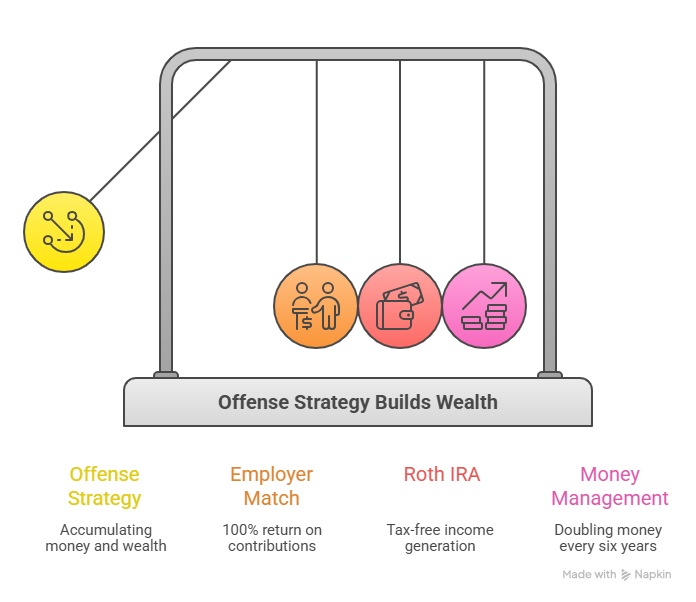

The Offense — Building Wealth and Financial Independence

Once you have the defense in place, you move to offense. This is where the fun starts. This is where you start accumulating money and taking advantage of everything that helps you build wealth.

First, capture your employer match if you have a 401k. Roy calls this the easiest money you will ever make. You put in 3%, they give you 3%. That is a 100% return before the money even grows. Then you get a tax deduction. If you are in the 25% tax bracket, that saves you about another dollar for every three you put in. So you put in $3, it only costs you $2 after the tax savings, but your account has $6 in it. That is free money.

Second, everyone should own a Roth IRA. Why would you not own a Roth IRA? It allows you to set up tax-free income. If you make a lot of money — $250,000 and up — and you are covered by a retirement plan, you can do a backdoor Roth. You contribute to a traditional after-tax IRA, then the next day you convert it to a Roth. Now you have a Roth IRA in addition to funding your 401k.

Third, invest in professional money management. Roy was teaching his advisors yesterday and showed them a fund that has averaged 12% since 1950. It has averaged 12% for the last 15 years, 10 years, 5 years, 3 years, and 1 year. Your money doubles every six years at 12%. Compare that to putting money in the bank at 3%, where it doubles every 24 years. Would you rather double your money every six years or every 24 years? It is that simple.

You could be earning the same amount of money as the person next to you. One of you has money in places with growth opportunities. The other does not. That is the difference. Roy walks through the complete offensive strategy in his wealth-building offense episode.

Investment Management and Asset Allocation

Where should you put your money? If you have a 401k and no one is helping you, Roy recommends a target-date or lifestyle fund. Here is how it works. Take 65 plus your birth year. If you were born in 2000, look at the 2065 target-date fund. It will manage your money as if your target retirement date is 2065. It will be very growth-oriented — mostly stocks — with the idea that long-term you have a big horizon.

If you were born in 1980, you might buy the 2045 target-date fund. If you were born in 1970, you buy the 2035 fund. That same account that started out all stocks will become less aggressive over time. Thirty years from now, it will be more conservative. Within 10 years of retirement, it will turn into a 50/50 stock-bond portfolio. That is the best way to manage if you do not have someone helping you.

Roy does not like target-date funds long-term because they get too conservative when you retire. But if you are not working with an advisor, a target-date fund is a solid starting point.

Tax Strategies — Buy One, Get One Free

Roy loves teaching people tax strategies. One of his favorites is what he calls “buy one, get one free.” If you max out your 401k and get a big tax deduction, use the tax savings to fund a Roth IRA. You get both — the 401k contribution and the Roth IRA funded with the tax savings. That is smart tax planning.

