The Boring Stuff That Builds Financial Freedom

Roy Matlock Jr. has been talking about money since 1992. After 40 years in the business, he has learned one thing for certain: most people wonder why their money is not working for them, and the answer almost always comes back to the same thing — they just do not plan.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy walks through the boring stuff that actually builds financial freedom. This is not about chasing 10% returns or finding the next hot investment. This is about protecting yourself, avoiding mistakes, and automating your path to financial independence. If you have too much month at the end of the money, this is the system that fixes it.

Start With Your Financial GPS — Goal, Plan, Schedule

Everything begins with knowing where you are going. When you order an Uber, the first thing the app asks is where you want to end up. Then it tells you what it costs and how to get there. Your money works exactly the same way.

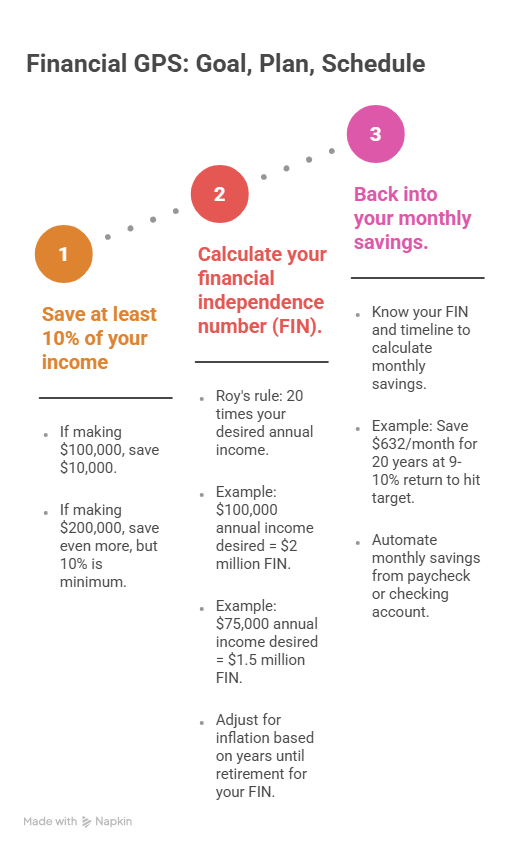

Roy’s Financial GPS system stands for Goal, Plan, Schedule. The goal is your financial destination. The plan is how you get there. The schedule is when you arrive.

Step one: save at least 10% of your income. If you are making $100,000, you need to save $10,000. If you are making $200,000, you should be saving even more, but 10% is the minimum.

Step two: calculate your financial independence number. Roy uses a simple rule — 20 times your desired annual income. If you want $100,000 per year in retirement, your number is $2 million. If you want $75,000 per year, your number is $1.5 million. Adjust for inflation based on how many years until you retire, and you have your FIN number — your financial independence number.

Step three: back into your monthly savings. Once you know your number and your timeline, you can calculate how much you need to save every month. Let’s say you need to save $632 per month to hit your target in 20 years at a 9% to 10% return. You automate that $632 out of your paycheck or checking account every single month, and you just automated your financial independence.

You have to know the numbers. Without a target, you are just guessing.

Financial GPS: Goal, Plan, Schedule

The Budget — Planning vs Accounting

The most important thing you can do to get your money right is to get on a budget. But a budget is not an accounting system. Most people confuse the two.

An accounting system counts up what you already spent. A budget preplans what you are going to spend and keeps you on track. That is the difference, and it matters.

You can download Roy’s budget form at roymatlockjr.com. Here is how it works.

First, fire all your expenses. Go through every line item and decide if you really need it and if you really want to rehire it. Some expenses you cannot get rid of immediately — you might be stuck in a car payment or a lease. But you can make a plan to get out of them.

Roy shares his own story. In 1986, he had two car payments totaling $600 per month. He thought he was cool buying two new cars. When he realized how stupid that was, he worked to pay them down, got out from being upside down, bought two cheap cars, paid those off immediately, and never had another car payment. That is the mindset you need.

Once you have fired your expenses and decided what to keep, you set up what Roy calls a draft account. One hundred percent of your income goes into this account. If you are married, all household income flows into one place.

From that account, you pay everything on paper first. You set aside money for future expenses — maintenance, car replacement, Christmas, vacations, all the irregular stuff that comes up. You pay yourself first by automating your 10% savings. You pay all your recurring bills. And then you fund your weekly spending money.

Roy recommends using two debit cards for weekly spending if you are married. Every Sunday, you move your budgeted weekly spending onto those cards — let’s say $200 per person. You set up automated daily text alerts that tell you how much you have left. Now all you have to do is manage $200 per week. Anyone can do that.

At the end of the week, you check your balance. If you only spent $172, you have $28 left. You move that $28 into your investment account and reload $200 for the next week. If you are under budget, you are winning.

When maintenance comes up or you need to replace a car, the money is sitting in your draft account waiting. You pull it out and pay cash. You are on track.

This is how you automate financial discipline. Your bills are automated. Your savings are automated. You only manage your weekly spending, and the system takes care of the rest.

