Mastering the Money Mindset: 10 Wealth-Building Habits the Rich Use

After 41 years in the financial business and working with over 40,000 clients, I’ve developed what I call “carnival vision”—I can walk into someone’s home and within minutes tell you their financial situation based on what they spend money on. New car in a modest neighborhood? Probably broke with debt. Paid-off older car? Likely has money saved.

The patterns are consistent. Wealthy people do specific things that struggling people don’t. Today, I’m sharing the 10 wealth-building habits I’ve observed across four decades of helping people fix their finances.

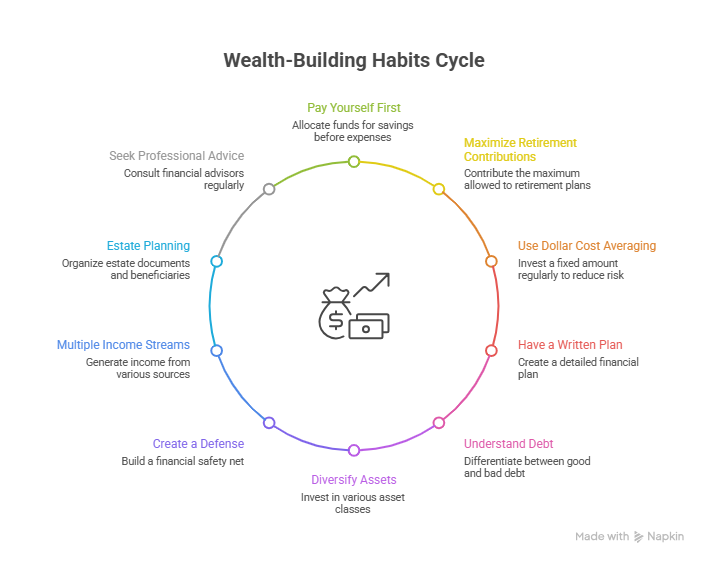

Wealth-Building Habits Cycle

Habit #1: Pay Yourself First

I feel more sorry for people who work Monday through Friday, eight to five for years and end up living paycheck to paycheck than I do for homeless people. Why? Because they made a choice—they decided NOT to make a profit on their efforts.

The mindset shift: Treat savings like a bill. It’s not optional.

The implementation: Automate it. Wealth is built by consistency, not occasional effort.

If you simply put away 10% of your income automatically, you will see dramatic results. This isn’t about willpower—it’s about removing the decision from your daily life. The money gets drafted before you can spend it.

Habit #2: Maximize Retirement Plan Contributions

Let the government give you a loan. Here’s how it works:

Put $10,000 into a deductible retirement account (like a 401k) while in the 25% tax bracket. You save $2,500 in taxes that year. That $2,500 sits in your account for potentially 30-40 years until you’re required to take distributions at age 73.

The compounding magic: At 10% return, money doubles every seven years. Over 30 years, you get four doubling periods.

The buy-one-get-one-free strategy: Put your money in a deductible 401k, then take the $2,500 in tax savings and stick it in a Roth IRA. You just bought one account and got another free. One grows tax-deferred, the other grows tax-free.

Business owners have even more options—SEP IRAs, Solo 401ks, Safe Harbor plans. These vehicles can shelter tens of thousands in income annually while building retirement wealth.

Habit #3: Use Dollar Cost Averaging

Dollar cost averaging means investing on a regular, consistent basis regardless of market conditions. And in the accumulation phase, you actually want the market to go down.

Why? Because you’re buying at a discount. The market always recovers, and you end up owning more shares at lower prices.

Stop trying to time the market. Set up your IRA to draft monthly from your checking account, and forget about it for the next 20-30 years. It’s automatic. It’s consistent. It works.

I have people tell me every year: “Yeah, I want to fund my IRA.” Here’s what I tell them: Let’s put in the amount for the months we’re already into the year right now, then set up automatic monthly drafts for the rest. Now it’s automatically funded for the next 20-30 years.

Why this works: When you wait to have “money left over,” you never do. There’s always something else to spend it on.

Habit #4: Have a Written Plan

Anything you put in writing automatically improves. Anything you review regularly gets better.

Most people plan their vacation more than they plan their personal finances—which is ironic, since good financial planning is the only way you can truly afford those vacations.

When you work with us, we help you create an automated plan for financial independence. Here’s our process:

- Education – Make sure you understand your strategy well enough to explain it to a friend

- Review – Assess where you are today financially

- Defense – Build protections to prevent costly mistakes

- Offense – Create growth strategies for wealth accumulation

- Product Marketplace – Match the right financial tools to your situation

- Updates – Adjust the plan as life changes

Your plan should be revisited annually at minimum. I have clients I’ve worked with for 30 years. We meet every six months to a year, look at goals, and adjust as needed. They’ve become friends, and their financial success has been built on this ongoing relationship.

