The Retirement Blueprint: Accumulation to Lifetime Income

Retirement planning is not about picking a date on the calendar and hoping everything works out. It is about building a system that transitions you from earning a paycheck to generating reliable income that lasts as long as you do — whether that is 20 years or 40 years.

In this episode of The Roy Matlock Jr. Money and Business Hour, Roy walks through the complete retirement blueprint from the accumulation years through the distribution phase. This is the same framework Roy has used with clients for 40 years, and it works whether you are just starting out, in your peak earning years, or already retired and pulling income.

Retirement Is Not an Age — It Is a Cashflow Transition

Roy is direct about what retirement actually means. It is not about turning 65 or hitting some magic number. Retirement happens when you have enough cashflow coming in that work becomes optional. That is the only definition that matters.

Your financial independence is measured by how many months you can survive without any income. Three to six months of emergency cash is the first goal. From there, you keep pushing that number higher — one year, five years, ten years, and eventually unlimited income that never runs out no matter how long you live.

Roy himself is turning 65 in January after 40 years in the financial advisory business, and he plans to keep working until the day he dies. Not because he has to, but because he loves it. If you genuinely enjoy what you do, there is no reason to stop. But if you are counting down the days to retirement because you hate your job, that is a signal you need to find work you actually like — not just wait for some arbitrary retirement age.

Retirement Planning Challenges

The Two Phases — Accumulation and Distribution

Building wealth and living off wealth require completely different strategies, and most people do not make the transition well because they treat retirement the same way they treated their working years.

The accumulation phase is all about growth, savings, and discipline. You automate contributions, chase higher returns, take advantage of tax breaks, and ride out market volatility because you have time on your side. A market crash when you are 35 is an opportunity to buy at a discount. You want the market to stay down so you can load up on cheap shares.

The distribution phase is about income, protection, and tax efficiency. You cannot afford to take the same risks because a big market drop right when you retire can destroy your entire plan. This is called sequence of returns risk, and it is one of the most dangerous threats retirees face.

Roy shares the math: if the market is up the first two years of retirement, you can pull 4% annually, increase withdrawals 3% per year for inflation, and 30 years later your portfolio is worth more than when you started. But if the market drops 20% in the first two years and you keep pulling the same amount, you are forced to sell extra shares to maintain your income. Those shares never recover, and you could run out of money entirely. Same portfolio, same withdrawal rate — completely different outcome based on timing.

That is why retirees need a completely different strategy than accumulators. You need protection against sequence of returns risk, and that means building the right buckets.

Procrastination Is the Number One Killer of Wealth

The biggest mistake people make is waiting. Waiting for the right time to start saving. Waiting for a raise. Waiting until they understand investing better. Waiting until they have more money to set aside. All of that waiting adds up to decades of lost compound growth.

Roy’s solution is simple: automate everything. Set up automatic contributions to your 401k. Set up automatic bank drafts to investment accounts. Make savings a bill that gets paid before anything else. He compares it to Netflix — once you sign up, you never cancel it. The money just keeps coming out every month, and eventually you forget it is even happening. That is exactly how retirement savings should work.

Roy works with clients who started their kids on $50 or $100 monthly investments when they were teenagers. Now those kids are in their twenties with six figures saved. One client’s son just got married at 24 with over $100,000 accumulated. That is what happens when you start early, automate contributions, and let compound interest do the heavy lifting.

Build Multiple Income Streams — Become Bulletproof

Roy emphasizes the importance of having more than one way to make money, both during your working years and in retirement. If you have a job, get a side business. If you have a business, diversify your revenue streams. If you own real estate, spread it across different property types and locations.

A side business gives you tax benefits, extra income, and something to fall back on if your primary income disappears. Roy’s firm offers a licensed referral partner program for people who want to learn the financial business on the side while keeping their day job. Visit the Join the Team section at roymatlockjr.com to learn more.

