Start Smart, Finish Strong: Your Lifetime Financial Blueprint

Financial independence isn’t achieved overnight—it’s built through intentional decisions at every stage of life. Whether you’re just starting your career, raising a family, or approaching retirement, having a clear roadmap can transform your financial future. This comprehensive guide walks you through the essential strategies for building wealth from your twenties through retirement.

The Foundation: Ages 20-35

Fix Your Income Problem First

The path to financial security starts with a simple truth: if you’re struggling financially, you have either an income problem or a spending problem. The good news? Both are solvable.

Love what you do. People who are passionate about their work rarely have income problems. Why? Because they invest the time to become excellent at it. When you’re great at what you do, opportunities follow—whether through promotions, raises, or the confidence to start your own business.

If you’re not there yet, give yourself permission to explore. By age 30, you should have tried different paths, changed directions when needed, and discovered something that truly motivates you. Don’t confuse quitting with pivoting—you’re not giving up, you’re finding your fit.

The Seven Essential Steps for Young Adults

1. Build Your Team of Trusted Advisors

Learn from people who are already where you want to be. Better yet, study those who are struggling financially and do the exact opposite. Surround yourself with mentors, financial advisors, and successful individuals who can guide your journey.

2. Master the Budget and Emergency Fund

Your budget should have three components:

- Draft Account: All income flows in, all automated bills flow out

- Upcoming Expenses: Set aside money for irregular costs like holidays, vacations, and car maintenance

- Weekly Living Money: Transfer a set amount to your debit card each Sunday—when it’s gone, it’s gone

Build an emergency fund covering 3-6 months of expenses. This single step prevents you from sliding into debt when life happens.

3. Buy the Right Insurance

Protect your income and assets with term life insurance, disability coverage, health insurance, and liability protection. Insurance isn’t about being pessimistic—it’s about being prepared.

Here’s something that should shock you: A 30-year-old in standard health can get a $1 million, 20-year term life insurance policy with living benefits for around $100 per month. If you qualify for preferred rates, it drops to about $60 per month. There’s simply no excuse not to protect your family.

4. Understand Good Debt vs. Bad Debt

- Good debt: Tied to appreciating assets you can afford (like a home with a 15-year mortgage at 15-20% of your income)

- Bad debt: Tied to depreciating assets you can’t afford (like credit cards, expensive cars, or houses beyond your means)

5. Set Up Your Estate Plan

Even young adults need wills, trusts, financial power of attorney, and healthcare directives—especially if you have children.

6. Automate Your Investments

Start with retirement accounts that offer matching contributions. If your employer matches your 401(k), that’s free money. Put in $3, get $6 with the match, plus a tax deduction? That’s like handing someone $3 and receiving $7 back.

7. Reach $100K by Age 30

This is your first major milestone. How do you get there?

- 5-year plan: Invest $1,391/month at 9% returns = $100,000

- 10-year plan: Invest $547/month at 9% returns = $100,000

Why does $100K matter? Because at 8% growth, money doubles every nine years. Your $100K becomes $200K in nine years—without adding another dime. That $200K becomes $400K in another nine years. Compound interest is your best friend, but only if you start early.

The Quality of Life Gap

Here’s a critical concept: The gap between your income and expenses determines your quality of life. If you’re spending more than you earn, you have no quality of life—you have stress.

As your income grows, resist the temptation to inflate your lifestyle at the same pace. Grow your income, maintain your expenses, and invest the difference.

The Accumulation Years: Ages 35-55

You’ve built your foundation. Now it’s time to scale.

From $100K to $1 Million

With your first $100,000 saved, your next goal is seven figures plus Social Security. Here’s how to get there:

- 10-year plan: $100K + $4,000/month at 9% = $1 million

- 20-year plan: $100K + $715/month at 9% = $1 million

- 30-year plan: $100K + $0/month at 9% = $1 million

Your strategy depends on your timeline and capacity to save. The key is having a GPS: Goal, Plan, Schedule.

Maximize Your Contributions

This is when you should be aggressive with retirement savings:

- Max out 401(k) contributions, especially if there’s employer matching

- Open and fully fund Roth IRAs

- Consider supplemental retirement vehicles like cash-value life insurance with tax-free growth potential

Aim to invest 25% of your income during these peak earning years.

Diversify Your Asset Allocation

Your investment portfolio should balance growth with security:

- Conservative bucket: Money market accounts, stable value funds

- Moderate bucket: Balanced funds, bonds, growth annuities with principal protection

- Growth bucket: Stock funds, equity investments

A classic 60/40 stock-bond allocation works well for many people in their 40s and 50s, though everyone’s situation differs.

Tax Strategy Matters

Your biggest expense isn’t your mortgage—it’s your taxes. Create a tax diversification strategy with three types of accounts:

- Taxable accounts: Regular brokerage accounts

- Tax-deferred accounts: Traditional 401(k)s and IRAs

- Tax-free accounts: Roth IRAs and certain life insurance policies

Prepare for Healthcare Costs

In your 50s, consider long-term care planning. Products purchased now can protect you from devastating healthcare costs later in life.

Should You Pay Off Your Mortgage?

One of the worst pieces of common advice: pay off your low-interest mortgage before retirement. If you have a 3-4% mortgage you can comfortably afford, keep it. Use that money to invest and earn higher returns. Liquidity and flexibility are valuable, especially as you approach retirement.

Pre-Retirement and Retirement: Ages 55+

You’re on the landing page. Time to shift from accumulation to preservation and distribution.