Habit #5: Understand Good Debt vs. Bad Debt

This is critical: Debt is not inherently bad. A mortgage is not bad. Here’s the distinction:

Good Debt

- Easily affordable payments

- Tied to appreciating assets (homes, rental properties, productive business equipment)

- Example: A 3% mortgage on a house appreciating at 4% annually

Bad Debt

- You can’t comfortably afford the payment

- Tied to depreciating assets (new cars, credit cards, consumer goods)

- Example: Financing lunch and dinner on a credit card or buying a car you can’t afford

Real talk: Don’t pay off those 3% mortgages. There are much better places to put that money when you can earn 8-12% in the market.

Habit #6: Diversify Across Different Asset Classes

Your asset allocation should match your age and time horizon:

Aggressive (Young accumulators): Stocks for growth and inflation protection

Middle Range: Balanced mix of stocks and bonds

Conservative (At or near retirement): Bonds, annuities, and guaranteed income sources

Most Conservative: Cash and money market accounts

The key principle: Always have cash available so you never have to sell investments when markets are down.

This starts with your emergency fund (3-6 months of expenses). If you lose your job, you pull from cash—not from your retirement plan where you’d face penalties and taxes.

As you accumulate wealth, raise your insurance deductibles (saving on premiums) and possibly self-insure older vehicles with just liability coverage. Your emergency fund makes this possible.

Habit #7: Create a Great Defense

The proper insurance protects everything you’ve built. Average financial mistakes cost $50,000 to $500,000 over a lifetime—and most are preventable with the right protection.

Term Life Insurance

- Pure death benefit, no cash value

- Protects income replacement

- Rule of thumb: 10-12 times your annual income

- Length: Until normal retirement age

- Get policies with living benefits riders (access up to 90% of death benefit if critically or terminally ill)

Permanent Life Insurance

- Kept until death

- Pays final expenses and estate taxes

- Replaces lost Social Security income for surviving spouse

- Changes your family tree by leaving a legacy

- Cash value grows tax-deferred, distributions come out tax-free

Disability Insurance

- Replaces 60-70% of income if you can’t work

- I believe becoming disabled is worse than dying—you can’t work, can’t earn, and can’t fix the situation

Health Insurance

- Number one cause of bankruptcy is lack of health insurance

- Consider high-deductible plans with Health Savings Accounts (HSAs)

- HSAs are like “super IRAs”—tax-deductible going in, grows tax-deferred, tax-free for medical expenses

Property & Casualty Insurance

- Home and auto with adequate liability coverage

- Umbrella policy ($1-2 million in extra liability protection)

- Raise deductibles as emergency fund grows

- Work with independent agents representing multiple carriers

Habit #8: Create Multiple Income Streams

Most wealthy people I know don’t rely on a single income source. They have:

- Primary income (job or business)

- Side business or consulting

- Investment income (stocks, bonds, mutual funds)

- Passive income (rental properties, royalties)

- Retirement accounts generating distributions

My father owned 40 rental properties at one time, plus his main business. He created multiple streams that worked together to build substantial wealth.

Don’t put all your eggs in one basket. If one income stream dries up, you have others to fall back on.

Habit #9: Get Estate Documents and Beneficiaries in Order

I run into people regularly who have nothing in place. Over 60% of Americans have no estate planning.

The consequences of doing nothing: Your kids fight over money, your spouse has problems, or maybe you don’t have healthcare or financial power of attorney when you need it most. The probate court will decide for you, and attorneys and lawsuits will drain whatever estate remains.

For most people with assets, you need:

- Living Trust

- Healthcare Power of Attorney

- Financial Power of Attorney

- Living Will

- Updated beneficiary designations on all accounts

The biggest benefit is while you’re living. If something happens and you’re incapacitated, someone can make medical decisions and pay your bills on your behalf—without court intervention.

Habit #10: Get Professional Advice and Meet Regularly

The wealthy understand that people who know more about money than they do can add tremendous value. They meet with advisors regularly—not just when there’s a crisis.

Work with a fiduciary advisor. We’re legally required to act in your best interest. We’re not tied to any one company or product, which means we can recommend what’s truly best for you.

Annual check-ins are essential. Where are you at in life right now? What’s changed? What needs adjusting?

I have clients I’ve worked with for 30 years. We meet consistently, maintain the relationship, and adjust strategies as they age and their needs change. They stick to their lane; we stick to ours.

The Power of Professional Money Management

Let me illustrate the difference professional management makes with actual numbers.

Scenario: Save $500 per month for 30 years

- At 3% (typical bank savings): $286,000

- At 8% (conservative professional management): $684,000

- At 10% (S&P 500 historical average): $995,000

- At 12% (aggressive professional management): $1,476,000

Same effort. Same $500 monthly contribution. But the difference between parking money in a savings account versus working with professional managers? Over $1.1 million.