The same principle applies in retirement. You do not want to rely on a single source of income. Social Security, pensions, investment withdrawals, annuity payments, rental income — the more streams you have, the more bulletproof your retirement becomes. If one stream dries up or underperforms, the others keep you afloat.

Tax Buckets — Taxable, Tax-Deferred, and Tax-Free

One of the most powerful tools in Roy’s system is organizing money by tax treatment. Most people think of their money as one big pile, but Roy divides it into three tax buckets that each serve a different purpose.

Taxable accounts are bank accounts and brokerage accounts where you pay taxes every year on dividends, interest, and capital gains. These accounts are fully liquid — you can access the money anytime with no penalties. You need some money here for emergencies and opportunities, but you do not want too much sitting in taxable accounts because you are paying taxes on money you are not even using.

Tax-deferred accounts are retirement plans like 401ks, 403bs, traditional IRAs, and annuities. You get a tax deduction when you contribute, the money grows without being taxed, and you pay taxes when you withdraw it in retirement. This is where the bulk of most people’s retirement savings lives. Roy calls it “buy one, get one free” — you fund a pre-tax account and use the tax refund to fund a Roth IRA, giving you both tax deferral and tax-free growth.

Tax-free accounts are Roth IRAs and Roth 401ks where you pay taxes upfront and never pay taxes on the growth. You can also access tax-free money by borrowing — loans are not taxed, so a home equity line of credit or a loan against life insurance gives you tax-free cash without triggering a taxable event.

Having money in all three buckets gives you flexibility in retirement. If you need to keep your income low to avoid paying taxes on Social Security, you pull from tax-free accounts. If you have a year where income does not matter, you pull from tax-deferred accounts and take the tax hit. This kind of tax planning can save tens of thousands of dollars over a 30-year retirement.

Risk Buckets — Conservative, Mid-Range, and Growth

Roy also organizes investments by risk level into three buckets: conservative, mid-range, and growth.

Conservative buckets include money markets, bonds, CDs, and fixed annuities. These do not go down when the market crashes, but they also do not grow much. You need money here for short-term income needs and to protect against sequence of returns risk. When the market drops, you pull from this bucket and leave your growth investments alone.

Mid-range buckets include balanced funds with a mix of stocks and bonds — maybe 60% stocks and 40% bonds. These give you some growth potential with less volatility than pure stock funds. Roy uses these for opportunity money — cash that is not earmarked for anything specific but could be deployed if a good opportunity comes along.

Growth buckets are stock funds and ETFs designed for long-term appreciation. This is where the real wealth-building happens, but it comes with volatility. You need time to ride out the ups and downs, which is why younger investors should have most of their money here and retirees should have less.

When you combine tax buckets with risk buckets, you create a complete system that works in any market environment. Market up? Pull from growth and rebalance. Market down? Pull from conservative and let growth recover. Need to minimize taxes? Pull from tax-free. This is how you build a retirement that cannot be broken by market crashes or tax surprises.

Why Professional Money Managers Beat DIY Investors

Roy has been in the business for 40 years, and he rarely sees individual investors who consistently outperform professional money managers over the long run. You might get lucky for a year or two, but over decades, the professionals win.

Why? Managing money is their full-time job. They have access to research, resources, and information that retail investors do not. They spend every day looking for opportunities and avoiding risks. And their track record is completely transparent — you can see exactly how well they have performed over 10, 20, or 30 years.

Roy works with funds that have been around for nearly 100 years. One of his core recommendations has doubled investors’ money every six years for a century. That kind of consistency is nearly impossible to replicate on your own, especially while juggling a career and a life outside of investing.

Your job is to go make a lot of money in your career or business. Their job is to grow the portion of that money you set aside for retirement. Let the professionals do what they are best at, and focus your energy on what you are best at. Use our Calculators section to model different scenarios and see how professional management compounds over time.