Play Defense First

Once you’ve reached financial independence, your primary goal is to never go backward. This means:

- Backing down from aggressive investments

- Ensuring adequate insurance coverage (life, long-term care, final expense)

- Having a comprehensive estate plan

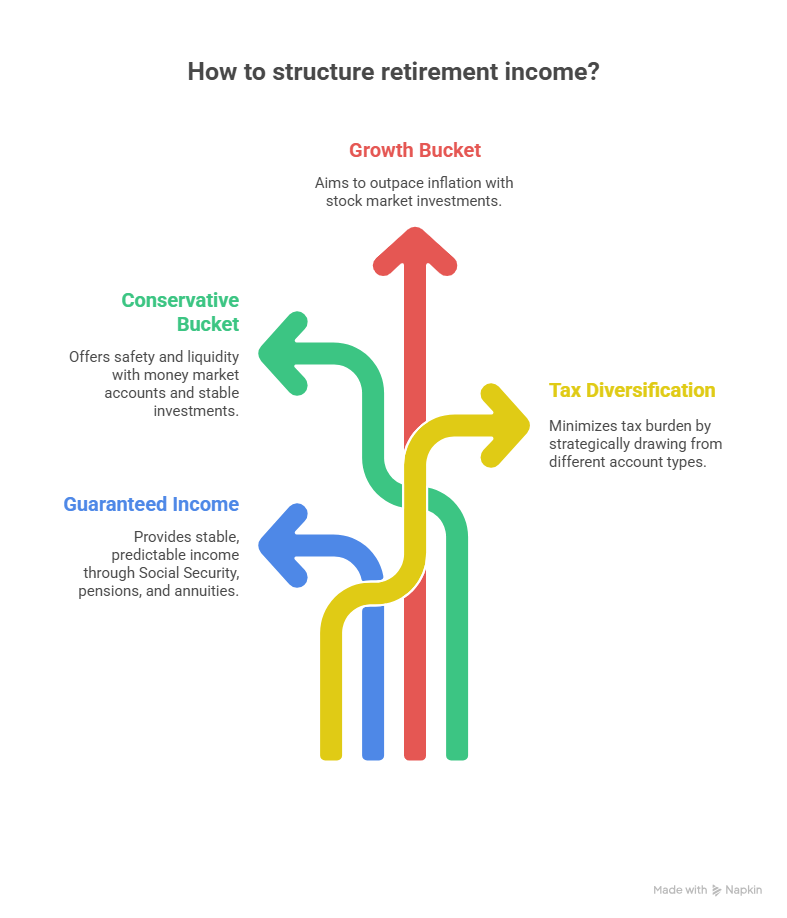

How to structure retirement income?

Create Your Income Buckets

Structure your retirement income from multiple sources:

1. Guaranteed Income

- Social Security (if you’re working at full retirement age, consider taking it and investing the payments)

- Pension (if you have one)

- Lifetime income annuities (a $300,000 annuity at age 67 can provide approximately 8% annual lifetime income)

2. Conservative Bucket

Money market accounts and stable investments to draw from when the stock market is down

3. Growth Bucket

Stock market investments to combat inflation over your 20-30+ year retirement

4. Tax Diversification Pull from different account types strategically to minimize taxes

The Three-Bucket Investment Strategy

Divide your retirement portfolio roughly into thirds:

- One-third: Guaranteed or highly secure (annuities with principal protection, treasuries)

- One-third: Conservative growth (bonds, balanced funds, annuities with upside potential)

- One-third: Growth investments (stocks, equity funds for long-term inflation protection)

Final Expense and Legacy Planning

Make sure you have:

- Final expense insurance to cover funeral and end-of-life costs

- Updated will and living trust

- Financial and healthcare power of attorney

- Clear beneficiary designations

A properly structured estate plan prevents family conflict and ensures your assets go where you intend them to go.

The Power of Automation

Across every life stage, one principle remains constant: automate everything.

Set up automatic transfers to savings and investment accounts. Make it impossible to forget or “decide later.” The moment your paycheck hits, your financial future should be funded first.

Think of it this way: When you spend $1,000 today instead of investing it, you’re not just losing $1,000. At 10% returns, you’re actually losing:

- $2,000 in 7 years

- $4,000 in 14 years

- $8,000 in 21 years

- $16,000 in 28 years

Every dollar counts. Every dollar today represents your lifestyle tomorrow.

Start Where You Are

Maybe you’re reading this at 25 with your whole career ahead. Perhaps you’re 45 and realize you’re behind. Or maybe you’re 60 and worried it’s too late.

Here’s the truth: The best time to start was 20 years ago. The second-best time is today.

Whether you need to grow your income, slash your expenses, get out of debt, or completely restructure your investments, there’s a path forward. Financial independence is achievable at any age with the right plan and commitment.

Take the Next Step

Building wealth is simple, but it’s not easy. It requires discipline, consistency, and often, professional guidance to avoid costly mistakes.

If you’re ready to create your personalized financial blueprint:

- Visit: roymatlockjr.com

- Call: (615) 843-2999

- Schedule: A complimentary 30-minute consultation

We’ll review what you’ve done right, identify what needs correction, and create an actionable plan to move you forward. We’re implementers—we automate and execute so you can focus on living your life with one less worry: your financial future.

Listen to the Full Podcast

Want to hear Roy walk through this entire lifetime financial blueprint in detail? Listen to the complete episode here: Start Smart, Finish Strong: Your Lifetime Financial Blueprint

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is? Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.