Become an Owner, Not a Loaner

This changed my life in 1985 when I bought my first mutual fund.

The bank scenario: You loan the bank money at 2-3%. They loan it back out on credit cards at 19% or car loans at 13%. Who makes more money—you or the bank? Always the bank.

The solution: Own the bank. Buy stock in banks through mutual funds managed by professionals who research and select the best ones.

The Vegas scenario: Would you rather be the gambler or own the casino? The house always wins. So own the house—buy stock in casino companies.

What is a mutual fund? Your $50 gets pooled with thousands of other investors’ money. Together, you hire a team of professional money managers with the same expertise available to people with $100 million. You get institutional-quality management on a retail budget.

Investment Account Types You Should Know

Throughout life, you’ll use different account types strategically:

- Retirement Funds – 401ks, IRAs, Roths (tax deductions, tax deferral, or tax-free growth)

- Insurance Cash Values – Permanent life insurance (tax-deferred growth, tax-free distributions)

- College Funds – 529 plans, ESAs, UTMAs/UGMAs (education-specific tax benefits)

- Opportunity Funds – Better than bank accounts, available for unexpected opportunities

- Non-Retirement Tax-Deferred – Annuities (tax-deferred growth outside retirement plans)

- Income Funds – Annuities with lifetime income guarantees

- Healthcare Funds – HSAs, long-term care insurance

Asset allocation means spreading money across these accounts based on your age, goals, and time horizon. As you age, you might make your 401k lump sum more conservative while keeping monthly contributions aggressive to benefit from dollar-cost averaging.

Special Considerations for Business Owners

If you’re self-employed, you’re in a unique position—and you face unique risks.

Common Business Owner Mistakes I See:

Partnership Problems

- Two brothers own a business 50/50 for 35 years

- One brother has two sons active in the business who will take it over

- Other brother has a son with no interest (or problems)

- First brother dies—now you’re in business with someone uninterested or problematic

The solution: Buy-sell agreements funded with life insurance. Get business valuations, buy insurance on each partner, and structure automatic buyouts if someone dies.

Retirement Plan Issues

- Signing 5500 forms without understanding what you’re signing

- Taking on excess personal liability for plan administration

- Not maximizing available contributions (SEPs, Solo 401ks, Safe Harbor plans)

Missing Protections

- No key employee insurance

- No business continuity plan

- No succession planning

- Healthcare costs out of control

The cost of doing nothing: Overpaying taxes, risk exposure, and lost opportunities. You’re great at your business, but you don’t have a business financial plan.

Taking Action: Change Your Family Tree

Here’s something powerful we do: Family Financial Workshops.

Open a $250 investment account for your kids or grandkids. Then bring the whole family together—like a financial family reunion. We teach everyone how money works, how to invest, how to build wealth.

I started this with my mother’s birthday gatherings. We’d create worksheets, fill-in-the-blanks education, and hands-on learning. Now my mother is over 100 years old, we have five generations, and every family member has an investment account and understands wealth building.

Imagine this: If you asked any of your kids how their money works, they could explain it clearly. That’s the power of family financial education.

We can do these workshops via Zoom or in person. It changes your entire family tree in one meeting.

The Bottom Line

These 10 habits aren’t complicated. They’re not secrets. But they are what separates wealthy people from those living paycheck to paycheck:

- Pay yourself first (automate savings)

- Maximize retirement contributions (tax advantages)

- Use dollar-cost averaging (consistency over timing)

- Have a written plan (review and adjust regularly)

- Know good debt from bad debt (leverage wisely)

- Diversify across asset classes (appropriate to age)

- Create a great defense (proper insurance)

- Build multiple income streams (reduce reliance on one source)

- Get estate planning done (protect your legacy)

- Work with professionals (fiduciary advisors who meet regularly)

You have over 200 podcast segments on roymatlockjr.com covering everything you need to know about money. The education is there. The tools are available. The only question is: Will you take action?

After 41 years, I can tell you this with certainty—the people who implement these habits don’t worry about money anymore. They’ve taken that stress off the table. And you can too.

Listen to the Full Podcast

Want to hear the complete breakdown of these wealth-building habits with additional examples, real client stories, and detailed strategies? Listen to the full episode where I walk through each habit in depth.

Listen to the full podcast episode: “Mastering the Money Mindset: 10 Wealth-Building Habits”

In this episode, I share the “carnival vision” that lets me predict someone’s financial situation within minutes, explain the exact numbers behind compound interest at different rates, and detail how professional money management can add over $1 million to your retirement nest egg. Don’t miss these insights from four decades of helping people build wealth.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.