Financial Disciplines That Will Shape Your 2026

As Roy Matlock Jr. kicks off year eight back on the air and his 40 year in the financial business, he is still answering the same question: when are you going to retire? His answer never changes — never. Why would he retire when he is having fun? That mindset is exactly what separates people who build lasting wealth from those who work hard but never quite get ahead.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy breaks down the financial disciplines that will shape your 2026 and beyond. These are not motivational speeches or temporary fixes. These are the habits that decide outcomes, and if you get them right, the rest takes care of itself.

The Rules of Money Work Like Gravity

Roy looked up the definition of discipline and found this: the practice of training people to obey rules or a code of behavior, with punishment or other undesired consequences for those who fail to comply.

There are rules when it comes to money. If you follow them, they work like gravity — predictable, reliable, and consistent. If you ignore them, you get consequences. You do not need someone standing over you enforcing these rules. The enforcement happens automatically through your bank account, your stress level, and your quality of life.

Good habits create good outcomes. Bad habits create bad outcomes. Discipline always beats motivation. Small decisions, if you take care of the little money, the big money takes care of itself. Delay gratification now, and you will be happier later.

Your Financial GPS — Goal, Plan, Schedule

Roy uses the same GPS framework he has been teaching for decades. When you get in your car and plug in a destination, the GPS asks where you are going, maps out the route, and tells you when you will arrive. Your money works the same way.

The goal is your financial destination. Roy’s rule of thumb: 20 times your desired annual income is when you can retire or achieve financial independence. If you want $100,000 per year, your target is $2 million. If you want $75,000 per year, your target is $1.5 million. That number becomes your goal.

The schedule is the timeline. Are you going to hit that number in 30 years? 20 years? 40 years? Once you have a goal and a deadline, you can reverse-engineer the plan.

The plan is the monthly action steps that get you there. How much do you need to save every month? What rate of return do you need? What accounts should you use? This is where the system gets built.

Roy has been self-employed for 45 years. Nobody tells him to get up in the morning. Nobody forces him to be anywhere at a certain time. But he learned early on that the schedule is the most important thing. If you know you have to be somewhere at a certain time, you will do better. He remembers doing a live radio show with Dave Ramsey for nine years, five days a week, starting at 1:00 PM sharp. Not 1:01. One o’clock. He was never late in nine years. That kind of discipline carries over into everything else.

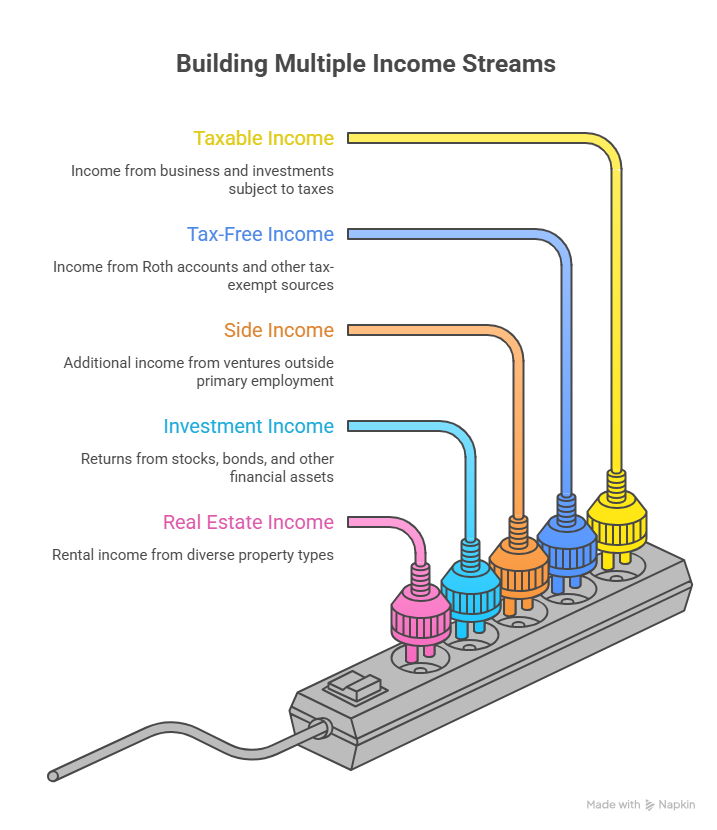

Building Multiple Income Streams

Columns of Income — Build Multiple Streams

Roy always works on building columns of income. He does not rely on a single source. He has taxable income from his business, investment income from his portfolio, tax-free income from Roth accounts, and side income from other ventures. If one stream dries up, the others keep flowing.