The Power of Managing What You Measure

Roy has come to a simple conclusion after decades of working with people: anything you put on paper and manage, you improve by 20% right off the bat. It does not matter what you are trying to accomplish — fitness, finances, business growth — if you write it down and track it, you get better.

When you start budgeting this way, magic happens. You realize you are saving money. You realize you spent less than $200 this week on miscellaneous expenses. You realize you are under budget. You realize your credit card debt is gone. You cannot believe it.

Why is all of this happening? Because you planned on it.

You used to live paycheck to paycheck. Now you do not. That is what planning does.

The Emergency Fund — Your Real Rate of Return

An emergency fund is designed to give you stay-in power. That means three to six months of expenses sitting in cash. If you are married and both working, three months is probably fine. If only one of you works, you want six months.

People always say they do not want money sitting there earning nothing. But that is not how you measure the return on an emergency fund. The return comes from what you avoid losing.

If you lose your job and you have six months of expenses saved, you can keep paying your mortgage. You do not have to pull from your retirement account and pay penalties. You do not have to rack up credit card debt at 20% interest. You do not lose your house. That is your return — avoiding the things that cost you money.

An emergency fund also lets you raise your deductibles on insurance. Roy carries only liability coverage on one of his cars because he has the cash to replace it if he totals it. That saves him several thousand dollars per year in premiums. He carries high deductibles on his home and auto insurance and his health insurance. Lower premiums every month because he can afford the risk.

You can also be more self-insured. If your car breaks down, you pay cash and keep moving. No stress, no debt, no drama.

The emergency fund keeps you from paying penalties for not having the emergency fund. That is how it works.

Here is how you build it. Let’s say you need $20,000 saved. You automate a monthly draft into a money market account. Right now, money markets are paying around 3.5%. Once the account hits $20,000, you redirect that monthly draft into long-term retirement savings. Simple, automated, done.

Good Debt vs Bad Debt

Debt will erode your ability to save if you do not manage it correctly. The key is knowing the difference between good debt and bad debt.

Bad debt has two characteristics. First, you cannot afford the payment. If making the payment stresses you out, that is a red flag. Second, it is tied to something that goes down in value. Car loans, credit cards, financing depreciating assets — all bad debt.

Good debt also has two characteristics. First, you can easily afford the payment. Second, it is tied to something that goes up in value. A mortgage on a home you can afford is good debt. A loan for business equipment that grows your revenue is good debt. Borrowing to buy rental property that cash flows is good debt.

Roy is very clear on this: you never finance depreciating assets. Depreciating things are not even assets. An asset is something that grows in value.

That is why having a mortgage is fine as long as you can afford it and still save your 10%. But paying off a low-interest mortgage early is one of the worst financial decisions you can make. If you have a 3% mortgage, your rate of return on paying it down is 3%. Put that money into investments that can grow at 9% or 10% instead.

Roy calls low-interest mortgages gold. They are like free money. Do not pay them off early. Invest the difference.

Debt Management for Financial Growth

Set Up a Home Equity Line of Credit

If you have more than 20% equity in your home, Roy recommends setting up a home equity line of credit even if you do not need it. You do not have to use it, but it gives you access to liquid cash if an emergency happens or an opportunity comes along.

Banks are funny. They love to loan money to people who do not need it, and they hate to loan money to people who do need it. So set up the line of credit when your income is high, your credit is strong, and everything is good. Then you have it if you ever need it.

Protect Your Income — Life Insurance and Disability Insurance

Insurance is designed to protect either your income or your assets. Let’s start with protecting your income.

There are two types of life insurance: term and permanent. Term insurance is what you buy if you die unexpectedly while you still have young kids, a mortgage, and people depending on your paycheck. You buy it for a specific term — usually 10 to 35 years — and the premium stays the same for the entire term.

Roy’s rule of thumb: 10 times your income plus enough to pay off debts and set aside education funds for your kids. So if you and your spouse each make $50,000 per year and you have a $300,000 mortgage, you might each need $1 million of term insurance. A young, healthy person can get $1 million of term coverage for less than $100 per month.

Why would you not do that? If something happens to you, your kids are taken care of. Your spouse is not financially destroyed. Your family can keep the house and move forward. You cannot replace the person, but you can replace their earning power.

Roy’s firm can issue up to $2 million of term life insurance in about 10 minutes if you are in good health. It even includes a will and trust. There is no excuse for not having it. Call 615-843-2999 or visit roymatlockjr.com to get it done today.

Once you reach financial independence — let’s say you have $2 million saved and can live off 5% returns — you do not need term insurance anymore. You bought it for a term, and now the term is over.

Permanent coverage is different. It is designed for when you die, not if you die. It provides an estate, covers funeral and medical expenses, and replaces income lost when one Social Security check goes away after a spouse passes. Roy typically recommends variable life or indexed universal life for permanent coverage. These policies can last as long as you live.

Disability insurance replaces your income if you cannot do your job. If you are a surgeon making $500,000 per year and you break your hand, you cannot do surgery anymore. You might be able to do other work, but it will not pay $500,000. Disability insurance covers the gap.