Take Advantage of Every Tax Break Available

Tax-advantaged accounts are how you supercharge your savings, and Roy walks through all the tools you should be using.

Max out your 401k or 403b and capture the full employer match — that is free money. If you get a tax deduction, take the refund and stick it in a Roth IRA. This is the “buy one, get one free” strategy — you fund a pre-tax account and use the tax savings to fund a tax-free account.

If you are a high earner who makes too much to contribute directly to a Roth IRA, use the backdoor Roth strategy. Contribute to a non-deductible traditional IRA and immediately convert it to a Roth. Now you have tax-free growth with no income limits.

For 2026, contribution limits increased. If you are over 50, you can now contribute $8,600 to an IRA or Roth IRA. Health savings accounts also went up. Roy had a client call him this week asking to bump his contributions by $50 per month to hit the new $8,600 limit. That simple adjustment puts him on track to maximize his tax benefits for the year.

These are the tools that let you save more, pay less in taxes, and build wealth faster. Use them.

The Retirement Income Strategy — Guaranteed Income Plus Growth

When you retire, Roy’s typical strategy is to split your portfolio into guaranteed income and growth investments. About one-third goes into an annuity or other guaranteed income source. The other two-thirds stays invested in a diversified portfolio of stocks and bonds.

The annuity gives you a baseline income that never runs out, no matter how long you live or what the market does. For a 65-year-old couple, a $500,000 annuity pays roughly 7.5% to 8% annually — about $40,000 per year for life. Add that to Social Security and you have a floor of guaranteed income you can count on every month.

The rest of the money stays invested for growth so it can keep up with inflation and give you flexibility. Roy typically uses a 60-40 or 75-25 stock-bond allocation depending on risk tolerance and income needs. When the market is up, you pull from the stock portion and rebalance back to your target allocation. When the market is down, you pull from the bond portion or money market and leave the stocks alone to recover.

This is how you avoid the sequence of returns disaster. If you are 100% in stocks when a crash hits and you are forced to sell shares to maintain your income, those shares never recover. But if you have guaranteed income covering your baseline expenses and conservative buckets to pull from during down years, your stock portfolio can stay invested and come back when markets recover.

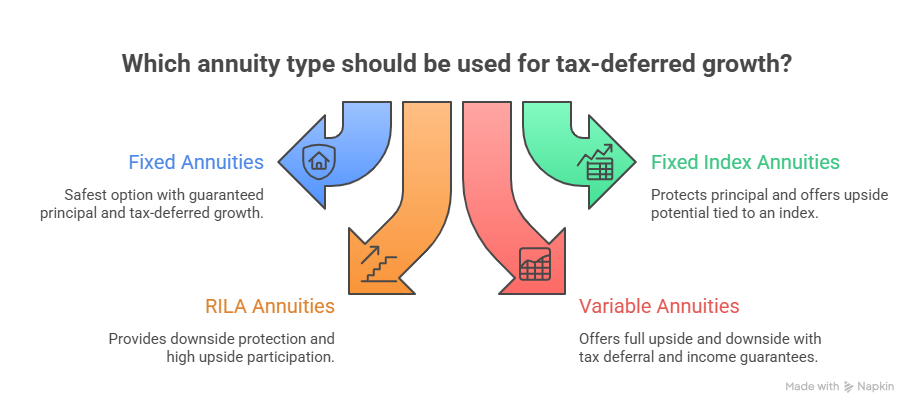

Which annuity type should be used for tax-deferred growth?

Types of Annuities and When to Use Them

Not all annuities are the same, and Roy explains the four main types.

Fixed annuities are the safest — slightly better return than a bank CD, guaranteed principal, and tax-deferred growth. Fixed index annuities protect your principal completely. If the market goes down, you lose nothing. If the market goes up, you get a piece of the upside tied to an index like the S&P 500. RILA annuities (Registered Index-Linked Annuities) offer 10% to 20% downside protection over a six-year period and give you most of the upside — currently around 90% to 100% participation in market gains. Variable annuities give you all the upside and all the downside with tax deferral and optional lifetime income guarantees.