If you own a business, there are SEPs and solo 401ks. Those are mainly for independent contractors. You can put about 25% of your profit into a SEP — up to almost $70,000 — and deduct it. If you do not have employees, a solo 401k allows you to put in an even bigger percentage.

If you are a small business owner competing with big businesses for employees, offering a 401k with matching funds helps. The matching funds are tax credits. They do not cost as much as you think. You also get to put money away for yourself and maybe your spouse. You get a big deduction there. Additionally, you get tax credits that offset the matching funds when you set up a new 401k. If you are interested in that as a business owner, reach out to Roy’s team.

Do-Nothing Money — The Ultimate Goal

Roy’s long-term plan is to get people to do-nothing money. Do-nothing money is investment money that produces income without you having to work for it. You look at the beginning of the month and say, “Oh, that is cool. It got deposited.” You do not have to do anything.

Roy works with a lot of families right now who built up their accumulation plans over the years. Then they retire and ask, “So what do I do now? How am I going to get this money?” Roy sets up a deposit in their account every month. They do not have to do anything. That is do-nothing money.

Wouldn’t everyone like to have do-nothing money? Roy thinks do-nothing money is the only way to go. You just have your account, and you do nothing. How do you get to having do-nothing money? You have to do something first. You have to have a plan.

The First Plan — Get Started Today

What is the very first plan Roy tells someone? Fix it and put a plan in place. Buy term life insurance so if anything happens, you are covered. If you get a policy with living benefits, you get additional protection if you get sick. Then combine that with an automatic draft that comes out of your checking account or payroll into a tax-deferred account — either a Roth or a tax-deductible 401k.

If you do that, you have started on your plan of financial independence. It is that simple. You do not need perfection. You need action. You need consistency. You need a plan.

Real Estate — A Business, Not Passive Income

Roy gets asked about rental properties all the time. There is nothing wrong with rental properties. Just understand that is a business. It is a rental business, and you have to run it like a business. You have to manage it, market it, collect rent, handle maintenance, and do everything any business would do.

If you want to do real estate, Roy has been to many real estate conferences. He grew up around real estate. His mom and dad had real estate. When his dad passed away, Roy had close to 40 properties. He did well with it. But real estate is a game for professionals. You need to stick your toes in it, learn how to do it, and get there. It is not passive income. It is active business income.

Roy does not do rental properties now. Why? Because he does not want to deal with them. He wants do-nothing money. That is investment money that produces income without him lifting a finger. That is his preference.

Why Roy and His Team Are Fiduciaries

Roy and his team are fiduciaries. That means they are required by law to act in your best interest. They are not tied to any one company or any one product. When it comes to money, you only need to call them, and they can give you advice and education and get you situated.

They have access to everything in the insurance market. If you are buying car insurance or home insurance, they can shop it and get you the right coverage with the right deductibles, get rid of junk fees, get the right liabilities, buy umbrella policies, and get a competitive rate.

They have access to all the investment products. They go out and pick what they believe are the best options for you. They are not selling you something because it pays them a higher commission. They are recommending what is best for your situation.

Three Hours of Training Every Week for 40 Years

Roy trains his advisors three hours a week every week. They do it online through Zoom, and they archive it. Roy has maybe six or seven years of three-hour weekly training sessions archived. That is thousands of hours of training on everything you can imagine related to money.

When you meet with one of Roy’s advisors, they know what they are doing. They have been trained. They have watched appointments. They have learned the systems. They know how to build plans. They know how to protect you. They know how to help you build wealth.

If you listen to Roy on the radio, you know he is up to speed on anything having to do with money. His advisors are trained the same way.

Ready to Build Your Complete Money Game Plan?

If you want help building your defense and offense strategy, reach out to Roy and his team. They will do a free consultation to find out if they are a good fit for you. They will walk you through where you are, where you want to be, and how to get there. Then they will build the plan and implement it.

Visit roymatlockjr.com or call 615-843-2999. Check out the resources, download the budget form, and use the financial calculators. Everything you need is at roymatlockjr.com/resources.

Listen to the Full Podcast

This episode breaks down Roy’s complete defense and offense strategy — the system he has used for 35 years to help thousands of families build wealth. Listen to the full May 10, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: May 10, 2026

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.