Build Your Financial GPS: Turn Goals Into a Plan and a Schedule

Define where you want to go (your goal), map the route (your plan), and put it on the calendar (your schedule). Then automate as much as possible so the plan keeps moving—rain or shine.

Your Financial GPS: Goal → Plan → Schedule

Think “GPS” for money: Decide your destination, outline the steps, and set recurring actions that keep you on course.

- Goal: Where do you want to end up? (e.g., €100,000/year in retirement income)

- Plan: What must happen monthly to reach it? (savings rates, allocation, debt strategy)

- Schedule: When will each step run automatically? (draft dates, review cadence, rebalancing)

Find Your FIN: Your Financial Independence Number

A quick way to size your target: Multiply your desired annual retirement income by 20 for a conservative starting point, then adjust for time and inflation.

- Example: Want €100,000/year? Target ≈ €2,000,000 in today’s money.

- Inflation guard: Every ~20 years, double the target (so a 40-year horizon ≈ 4× today’s target).

Next: Subtract what you’ve already saved (and project its growth), then calculate a monthly contribution that closes the gap.

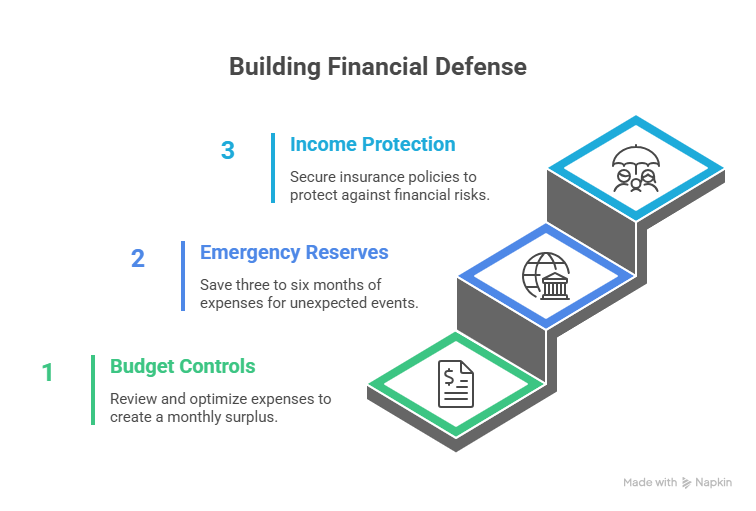

Building Financial Defense

Build the Defense First (So You Don’t Lose Ground)

Defense = protections that prevent costly setbacks.

Budget & Cash-Flow Controls

Fire your expenses once a year: List every recurring cost, “re-hire” only the ones you’d choose today, and aim to create ~25% monthly surplus to deploy to goals.

Emergency Reserves

Three to six months of expenses is your first line of defense. It keeps you from tapping retirement accounts or using high-interest debt when life happens.

Helpful add-on: If you have home equity, consider setting up a home-equity line of credit before you need it as a secondary buffer.

Income & Asset Protection

Starting with these key coverages may be a good path forward: health insurance, term life (income replacement), disability income, auto/homeowners/renters liability, and—later in life—long-term care. Many modern term policies also include living benefits (access to a portion of the death benefit during qualifying critical/chronic illness).

Consider a personal umbrella policy: Often inexpensive and can add €1M+ of liability protection above home/auto limits.

Go On Offense (So You Actually Win)

Offense = growth engine, tax strategy, and smart automation.

Automation Beats Willpower

Pay yourself first: Set drafts on payday to investment accounts and retirement plans. If income fluctuates, use a “minimum draft + quarterly top-ups” model so contributions still happen.

Rule of 72 & Time in the Market

Let compounding do the heavy lifting: Approximate years to double by 72 ÷ rate of return (e.g., ~8 years at 9%). Dollar-cost average through ups and downs rather than trying to time the market.

Allocate—Don’t Accumulate Redundancy

Diversify across asset classes: equities (by size/style/region), bonds (by term/credit), and cash. Check for hidden overlap—four different funds can still hold the same top positions.

Use the Right Buckets

- Tax-advantaged: Workplace plans (with match), IRAs/Roths, HSAs where applicable.

- Tax-deferred: Certain annuities or insurance-based solutions for specific goals and timelines.

- Taxable/liquid: Flexible investing for mid-term needs and opportunistic rebalancing.

Debt: Make It Work for You (or Replace It)

Good debt: Affordable payments tied to assets that can appreciate or produce income (home, business equipment).

Bad debt: High-rate balances tied to depreciating items (e.g., over-financed vehicles, revolving credit).

Simple win: If you’re holding cash while carrying high-rate credit cards, paying down the cards may be your best immediate “return.”

Annual GPS Check: Review, Rebalance, Refresh

Schedule a yearly 60–90 minute review:

- Defense: Emergency fund level, deductibles, coverage limits, beneficiaries, wills/trusts.

- Offense: Performance net of fees, drift vs. target allocation, contribution increases, tax moves.

- Life updates: Job changes, new goals, upcoming large expenses, retirement timeline shifts.

Sequence-of-Returns Awareness (Near & In Retirement)

Avoid selling on the down: Use multiple buckets—cash/money market, bonds, growth assets, and (optionally) guaranteed income tools—so downturns don’t force equity sales to fund monthly needs.

Put It All Together: A Sample “Financial GPS” You Can Copy

Goal: €100,000/year retirement income (today’s euros), retire in 25 years.

Plan: Save €X/month (automated), 80/20 growth-tilted allocation today, glide down risk gradually in the last 5–7 years, clear all bad debt in 18 months, keep 4 months’ expenses in cash, review annually in May.

Schedule:

- 1st/15th monthly: Auto-draft to retirement/taxable accounts.

- Quarterly: Top-up contributions if income exceeded baseline; check overlap among funds.

- Annually (same month each year): Full defense/offense review, rebalance, beneficiary check, raise savings rate by 1–2% if cash flow allows.

Quick Wins You Can Do This Week

- Calculate your FIN: Desired annual income × 20 (then adjust for time to retirement).

- Automate: Set a draft you’ll actually keep—even a modest start builds momentum.

- Harden the defense: Top up emergency fund; review umbrella liability and deductibles.

- Consolidate stranded accounts: Old workplace plans often deserve a rollover so you can truly allocate and monitor.

- Declutter overlap: Check top holdings across funds to ensure you’re diversified, not duplicated.

Need a Second Set of Eyes?

A short advisory call can surface blind spots and convert your ideas into a concrete GPS. If you’re unsure about allocation, overlaps, or beneficiary setup, that’s a great place to start.

🎧 Listen to the full episode: Turn Goals Into a Plan and a Schedule

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.