You should be doing the same thing. If you have a job, get a side business. If you have a business, diversify your revenue. If you own real estate, spread it across different property types. The goal is to build four or five income streams so that no single event can knock you out.

And within those income streams, always be working on your income. Roy had 18 consecutive years of double-digit income growth before the 2008 crash. How? He got better at what he did. He worked hard. He got smarter. He invested in himself. If you want to improve your financial life, one of the fastest ways is to become better at what you do and demand more money for it.

Live Below Your Means — Create the Quality of Life Gap

Living below your means does not mean living a miserable life. It means creating a quality of life gap between your income and your outgo. You are not overstretching. You are not stressed. You are not constantly worried about money.

That does not mean you never take risks. If you start a business, you will put capital at risk. But you always make sure you have income streams in place so one bad decision does not wipe you out.

The first step is knowing where you are. Maybe 2025 was great. Maybe it was terrible. Either way, you are where you are. You can complain about it, or you can lock in the behavioral changes you need to move forward. Roy’s advice: lock in the changes and move forward.

Get Started Now — Procrastination Costs You Everything

Roy keeps a book on his desk called Common Sense by Art Williams, written about 40 years ago. The first principle in that book is get started now. Roy has watched people procrastinate for years, and it kills him every time. They say they are not quite ready. They want to wait until they understand it better. They want to save a little more before they start investing.

Meanwhile, years go by and nothing happens.

Roy shares a story about his father, who passed away 25 years ago. Before he died, his father set up five $25-per-month investment accounts for Roy, his siblings, and grandkids. Roy’s mother is now 102 years old, and those accounts have been running on autopilot for decades. Roy forgot about them. His sisters forgot about them. Nobody touched them.

Those $25-per-month accounts — about $7,500 in total contributions — are now worth over $30,000. That is do-nothing money. Set it up, forget about it, and let compound interest do the work.

That is what happens when you just get started. You set it up once, automate it, and never look back. It is like Netflix — once you sign up, you never cancel it. Your retirement savings should work the same way.

Pay Yourself First — Automate Everything

The second discipline after getting started is paying yourself first. This is non-negotiable. Before you pay any bill, before you spend a dollar on anything else, you pay yourself.

Here is how Roy sets it up. All income goes into what he calls a draft account. From that account, everything is automated — mortgage, utilities, insurance, and most importantly, savings. If you have a 401k at work, you are capturing the full employer match. If you are self-employed, you have automatic drafts pulling money into investment accounts every month.

You also fund three types of accounts from this draft system. First is the emergency fund — about three months of expenses sitting in cash. This fund is not really an investment, but it gets a great return by keeping you from paying penalties, cashing out retirement accounts early, or going into debt when life happens. Second is what Roy calls the opportunity fund — money set aside with no specific purpose, but it is invested and growing. This is cash that is available if a good opportunity comes along. Third is your retirement accounts — 401k, IRA, Roth IRA, whatever you have access to.

All of this is automated. You do not think about it. It just happens every month. Roy set up his first $50-per-month account 40 years ago. Fifty dollars per month at 10% for 40 years is about $250,000. That is money you forget about, but it grows in the background while you live your life.

You can open investment accounts today for as little as $50 per month or $250 to start. Roy encourages people to set up what he calls a spend it or save it account. If you decide not to go out to dinner and save $50 instead, you pull out your phone, transfer $50 to your investment account, and it is done in 30 seconds. Just like you can buy anything on Amazon 24 hours a day, you can invest the same way.