You typically buy coverage for about 60% of your income. Insurance companies will not let you buy more than that because they do not want you making more money disabled than you would working. The goal is to indemnify you back to where you were, not give you an incentive to stop working.

Protect Your Assets — Health Insurance, Home and Auto, Umbrella Policy

One of the number one causes of bankruptcy is people not having health insurance. And the crazy thing is, most people who do not have it could get it cheap. If your income is low, you qualify for government subsidies. There is no excuse for being uninsured.

Roy has always carried high-deductible health insurance because he has an emergency fund. He has had $1,500 deductibles and $7,500 deductibles for years. High deductibles mean lower premiums, and he has the cash to cover the deductible if something happens.

He also negotiates. When he needed an MRI on his hand, the quoted price was $1,700. He asked for the cash price. They said $450. He paid $450. If you are not going to hit your deductible anyway, why pay full price? Always ask for the cash price.

Health savings accounts are another tool. If you are married, you can contribute over $8,000 per year and deduct it from your taxes. Once you hit age 59.5, you can take that money out tax-free just like a Roth IRA. It is a great way to save on taxes while building a medical fund.

For home and auto insurance, raise your deductibles as your emergency fund grows. Move from a $250 deductible to $1,000 or $2,500. Your premiums drop, and you have the cash to cover the deductible if needed. Make sure your coverage keeps up with inflation so you can actually replace what gets damaged.

Also look at your liability coverage. If you hit a Mercedes and do not have enough liability coverage, you are getting sued and paying out of pocket. That is where an umbrella policy comes in.

An umbrella policy is additional liability coverage on top of your home and auto insurance. Roy calls it a cheap lawyer. He once got sued after a minor fender bender with a delivery truck. The guy saw Roy’s car and thought he could cash in. Roy had an umbrella policy. He had a couple of phone calls with the insurance company’s lawyers, and that was the end of it.

Umbrella policies cover personal liability, injuries at your house, car accidents, anything where someone might sue you. They are inexpensive and worth every penny.

Public Adjusters — Get What You Deserve on Insurance Claims

Roy brings up an important point for anyone dealing with property damage right now, especially after the recent storms in Nashville. If you have damage to your home, you need to know about public adjusters.

When you file a claim, your insurance company sends an adjuster. That adjuster works for the insurance company. The insurance company is a for-profit business, and their adjuster might overlook damage you do not even know about because you are not a professional.

You settle the claim, and two years later you find out your drywall has to be torn out because of mold. But the insurance company already paid, and now you are stuck with a huge bill.

A public adjuster works for you, not the insurance company. They get you about twice as much money on average, and they typically charge based on the increase they get you. If you have any type of damage, reach out to roymatlockjr.com and Roy’s team can connect you with a vetted public adjuster.

Long-Term Care and Estate Planning

Long-term care insurance protects your assets if you end up in a nursing home or need in-home care. You can buy standalone policies, but Roy typically recommends adding riders to annuities instead. You put in $100,000, it grows at 3% tax-deferred, and if you need long-term care, they pay out up to three times that amount. If you never need care, the money still grows and passes to your heirs.

Finally, you need a will and trust. If you have any assets or children, you need healthcare and financial powers of attorney. You need a living will so your kids are not stuck making life-support decisions. Get it done. Roy’s team has vetted estate planning attorneys they can refer you to if you need help.

The Complete Defense Strategy

Here is everything Roy covered in this episode.

You set up your financial GPS — goal, plan, schedule. You automate 10% savings. You calculate your FIN number and back into your monthly target. You build a real budget using the draft account system. You manage weekly spending with debit cards and daily balance alerts. You build a three to six month emergency fund. You eliminate bad debt and only keep good debt. You set up a home equity line of credit when you do not need it.

You buy term life insurance — 10 times your income plus debt payoff and education funds. You buy disability insurance to replace 60% of your income if you cannot work. You get health insurance with high deductibles to save on premiums. You raise deductibles on home and auto insurance. You buy an umbrella policy for liability coverage. You use public adjusters for property damage claims. You add long-term care riders to annuities. You set up a will, trust, and powers of attorney.

That is your defense. This is the boring stuff that keeps one surprise from wrecking your entire financial life. The average financial mistake costs $50,000 to $500,000 over a lifetime. Your defense is designed to avoid those mistakes.

Once your defense is locked in, you can go on offense. That is where retirement plans, asset allocation, tax-advantaged investing, and wealth transfer strategies come in. Roy will cover the offense in the next show.

Ready to Build Your Defense?

Everything begins with education. If you are reading this, you are already ahead of most people. The next step is advice. Roy believes that working with a great financial advisor is the least expensive thing you will ever do because it makes you money. His team cuts taxes, shows people better ways to structure their finances, and helps them avoid costly mistakes every single day.

If you want help building your financial defense, reach out for a 15-minute phone call. Visit roymatlockjr.com or call 615-843-2999.

Listen to the Full Podcast

This episode walks through the complete defensive foundation for financial independence. Listen to the full February 14, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: February 14, 2026

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.