All annuities share three core benefits: tax deferral, the option for guaranteed lifetime income, and special riders like long-term care coverage. Some annuities let you and your spouse each contribute $50,000, and if you need long-term care, they pay out three times that amount. If you never need care, the money still grows tax-deferred and passes to your heirs.

Roy is meeting with a client this Friday who has money he never expects to touch — it is inheritance money for his kids. That money is going into an annuity for tax-deferred growth. No required minimum distributions, no annual tax bills, and it grows until he passes it down to the next generation.

Adjust Your Strategy as You Get Closer to Retirement

As you approach retirement, your strategy needs to shift. Roy asks a simple question: what is more important to your retirement — the money you have already saved, or the money you are going to save between now and retirement?

When you are young, the answer is obvious — most of your retirement wealth will come from future contributions. So you stay aggressive with everything. But as you get older and your portfolio grows, the money you have already saved becomes more important than future contributions. At that point, Roy gets more conservative with the lump sum while staying aggressive with monthly contributions.

Here is how it works. You are 58 years old with $500,000 saved in your 401k. That $500,000 is the foundation of your retirement. If it drops 40% right before you retire, you are in serious trouble. So Roy shifts that money into a more conservative allocation — maybe 60-40 or even 50-50 stocks and bonds. But your ongoing 401k contributions? Those stay 100% aggressive, buying into stock funds every month. If the market drops, those contributions are buying at a discount and will recover when markets come back.

This strategy protects what you have while still taking advantage of dollar-cost averaging with new money. It is how you avoid getting crushed by bad timing while staying positioned for growth.

Rebalance and Review Annually

Retirement planning is not a set-it-and-forget-it event. It is a living plan that needs to be reviewed and adjusted as your life changes.

Roy meets with clients once per year to rebalance portfolios, decide where to pull income from, and adjust allocations based on market conditions and life changes. If the market had a big run and your stock allocation drifted from 60% to 70%, you rebalance by selling some stocks and buying bonds. If the market dropped and you are pulling income this year, you decide whether to take it from conservative buckets or tap into required minimum distributions from tax-deferred accounts.

This annual review process keeps your plan on track and prevents emotional decision-making. You are not reacting to daily market noise. You are following a system that has been proven to work over decades.

The Complete Blueprint

Here is Roy’s full retirement system from start to finish.

Start by building an emergency fund of three to six months of expenses. Eliminate bad debt. Automate contributions to retirement accounts and take advantage of every employer match. Use professional money managers and diversify across asset classes and tax buckets. Max out contributions to 401ks, IRAs, Roth accounts, and health savings accounts.

As you approach retirement, shift accumulated wealth into more conservative allocations while keeping new contributions aggressive. When you retire, convert a portion of your portfolio into guaranteed lifetime income through annuities or pensions. Keep the rest invested in a diversified mix of stocks and bonds. Pull income strategically based on market conditions — from growth when markets are up, from conservative when markets are down, from tax-free when you need to minimize taxes.

Meet with your advisor annually to rebalance, adjust withdrawals, and make sure your plan still matches your life. Set up a living trust and estate plan to transfer wealth smoothly to the next generation.

This is the blueprint. It works. And if you follow it, you will never run out of money.

Ready to Build Your Retirement Blueprint?

Roy and his team are implementers — they do not just give advice, they execute plans and make sure everything is set up correctly. If you want help building your retirement strategy from accumulation through distribution, reach out for a 15-minute phone call. Visit roymatlockjr.com or call 615-843-2999.

Listen to the Full Podcast

This episode walks through Roy’s complete retirement blueprint from accumulation through income distribution. Listen to the full December 20, 2025 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: The Retirement Blueprint – From Accumulation to Income You Can’t Outlive

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.