What Wealthy People Do That Most People Don’t

After 40 years of helping people win with money, Roy Matlock Jr. has seen a clear pattern: wealth is not an accident. In this episode of The Roy Matlock Jr. Money and Business Hour, Roy lays out the complete financial playbook that separates people who build lasting wealth from those who work hard but never quite get ahead. Whether you are just getting started or looking to plug the holes in your current plan, this episode covers every piece of the puzzle.

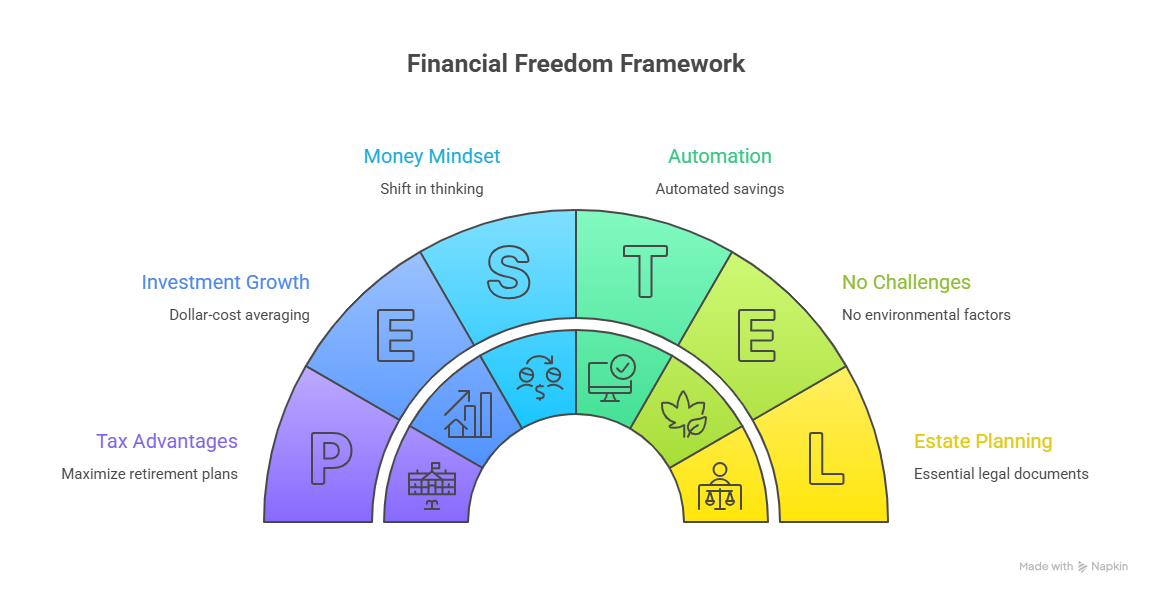

Start With a Written Plan — Your Financial GPS

Wealthy people do not stumble into financial freedom. They decide to get there. Roy’s framework for this is simple: Goal, Plan, Schedule — what he calls your Financial GPS. You write down exactly where you want to go financially, you map out how to get there, and you put it on a timeline. Roy has been doing this himself since the mid-1980s, and his written plan has grown to about 80 pages covering every area of his life and finances.

The act of writing it down and reviewing it daily creates what Roy calls a money mindset — a shift in how you think and feel about spending versus saving. Once you have that mindset, the decisions become easier because you have already decided who you are with money.

Define Your “Do-Nothing Money” Goal

The destination on your financial GPS is what Roy calls do-nothing money: enough accumulated wealth that your investments pay you whether you work or not. The rule of thumb Roy uses is 16 to 20 times your desired annual income. If you want to live on $100,000 per year, your target is $2 million. At a 5% withdrawal rate, that money never runs out.

Pay Yourself First — Automatically

One of the most powerful things wealthy people do is treat savings like a bill that gets paid before anything else. Roy recommends automating at least 10 to 25% of your income into investments the moment it hits your account. You never see it, so you never miss it.

Roy tells the story of a client who now has $4,000 per month automatically moving into investments without thinking about it. That kind of automated consistency — not occasional effort — is what builds wealth over time. Wealth is built by consistency, not intention.

The best analogy Roy uses: if you had waited 10 years before starting to invest the same amount as someone who started today, that other person would have ended up with a million dollars more than you — simply because their money had an extra decade to double.

Dollar-Cost Averaging: Let the Market Work For You

Closely tied to paying yourself first is the practice of dollar-cost averaging — investing a set amount on a regular schedule regardless of what the market is doing. When prices are down, your fixed contribution buys more shares. When prices recover, you benefit from all those discounted purchases.