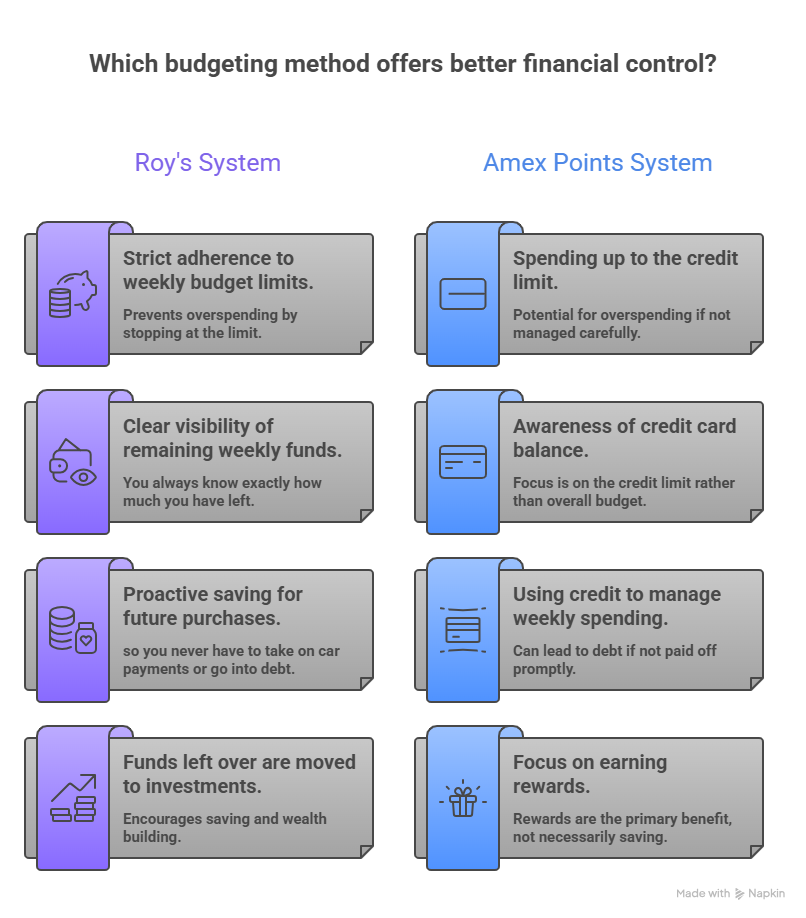

Which budgeting method offers better financial control?

The Budget — Weekly Spending and Predetermined Decisions

Roy’s budgeting system is simple. You list all your expenses — recurring bills, irregular expenses like car maintenance and vacations, everything. You compare that to your income and make sure there is a gap. Inside that budget, you set aside money for future purchases so you never have to take on car payments or go into debt for things you know are coming.

Once you know your numbers, you set up the draft account and automate all the bills. Then you take your weekly spending money and move it into a separate checking account or load it onto a debit card. If your weekly budget is $500, that is what you move over. When the week ends, you stop spending. If you have money left, you move it into your investment account.

Roy has clients who like using their American Express to earn points. That is fine — just move your weekly budget onto the card as a credit, spend it down through the week, and when you hit your limit, you are done. At the end of the week, you load the next week’s budget.

This system keeps you in control. You always know exactly how much you have left for the week. You are not guessing. You are not hoping. You know.

Reframe Spending — What Does That Purchase Really Cost?

Roy thinks differently about money, and he encourages you to do the same. If you want to win with money, you cannot follow the crowd. You have to go in a different direction.

Here is how Roy reframes spending. If you are looking at a $1,000 purchase and you are 25 or 30 years old, you should not be asking if it is worth $1,000 today. You should be asking if it is worth what that $1,000 will become over time.

One thousand dollars invested at 10% becomes $2,500 in 10 years, $6,700 in 20 years, $17,000 in 30 years, and $45,000 in 40 years. So when you are standing in front of that fancy whatever-it-is, you are not deciding if it is worth $1,000. You are deciding if it is worth $45,000.

Most of the time, the answer is no.

That does not mean you never enjoy life. Roy has traveled, played golf, and done plenty of fun things. But he always set money aside first, and then he worked on growing his income so he could afford the fun stuff without sacrificing his future.

The time value of money is real. A thousand dollars spent today is zero in 40 years. A thousand dollars invested today is $45,000 in 40 years. That difference is what separates people who retire comfortably from people who work until they die.

Build Your Defense — Protect Income and Assets

Before you go on offense with investing and wealth-building, you need a solid defense. Defense is about protecting what you have and avoiding mistakes.

Your defense includes an emergency fund, a working budget, term life insurance with living benefits, disability income insurance, health insurance, liability coverage on your home and car, and an umbrella policy if you have significant assets. These are the things that keep one bad event from wiping you out.

Term life insurance is the one product everyone with a family should own. It protects your income in case you die unexpectedly. The new living benefit riders let you access the death benefit early if you are diagnosed with a chronic, critical, or terminal illness. This is not just death insurance anymore — it is life insurance.

You also need estate planning documents. If you have accumulated money and you want your life’s work to go where you intend instead of probate court or family fighting, you need a will, a trust, healthcare and financial powers of attorney, and a living will. If you are young with kids, it should terrify you to not have something in place to make sure your children are taken care of if something happens to you.

Once your defense is locked in, you can go on offense.

Go on Offense — Professional Money Management and Tax Strategy

Offense is about growing wealth efficiently. That means using professional money managers, taking advantage of tax breaks, and letting compound interest do the heavy lifting.

Roy learned early on to use professional money management. He has been putting clients into funds that started in 1934 — nearly 100 years of track record. Those funds have doubled investors’ money every six years for almost a century. How? They do research. They visit companies. They meet with CEOs and employees. They talk to customers and industry experts. They rank companies and invest in the best ones.

You are not going to beat that on your own. You might get lucky for a year or two, but over decades, the professionals win. Your job is to go make a lot of money in your career or business. Their job is to grow the portion of that money you set aside for retirement.

You can access these kinds of funds through financial advisors. Typical fees are around 1% to 1.25% for advice, plus about 0.5% for the underlying fund management. When you net it all out, these managers have been delivering 10% to 12% annually, doubling your money every six to seven years.

Use the calculators at our Resources section to model different scenarios and see how professional management compounds over time.

You also need to take advantage of tax breaks. Max out your 401k and capture the full employer match. Fund a Roth IRA. If you are a high earner, use the backdoor Roth strategy. If you are self-employed, use a SEP IRA or solo 401k to defer even more income. These are the tools that let you save more and pay less in taxes.

Teach Your Kids — Start Them Early

One of the smartest things you can do is teach your kids about money while they are young. Roy has done family financial workshops where teenagers learn what a mutual fund is, how compound interest works, and why starting early matters.

He remembers showing his kids different funds on a website and letting them pick which one to invest in based on what companies were in the fund. One of his sons saw Nintendo and GameStop in a fund and said he wanted that one. That is how kids learn — by seeing it, touching it, and watching their own money grow.

If you start your kids on $50 or $100 per month when they are teenagers, by the time they are in their twenties, they could have six figures saved. Roy has clients whose kids are doing exactly that. One client’s son just got married at 24 with over $100,000 in investments. That is what happens when you start early and let time do the work.

Systems Beat Motivation Every Time

Roy’s final point is this: systems beat motivation. You cannot rely on being motivated to save money or invest or stick to a budget. Motivation fades. Discipline lasts.

That is why everything Roy teaches is about automation. Set it up once, and let the system run. You pay yourself first automatically. Your bills get paid automatically. Your budget resets every week automatically. You never have to think about it.

Roy has been putting his written goals on paper since 1986. A couple of weeks ago, he found his 1986 business plan and showed it to his team on Zoom. He still has the original paper — not just a picture. He reads those goals regularly because he wants to brainwash himself into staying on track and making good decisions unconsciously.

That is what discipline looks like. You do not wait to feel like it. You set up the system, and the system makes the decisions for you.

Ready to Lock In Your Disciplines?

Roy and his team are fiduciaries who have been doing this for 41 years. They automate outcomes for clients every day. If you want help building your financial disciplines and setting up systems that work, reach out for a 15-minute phone call. Visit roymatlockjr.com or call 615-843-2999.

Listen to the Full Podcast

This episode walks through every financial discipline Roy has used for 40 years to build wealth and help clients do the same. Listen to the full January 10, 2026 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: January 10, 2026

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.