Roy walked through what happened between 2006 and 2012 when markets fell and stayed down for years. The people who kept investing through that period were buying at a discount the entire time. When the recovery came, they were far ahead of those who stopped out of fear. The lesson: when you are in the accumulation phase, a down market is your friend.

Maximize Every Retirement Plan Available to You

Wealthy people do not leave tax advantages on the table. Roy breaks down the main vehicles: 401(k), 403(b), and 457 plans through employers — always capture the full match, because that is free money and an instant tax deduction. Then there are traditional IRAs, Roth IRAs, and the backdoor Roth IRA strategy for higher earners who make too much to contribute directly. A SEP IRA or solo 401(k) for self-employed individuals can allow even larger contributions.

The tax savings from a deductible retirement account can be reinvested into a Roth, giving you both the upfront deduction and tax-free growth on the savings — what Roy calls a buy-one-get-one-free move.

Diversify Across Risk Buckets and Tax Buckets

Wealthy people do not put all their money in one type of account or one type of asset. Roy organizes investments into two dimensions: risk buckets and tax buckets.

Risk buckets include cash and money markets for safety, bonds for conservative income, stocks and stock funds for long-term growth, and annuities for guaranteed lifetime income backed by an insurance company. The goal is that when the market is down, you pull from the conservative buckets — not forced to sell stocks at a loss. When the market is up, you let your growth run.

Tax buckets mean having a mix of pre-tax accounts, tax-free accounts like a Roth, and taxable accounts so you can pull income from the most efficient source in retirement depending on your tax situation in any given year.

Build Your Defense: Protect Everything You Have Built

Roy is emphatic that offense without defense is a losing strategy. Here is what a solid financial defense looks like.

An emergency fund covers three to six months of expenses and protects you from derailing your investments when life hits unexpectedly. A real, working budget — one that includes irregular expenses like car repairs, vacations, and holidays — is the foundation that allows you to consistently produce a financial profit every month. Roy recommends downloading the budget form at roymatlockjr.com and combining it with an automated draft account so that your bills, savings, and living expenses all flow predictably.

Good debt versus bad debt matters more than most people realize. Good debt is affordable and tied to something that appreciates — like a mortgage at 3%. Roy is direct: do not rush to pay that off. That rate will never exist again in our lifetimes, and the money is better deployed elsewhere. Bad debt is anything that is unaffordable or tied to something that loses value. That gets eliminated as fast as possible.

Insurance is a critical piece of defense. Roy sees people consistently under-insured — particularly on liability coverage. Term life insurance, disability income protection, health coverage, and proper property and casualty insurance all protect the income and assets you are building. Most bankruptcies, Roy notes, trace back to a lack of proper insurance coverage.

Estate planning documents — a will, healthcare power of attorney, financial power of attorney, and living will — are essential and yet over 60% of Americans have none of them in place. This matters especially for single people who would have no one with legal authority to manage their affairs if they became incapacitated.

Create Multiple Income Streams

Wealthy people do not rely on a single source of income. Roy’s own framework: primary business income, plus passive investment income that runs without his direct management, plus multiple streams inside his business.

Whether that means starting a side business, building investment accounts that produce income, owning rental properties actively or passively, or a combination of all of the above — the goal is to reach a point where one setback cannot destroy your financial life. As Roy puts it, you do not hustle to get ahead. You hustle so you cannot be knocked out.

Work With a Fiduciary to Implement It All

Everything Roy describes in this episode — the planning, the automation, the tax strategy, the product selection, the defense — requires implementation, not just intention. Roy calls himself an implementer of financial independence. The difference between a plan that sits in a drawer and one that actually changes your life is having someone who executes it with you.

If you are ready to get your plan in motion, visit roymatlockjr.com to schedule a phone call, or call 615-843-2999. The first step is a conversation.

All four segments of this episode are available now. You can listen to the complete November 1, 2025 episode of The Roy Matlock Jr. Money and Business Hour here: PODCAST: November 1, 2025 – Pay Yourself First, Forever

Roy covers every topic above in his own words — with real client stories, specific numbers, and decades of hard-won perspective. It is one of the most comprehensive single-episode breakdowns of the complete wealth-building system Roy has spent 40 years developing. Worth your full attention.

Business Owners on the Air with Roy

Are you a successful small business owner, or maybe you know someone who is! Roy wants to interview business owners who have success stories for inspiration to our listening audience, to share their journey from starting out to success. Nominate someone you may know, or yourself, by clicking here.